How Medicare Levy Surcharges Work for High-Earning Electricians

Published on April 14, 2026

How Medicare Levy Surcharges Work for High-Earning Electricians is something many sparkies only discover when their income tax bill jumps and they realise they may have to pay more than just the usual levy. You might be flat out on the tools, your annual income looks strong, but when you lodge your tax return the Australian Taxation Office shows an extra charge on top of the standard Medicare Levy because your income level has moved up and you do not have the right private hospital cover.

The Real Issue: “Why Am I Suddenly Paying a Surcharge?”

This is usually the first question that comes up when an electrician has a stronger year and sees a bigger tax bill than expected.

You might be thinking, “Most taxpayers pay something for Medicare anyway, so why am I copping more?” That extra cost is often the Medicare Levy Surcharge (MLS), which sits on top of the normal levy and catches higher incomes without appropriate hospital cover.

Avoiding unexpected MLS charges on your tax bill?

Schedule a complimentary consultation with us today to check your income thresholds and cover status.

When Your Income Jumps

When your electrical business grows, your business profit, wages and certain add-backs used for MLS purposes, such as reportable employer super contributions, can increase the income used to assess MLS. That is where many electricians get caught without realising they have moved into a new income level that triggers extra charges.

Once your income steps over key thresholds for MLS purposes, the system can treat you as a higher‑income earner, even if your cash flow still feels tight because of tools, vehicles and staff, or because you are trying to stay under the GST registration threshold to simplify your business.

Levy vs Surcharge Shock

The Medicare levy is a standard charge that helps fund Australia’s public health system and is something most Australian residents pay. The MLS, however, only applies to higher incomes who do not hold appropriate hospital cover for themselves, their spouse and any dependent child for the full income year.

For a busy electrician, that can mean an extra percentage of tax on top of everything else, automatically calculated by the Australian Taxation Office (ATO) based on your income and private health insurance information.

What Is the Medicare Levy and the Medicare Levy Surcharge?

It helps to separate the two charges so you can see what is standard and what is avoidable with the right planning.

The levy is the baseline contribution that supports Medicare benefits and public hospitals. The surcharge is the extra amount that kicks in only when your income for MLS purposes passes certain income thresholds and you do not have appropriate hospital cover in place.

Medicare Levy Explained

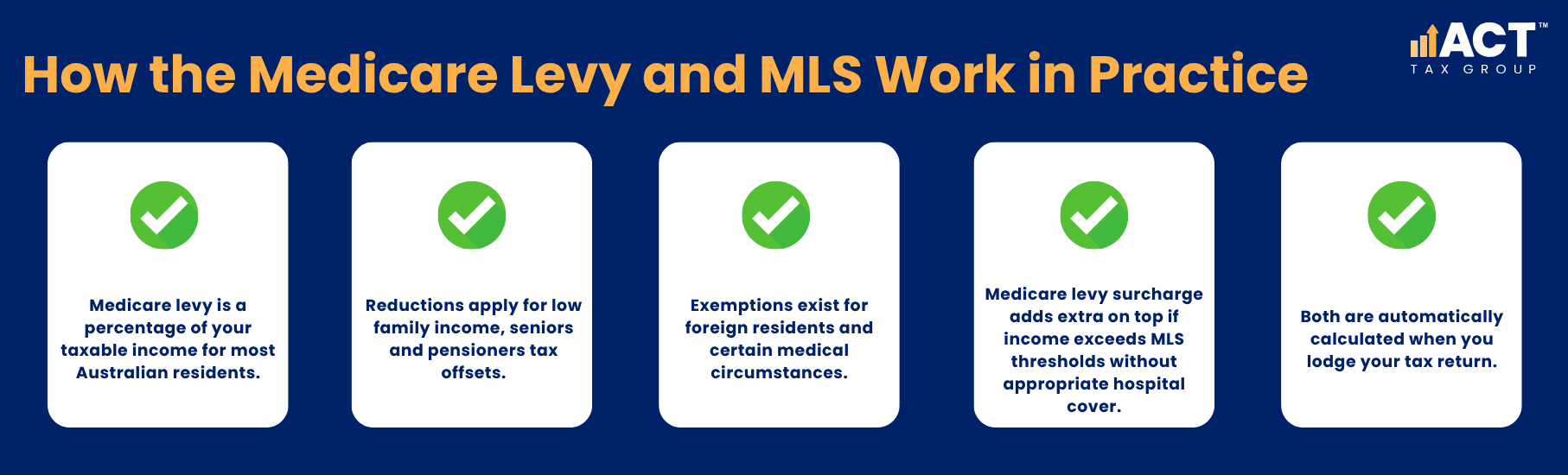

The Medicare levy is a percentage of your taxable income that most Australian residents pay to support Australia’s public health system. For most taxpayers this levy is simply part of their overall tax and is included when you calculate how much you need to pay each financial year.

It is tied to your taxable income and can be reduced or waived in certain cases, such as low family income or some seniors and pensioners tax situations. But for many high‑earning electricians, the levy itself is not the problem: the surcharge is.

What the Surcharge Adds On

The MLS is an extra amount that may apply if your income for MLS purposes goes over set income thresholds and you do not hold appropriate level private patient hospital cover. It is aimed at higher incomes and designed to encourage people in that group either to hold private health cover or accept an extra charge if they do not.

This surcharge is worked out using your income for MLS purposes, which is not always the same as taxable income and can include items such as reportable fringe benefits, reportable employer super contributions, net investment losses, and in some cases exempt foreign employment income. For electricians whose income has grown quickly, this is often the missing piece that explains why they suddenly pay more tax than in previous years.

Income Thresholds and How the Surcharge Purposes Test Works

Once your business is doing well, the income thresholds for the surcharge are what determine whether MLS applies to you at all, just as understanding instalment activity statements and PAYG reporting helps you stay on top of other ATO obligations.

The Australian Taxation Office looks at your income for MLS purposes, not just your basic wages, so the numbers can climb faster than you expect once the business is healthy.

Why Income for MLS Purposes Matters

For surcharge purposes, the Australian Taxation Office looks at your income for MLS purposes, which includes your taxable income plus certain reportable super contributions and other items. If you are single, the surcharge may apply once your income moves over the base threshold for that income year.

This means that even if you feel like your cash is going straight back into the business, the system may still treat you as a higher income earner for MLS purposes, particularly once you factor in regular BAS and GST reporting obligations for your business.

Families and Dependent Children

For families, the combined family income is used, and the family threshold increases by $1,500 for each MLS dependent child after the first. A strong year in the business for you or your spouse can push the family into a higher tier.

These thresholds are set each financial year and are listed clearly on the ATO website. If your income for MLS purposes is under the base income thresholds, the MLS does not apply. If your income sits in one of the higher bands, you may have to pay the surcharge at a rate that increases as your income rises, which makes it even more important to avoid common tax deduction mistakes that can distort your true position. That is why a strong year of jobs can move you from “no surcharge” to “pay MLS at a higher rate” without you changing anything about your health insurance cover.

How Is Medicare Levy Calculated for Busy Electricians?

Most electricians just want to know what the numbers mean in practice and where they can and cannot make a difference, especially when lining up MLS with broader tax‑savvy strategies to boost profits.

The levy and surcharge work together, but they have different rules, reductions and exemptions depending on your situation, much like the distinct rules around ASIC late fees and penalties for companies that can also affect your overall compliance costs.

The Core Medicare Levy

The Medicare levy itself is calculated as a percentage of your taxable income, with some reductions and exemptions based on family income, seniors and pensioners tax rules and certain personal circumstances. There can be a reduced rate or full exemption for eligible seniors, pensioners or people with lower family income, which is where terms like seniors and pensioners tax offset or pensioners tax offset can come into play.

If your income is higher, you generally pay the full levy unless you fall into a specific exemption group. For an active electrician in their main working years, this usually means the full standard levy is part of your normal tax, alongside obligations like PAYG instalments and their consequences if missed.

Exemptions and Reduced Rates

Some taxpayers can also qualify for a Medicare levy exemption or pay a reduced rate if they meet specific exemption means tests. This can include being a foreign resident for tax purposes or having exempt foreign employment income in some situations.

The MLS is then calculated on top, using your income for MLS purposes and your private health cover status. If you hold an appropriate level of private patient hospital cover for yourself, your spouse and your dependants, you generally won’t pay MLS for the days you were appropriately covered. If you do not, and your income passes the thresholds, you pay the surcharge at the relevant rate. Both the levy and the surcharge are included when you lodge your tax return and are automatically calculated based on the information you and your fund provide.

Why Private Health Insurance and Hospital Cover Matter for MLS

For many high‑earning electricians, the main choice is whether to pay MLS or take out suitable private hospital cover instead.

The surcharge is one of the few parts of your tax bill you can influence by changing your cover, as long as you understand the rules and how they apply to you and your family.

Avoiding Paying MLS

To avoid paying the Medicare Levy Surcharge, you need an appropriate level of private hospital insurance that meets clear criteria. It must be private patient hospital cover (not extras‑only cover) and must apply to you, and where relevant your spouse and dependent child or children, for the full income year or part of it if you only need relief for some months.

If you are a high‑earning electrician with a strong annual income and no private health cover, the result is that you may have to pay MLS on top of your normal tax and Medicare levy. For some sparkies, that total can be more than the cost of suitable cover, which is why it is worth running the numbers.

What Does Not Count as Appropriate Cover

Extras such as dental, physio or optical on their own do not count as appropriate hospital cover for MLS purposes. The cover must be an appropriate level of private patient hospital cover. Extras-only cover, travel insurance and cover from an overseas fund do not count for MLS purposes.

If you have private health insurance but are unsure whether it counts as appropriate hospital cover, you can check with your health insurance fund or use calculator tools and guidance on the ATO website and Services Australia pages to estimate your position. For many electricians, the best step is to review their financial situation with a professional before the income year ends so they can decide whether to pay MLS or adjust cover, and to confirm whether methods like the fixed rate method for work‑from‑home deductions are relevant to their overall tax planning.

Special Cases: Exemptions, Foreign Residents and Personal Circumstances

Not every electrician fits the same pattern, and some situations change how much levy or surcharge you must pay.

Your residency status, medical requirements, age and family situation can all affect whether a reduction or exemption applies.

When You Might Be Exempt

Some taxpayers can claim a Medicare levy exemption or a reduction if they meet specific conditions. For example, a foreign resident for tax purposes during all or part of the income year may be exempt, just as property owners who move into short‑term rental accommodation arrangements and face CGT implications need to consider how their changing circumstances affect overall tax outcomes.

Someone with certain medical requirements may qualify for a Medicare entitlement statement that confirms they were not entitled to Medicare benefits for a period and can claim an exemption for that time. In those cases, the levy or surcharge may be reduced or not applied for the relevant part of the year.

Seniors, Pensioners and Families

Pensioners, some seniors and certain other eligible taxpayers may also qualify for a reduced rate or a full reduction of the levy based on their family income and seniors and pensioners tax rules. If you are an electrician who has recently become a pensioner, or you share income with a partner who is a pensioner, it is important to check how seniors and pensioners tax offsets, Family Tax Benefit Part A entitlements and related rules impact your Medicare levy and surcharge.

The key is not to assume you are exempt, but instead to check the criteria on the ATO website or speak with an advisor so your tax return reflects your true position.

Step-by-Step: What to Do Before You Lodge Your Tax Return

A simple yearly checklist can keep the Medicare levy and surcharge from becoming a nasty surprise.

If you follow these steps before the end of each financial year, you will have a much clearer view of what you are likely to pay.

Check Your Income and Thresholds

First, estimate your income for MLS purposes by starting with your taxable income and then checking any relevant add-backs, such as reportable fringe benefits, reportable employer super contributions, net investment losses, and, where relevant, exempt foreign employment income. Use this to work out your likely income thresholds tier and whether the Medicare Levy Surcharge applies at all, while also checking that your GST credits and BAS claims are accurate and ATO‑compliant.

This is where good bookkeeping, up‑to‑date accounts and efficient use of ATO online services for business make a real difference, because you can see issues early and not just when the return is due.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

Review Your Cover and Possible Exemptions

Second, review your health insurance cover to confirm whether you have private patient hospital cover at an appropriate level for the full year or part of it, and whether your spouse and dependants are also covered. Make sure you know whether your policy is hospital, extras, or a mix.

Third, check whether any exemptions or reductions could apply to you, such as being a foreign resident for part of the year, having a Medicare entitlement statement due to lack of access to Medicare benefits, or qualifying for seniors and pensioners tax relief.

Lodge With Accurate Information

Finally, when you lodge your tax return, make sure your health insurance and income details are correct so the amounts the system calculates are accurate. If anything is unclear, using a clear guide on how to apply for a tax return in Australia can help you understand each step before you rely only on the automatically calculated figures.

A short chat with an accountant who understands MLS can often clear up questions that might otherwise drag on for years.

Getting Help from a Team That Understands Sparkies

Electricians deal with enough risk on site without needing surprise tax bills on top. Getting clear, simple advice helps you stay on top of MLS while you focus on running jobs and leading your team.

You do not need to become an expert in tax law; you just need the right structure, clear records and someone who can translate the rules into action for your business.

Why Support Matters

Working with an accounting team that understands how income, family income, cover and exemptions all interact means you can treat the Medicare levy and Medicare Levy Surcharge as predictable parts of your overall tax picture. That reduces stress and lets you plan your financial year with more confidence.

We can help you calculate likely outcomes for the current income year, review whether your private health insurance meets the appropriate level criteria and make sure your tax return reflects your real situation, so you do not overpay or miss out on a legitimate reduction.

How ACT Tax Group Can Help

At ACT Tax Group, we work with electricians across the ACT who want straight answers and clear steps. Our focus is on helping you keep compliant, protect your cash flow and avoid avoidable surprises from Medicare levy and MLS.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)