Claiming Home Office Expenses as an Australian Electrician: What Can You Deduct?

Published on March 23, 2026

Claiming home office expenses as an Australian electrician can help bring down your tax bill, but it only works if your claims are tied to real work and solid records. When most of your days are on the tools and nights are spent quoting, invoicing and chasing payments from a home office, you want clear rules, not guesswork.

How Home Office Deductions Work for Electricians

For most electricians, a home office is a spare room or a small, dedicated home office space where you handle quotes, supplier emails, ServiceM8 or SimPRO, payroll and tax return prep. You are allowed to claim home office expenses for the work-related portion of your home office running expenses, but you cannot turn general home expenses into business costs just because you sometimes answer a work call on the couch.

The key idea is simple: you only claim expenses that relate to your work and only for your work-related proportion. That means you cannot just guess a percentage and hope it sticks. If you use the fixed rate method, keep a record of all hours worked from home for the entire income year. Estimates are not accepted.

Unsure how much you can really claim for your home office?

Schedule a complimentary consultation with us today to clarify fixed rate versus actual cost for your electrical business.

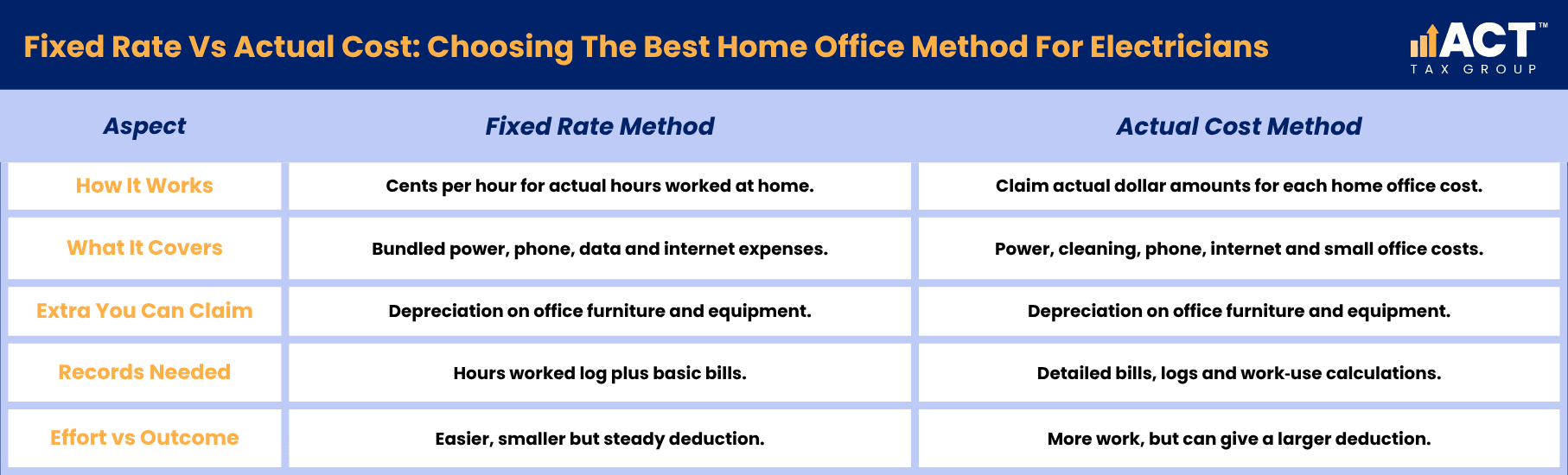

Fixed Rate Method: Simple Working from Home Expenses

The fixed rate method is often the most practical way for a busy electrician to claim home-based business running expenses. For the 2024–25 income year, the ATO’s fixed rate for eligible sole traders and partnerships is 70 cents per hour. Before lodging, check the rate that applies for the income year you are claiming.

This revised fixed rate method for claiming work-related home office deductions covers common running expenses such as electricity bills, energy expenses for heating and cooling, phone expenses, mobile phone expenses, mobile internet, data expenses, and internet expenses. Because these are bundled into the cents per hour rate, you usually cannot make separate claims for the same running expenses again in your tax return.

What You Still Claim Separately Under Fixed Rate

Under the fixed rate method, you may still separately claim the business-use portion of depreciating assets and equipment, such as office furniture, screens, printers, laptops and phones, and in some cases their repairs and maintenance.

These items are often claimed as decline in value over time, based on business use. However, if you are an eligible small business using the simplified depreciation rules, an immediate deduction may be available, including under the current $20,000 instant asset write-off rules where the conditions are met. You just need invoices, bank statements or other proof of the purchase, and a reasonable way to work out the work-related proportion.

Actual Cost Method: When You Want to Claim Actual Expenses

The actual cost method can suit electricians who want to calculate their real additional home-based business expenses in detail. A dedicated home office is not required, but stronger records are needed, and a dedicated area may matter for some claims such as cleaning or occupancy expenses. Instead of a simple cents per hour claim, you calculate actual expenses for each type of home office running expense and then work out the work-related portion. Under this method, you might claim:

Additional running expenses for electricity and gas in your home office

Cleaning costs for a dedicated home office area

Phone bills and internet bills, based on how much of your mobile phone and monthly internet bill relate to work

Office expenses such as computer consumables, diaries and small office supplies

You only claim the work related proportion, which might be based on floor area for a separate home office, or on usage logs and itemised phone accounts for phones and internet. This method can produce higher home office deductions in some cases, but only if your record keeping is strong and your numbers match your real work patterns, and you may find that using ATO online services for business makes managing these records and claims more efficient.

If you are a sole trader or partnership and have an area of your home set aside as a genuine place of business, the floor area method may also be relevant for some occupancy and running expenses.

What You Can and Cannot Claim as Home Office Expenses

It is important to know where the line sits between home office running expenses, occupancy expenses and private home expenses. Getting this wrong is where many home deduction claims fall over, often alongside other common tax deduction mistakes Australians make.

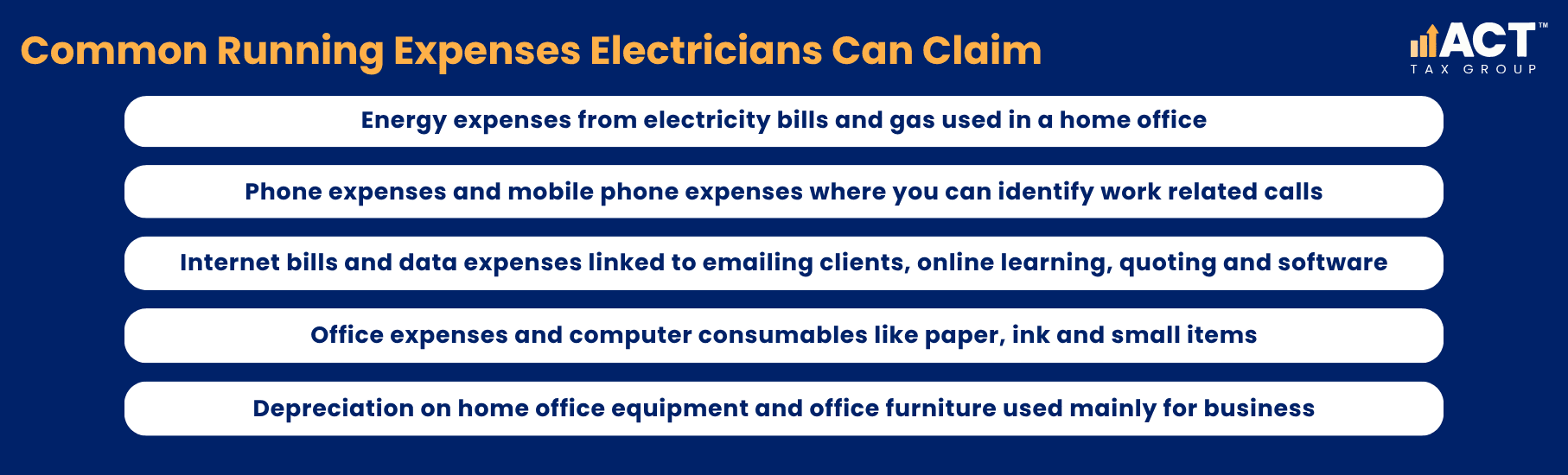

Common Running Expenses Electricians Can Claim

Most electricians can usually claim some of the following common running expenses, either through the fixed rate or actual cost:

These are tied to your home office running expenses, not to the cost of owning or renting the home itself.

Occupancy Expenses and Home Ownership Costs

Occupancy expenses are the costs of owning or renting the home itself. They can include rent, mortgage interest, council and water rates, land tax and house insurance premiums, but they are only deductible in limited circumstances where part of the home is a genuine place of business.

If you claim occupancy expenses, you are moving beyond basic home office tax deductions and into more complex home tax deductions. This can have flow‑on effects, such as affecting future Capital Gains Tax when you sell the property. Before you claim occupancy expenses, especially mortgage interest or land taxes, it is important to get advice that considers your personal circumstances as an electrical business owner, ideally through tailored accounting and tax services that understand trade businesses.

Phones, Internet, and Other Work-Related Expenses

As an electrician, your mobile phone is often your lifeline. You use it for quoting, chasing payments, scheduling jobs, talking to suppliers and checking plans. That is why mobile phone expenses and internet expenses are such a big part of home office tax deductions.

Phone and Data Claims for Electricians

When you claim mobile phone or phone expenses, the Australian Taxation Office (ATO) expects you to be able to identify work related calls. One common approach is to use itemised phone accounts for a sample period and work out how many calls are work related compared with private calls. You then apply that percentage to your total phone bills for the income year.

You can use a similar approach for data expenses and mobile internet. Look at how often you use your phone and internet for work tasks versus personal use. This helps you set a realistic work-related proportion that will stand up if the ATO checks your claim.

Internet and Online Work from Home

Your home internet is not just used for streaming and social media. You are also using it for email, job management software, tax return online lodgement, online learning and supplier ordering. You can claim a work related portion of your monthly internet bill by keeping a short log for a typical period and working out how much is work versus private.

Remember that if you use the fixed rate method, you may already be covering some of these internet and phone costs in your cents per hour claim. In those cases, you generally cannot make separate claims for the same expenses again. Keeping a simple spreadsheet that shows which claims fall under the fixed rate and which are separate claims for depreciating assets can help avoid double counting.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

Record Keeping So Your Home Office Tax Deductions Stick

The strongest home office deductions are backed by clear record keeping. The ATO places a lot of weight on whether your numbers are backed by actual hours, real bills and consistent calculations, especially when you claim home office expenses for the entire income year, whether you are an electrician or another tradie looking to maximise your trade tax deductions.

What Records an Electrician Should Keep

To support your home office tax deductions, it is worth getting into the habit of:

Tracking actual hours you work from your home office, using a diary, calendar or job software

Keeping copies of electricity bills, phone bills, internet bills and other home expenses you are using for claims

Keeping receipts, invoices and bank statements for office equipment, home office furniture and other depreciating assets

Keeping any logs or notes used to apportion costs, such as phone call counts or floor area calculations

This level of record keeping might feel like extra work at first, but it means you can claim tax deductions with confidence and avoid having to rebuild your evidence years later.

Why Getting Help Can Deliver Real Financial Benefits

Getting your home office tax right is not just about avoiding problems with the ATO. Done properly, it can deliver real financial benefits by reducing your tax bill in a way that aligns with your actual expenses and personal circumstances. When you claim expenses correctly, you keep more cash in the business to invest in staff, tools and growth.

If your electrical business operates through a company or trust rather than as a sole trader or partnership, different home-based business rules may apply, so it is important to get advice before claiming occupancy or other home-based business expenses.

If you are unsure which method to use, whether you can claim occupancy expenses, or how to claim depreciation on home office equipment, it is worth speaking with a tax adviser who understands electrical businesses, such as the ACT Tax Group team of specialist small-business accountants. The rules around home office, home office tax and working from home expenses are detailed, and the right approach depends on your structure, home set‑up and long‑term plans.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)