ATO Record-Keeping Requirements: How Long Australian Electricians Really Need to Keep Their Books

Published on April 21, 2026

Ever missed a BAS deadline because an invoice was buried in the ute, or had the Australian Taxation Office call about something you thought was sorted, but you could not find the paperwork? ATO record-keeping requirements: how long Australian electricians really need to keep their books is rarely top of the list, but it can be the difference between a simple question and a stressful review.

If you run an electrical business, you are expected to keep the records you need that show your business income, business expenses, tax deductions and financial position. The real challenge is working out how long to keep tax records, which business records actually matter, and how to manage them without living in a pile of old folders.

The Real-World Problem with Record Keeping for Electricians

Most sparkies in ACT do not get into business because they love record keeping. You are often moving from job to job, quoting, supervising staff or apprentices, and dealing with clients who sometimes pay cash, sometimes pay by transfer, and sometimes pay late. By the time you sit down at the end of the day, tax records usually feel like the last thing you want to think about.

Struggling to stay on top of ATO record‑keeping for your electrical business?

Schedule a complimentary consultation with us today to set up an easy, ATO‑compliant system that fits how you work.

Mixed Records and Missing Details

Because life is busy, many electricians end up with a mix of bank statements, original paper records, electronic copies and random receipts. Some paperwork sits in the office, some in the ute, and some in an email inbox. You might know that the Australian Taxation Office expects written evidence for work related expenses and other deductions. What is not always clear is which records need to be kept, what a complete copy looks like, and whether a photo or credit card statement will be enough if questions come up later.

Stress at Tax Time and ATO Questions

This confusion tends to hit hardest at tax time. When it is time to prepare your income tax return, you may feel that you are guessing some of the totals for your total claim because you cannot find every original record. The worry is that you could end up paying more tax than necessary, or that an ATO review will uncover records that were accidentally lost or never kept. That can create pressure, even if your business income and business expenses are otherwise under control.

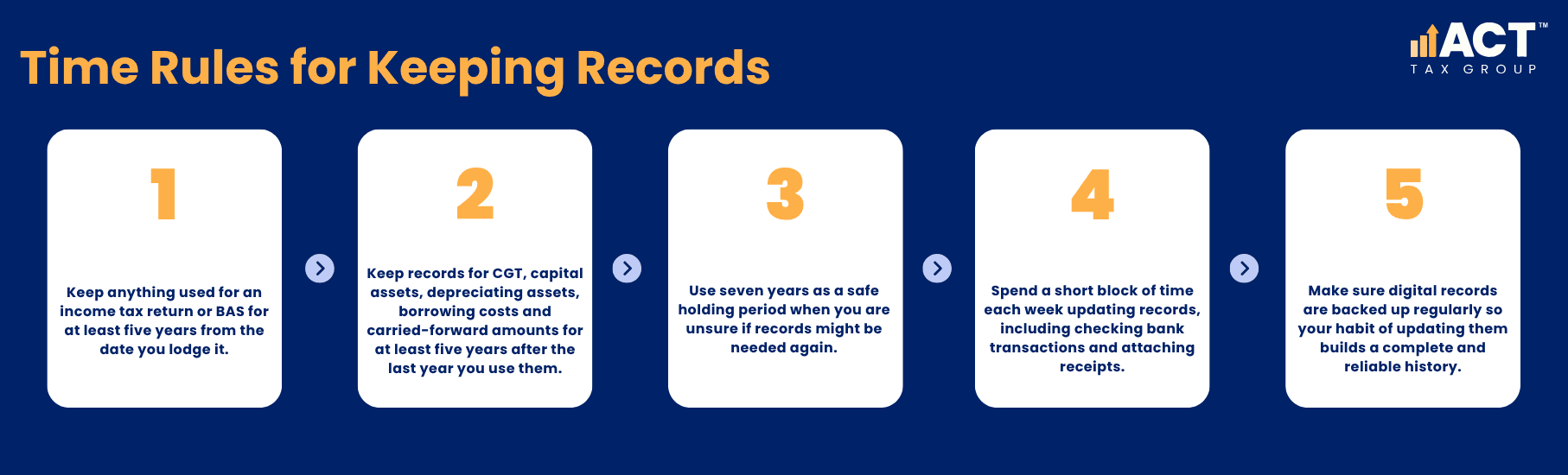

The Five-Year Rule: The Minimum Time Most Records Need to Be Kept

The basic ATO rule is that most business records need to be kept for at least five years. For most electricians, this is the starting point when planning how long to retain records.

When the Five Years Starts

For many business records, the 5-year period starts from the later of when you prepared or obtained the record, or when the transaction or act it relates to was completed. For records used to support claims in an income tax return, the 5-year period will often run from the date you lodge that return, although some records must be kept longer where their tax effect continues into later years. For example, if you lodge your 2024–25 return in October 2025, the tax records supporting that return generally need to be kept until at least October 2030.

What This Means in Day-to-Day Terms

In practical terms, you should plan to keep any record that supports income tax, GST, PAYG instalments or tax deductions for at least five years from the relevant date so you can avoid common tax deduction mistakes. If in doubt, it is safer to keep records a little longer than the minimum. Many businesses use seven years as an internal rule, so they do not accidentally destroy something that relates to a later income year or a final claim on a long-term item. This information requires professional verification for your specific situation.

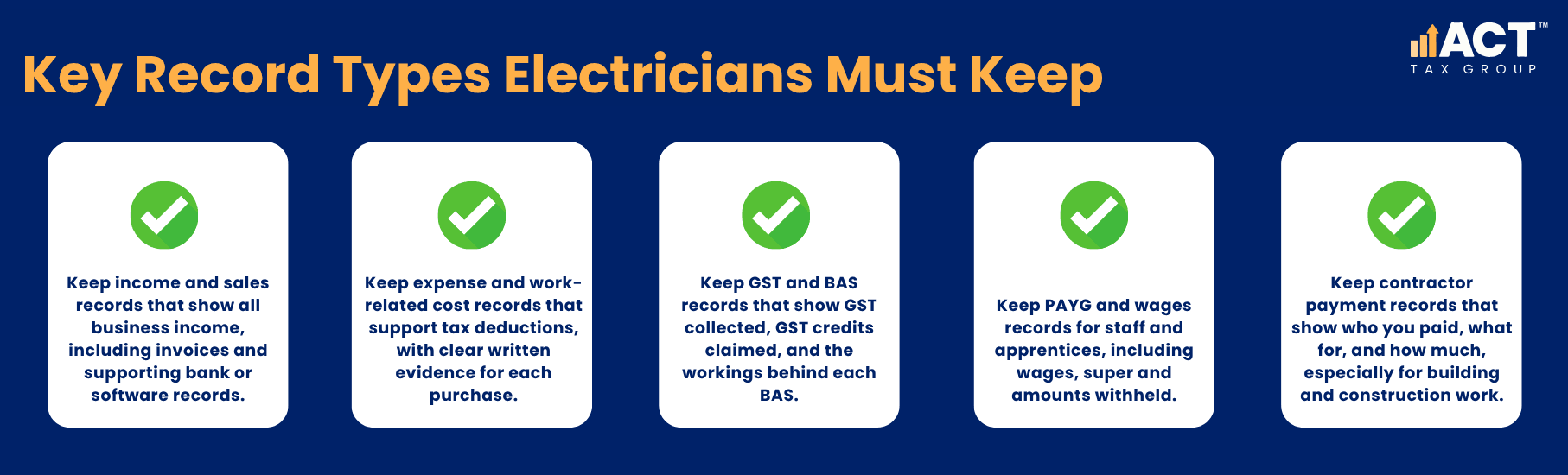

Records You Need as an Electrician

For an electrical business, the records you need fall into several clear categories. Thinking about them this way makes it easier to check whether your record keeping is complete.

Income and Sales Records

Income records show your business income from all sources. This includes invoices you issue for jobs, whether they are residential, commercial or maintenance work. These records should clearly show your business name, the customer, the goods or services date, payment amounts and how the client paid. Bank statements and reports from your accounting software or record keeping app can also support these amounts, as long as they connect clearly back to each transaction.

Expense, Deduction and Work-Related Cost Records

Expense records support your tax deductions and show what each expense relates to. For an electrician, this includes materials, tools, fuel, repairs, insurance, phones, internet, uniforms and other work-related expenses. The Australian Taxation Office generally expects written evidence such as receipts, invoices or similar documents, even if you are using simplified methods like the fixed rate method for certain work deductions. A bank or credit card statement on its own is generally not enough. You usually need written evidence such as a receipt or invoice showing the supplier, amount, date, and nature of the goods or services. The evidence should make it clear what was purchased, when, and that it was paid by your business.

GST, BAS and PAYG Records

If you are registered for GST, you need records that support your GST collected and the credits you claim so you can maximise your GST credits and stay compliant. This includes the invoices and receipts that show GST, as well as the workings behind your Business Activity Statements and GST reporting. PAYG instalment amounts, including those reported on Instalment Activity Statements, also rely on good records. Keeping your workings for each BAS, rather than just the final figures, makes it easier to answer any questions about changes between one period and the next.

Wages, Apprentices and Contractor Records

If you employ staff or apprentices, you need records for wages, super, PAYG withholding and employment terms. Employee time and wage records generally must be kept for 7 years under Fair Work laws, in addition to tax record-keeping rules. If you use contractors, especially in building and construction, keep records showing the contractor’s details, payment amounts, and the services supplied. You may also need these records for Taxable Payments Annual Report (TPAR) obligations. These records help separate business transactions from personal spending and are important if you need to report contractor payments.

When Five Years Is Not Enough

While the five-year rule covers most tax records, some records need to be kept longer. This usually happens where the tax effect stretches across several years.

Capital Gains Tax Assets and Capital Assets

If your business owns capital gains tax assets, such as commercial premises, investment properties, shares, managed funds or inherited property subject to CGT, the record keeping rules are stricter. For Capital Gains Tax (CGT) assets, you generally need to keep records for at least 5 years after the CGT event, and longer if the records are needed to work out a later capital gain or to support a carried-forward capital loss. That means records for purchase costs, improvement costs, sale proceeds and other documents that affect the capital gains tax calculation may need to be kept for much longer than five years.

Depreciating Assets and Long-Term Claims

Depreciating assets, such as larger tools, vehicles and equipment, are often claimed over a number of years, and managing these claims is easier if you are using ATO Online Services for Business. For depreciating assets, you generally need to keep records for as long as you hold the asset and for 5 years after you sell or otherwise dispose of it. Special rules can apply for low-value pools or rollover relief. If you spread borrowing costs over several years, or if you carry forward a business loss into later years, the records that support those amounts also need to be kept until at least five years after the final year in which they are claimed. This information requires professional verification based on your specific claims.

Company and Employment Records

If you run your business through a company, company officeholders must keep important company records, including financial and governance records, so you do not run into issues like ASIC late fees and penalties. Separately, employee time and wage records must generally be kept for 7 years under Fair Work laws. This can apply to employee details, pay records and other employment documents. It is important to check both tax and workplace rules before destroying any older records. This information requires professional verification for your structure and staff arrangements.

What Acceptable Records Look Like in Practice

The ATO is not only interested in how long you keep records, but also in the quality of those records. Whether you use paper, digital records or a manual system, the same basic standards apply.

Clarity, Completeness and Language

Records should be clear and complete. They should show enough detail for someone else to understand your business transactions without guessing. They must be in English or easily converted to English. They should show dates, amounts, names, and what the goods or services were. This applies equally to income tax, GST and other obligations.

Paper Records, Digital Records and Electronic Copies

If you receive original paper records, you can keep them as they are or create electronic copies by scanning or photographing them. The electronic version must be a true and clear reproduction, showing all the information from the original record. Once you have a complete copy stored safely, you may not need to keep the original paper records, as long as the copy would be accepted as sufficient evidence if the ATO asks for it.

Keeping Records Safe and Ready to Use

Records should be stored in a way that protects them from damage and data loss. For digital records, that means regular backups, secure logins, and checks that files remain readable over time. For paper records, that means safe storage where they will not be easily destroyed or mixed in with personal documents. The goal is that if the ATO calls, you can find and share the records quickly, without a major search.

Digital Records Versus Paper: Choosing a System That Works

Many electricians now prefer digital records because they reduce clutter, make it easier to keep up to date records, and support tax‑savvy strategies to boost profits. A simple, well-thought-out system can support both daily work and ATO requirements.

Using Accounting Software and Record Keeping Apps

Accounting software can connect to your bank statements, so business income and payment amounts appear automatically. This helps you keep track of business transactions and generate reports that show your financial position. A record keeping app lets you photograph receipts for fuel, tools and other expenses as you go. These images can be attached to transactions inside the software, creating a clear link between the payment and the written evidence.

Organising by Financial Year and Record Type

A helpful approach is to sort records by financial year and then by type, especially if you are monitoring income levels closely to stay under the GST registration threshold. For example, you might have folders or categories for income, expenses, capital assets, payroll and other records within each year. This makes it easier to review a single income year if needed. It also makes it clear when records for that year have reached the end of their required time period and may be ready to be destroyed, after you confirm there are no longer-term claims tied to them.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

Lost or Destroyed Records: What to Do if Things Go Wrong

Even good systems are not perfect. Records can be accidentally lost, damaged in an accident or destroyed in events like fire or flood.

Rebuilding From Other Documents

If records are lost or destroyed, you may still be able to support your claims by rebuilding the information from other documents. Bank statements, credit card statements, duplicate copies from suppliers, emails and similar documents can all help recreate the trail of a transaction. The aim is to show that you have sufficient evidence for your final claim, even if the original record is gone. If records are lost or destroyed, the ATO may accept replacement records or other evidence, particularly where you took reasonable precautions and it is not reasonably possible to obtain a substitute document.

Talking to Your Accountant Before Lodging

If you know that some records cannot be recovered, it is important to discuss this with your accountant or tax agent before you lodge your return. They can help decide whether the remaining evidence is strong enough or whether it is safer to adjust certain expenses. Being open about data loss and showing that you have tried to replace the missing information with similar documents, can help reduce the risk of problems later.

A Simple Way to Think About How Long to Keep Records

It helps to have a straightforward way to think about all of this, so record keeping becomes part of your normal routine rather than a yearly panic.

A Practical Time Guide

Records supporting an income tax return or BAS often need to be kept for at least 5 years, but some records must be kept longer. This commonly includes CGT records, depreciating asset records, delayed GST input tax credit claims, and records supporting carried-forward losses or other amounts used in later years. If you are unsure whether something will be needed again, keeping it for seven years is often a safe internal rule. This information requires professional verification, especially if you have a company or more complex investments.

Making Record Keeping a Regular Habit

Instead of waiting for tax time, it is easier to spend a short amount of time each week updating your records. That might mean checking bank transactions, attaching receipts, saving new contracts, and making sure your digital records are backing up correctly. Over time, this habit means your records are always close to complete. You are not trying to remember every detail at once, and you are less likely to miss something important.

Getting Support to Set Up a Better System

You do not need to become a tax specialist to meet the Australian Taxation Office record keeping rules. What you do need is a system that fits how you work and gives you confidence at tax time. ACT Tax Group works with electricians in ACT to set up practical record keeping systems. This includes choosing accounting software, setting clear rules for how long to keep different records, and making sure digital records are stored safely and can be easily shared if needed.

By mapping the flow of your jobs, from quote to payment, and checking that the right records are captured at each step, we help you stay compliant while keeping your admin load as light as possible.

Conclusion

For Australian electricians, record keeping is about more than keeping the ATO happy. It is about protecting your business, your time and your peace of mind. Most records must be kept for at least five years, and some, like capital gains tax assets and depreciating assets, must be kept longer. Digital records, backed by sensible habits, can make this task manageable.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)