Capital Gains Tax Explained for Arborists: From Selling Equipment to Property

Published on April 21, 2026

Capital Gains Tax Explained for Arborists: From Selling Equipment to Property becomes very real when work slows down, bills keep coming, and you start looking around the yard asking what you can sell to get through the next few months. You may be thinking about selling assets like a chipper, a truck, or even a property, but you are not sure how capital gains tax is calculated or how much you might end up paying out of the profit.

What Capital Gains Tax Means for Arborists

When you hear people talk about “gains tax” or CGT, they are talking about how the tax law handles profits and losses from certain assets acquired and later sold. For an arborist, this usually matters most when you sell property or other significant assets, rather than everyday small tools.

Unsure how much CGT you’ll pay on a sale?

Schedule a complimentary consultation with us today to estimate your capital gains accurately.

What Is a Capital Gain or Capital Loss?

A capital gain arises when the selling price or other capital proceeds from an asset is higher than what it cost you for tax purposes. The starting point is the cost base, which generally includes the purchase price and certain incidental costs such as legal fees and stamp duty on a property. If the capital proceeds are higher than this cost base, you have made a capital gain.

A capital loss occurs when the capital proceeds are less than the reduced cost base. In simple terms, you have sold the asset for less than it effectively cost you. This is called a capital loss, and it does not reduce your wages or business income directly. Instead, it can be used to reduce capital gains in the same financial year, and any net capital loss that remains can usually be carried forward to reduce capital gains in future years.

How Capital Gains Flow into Your Taxable Income

Capital gains are not a completely separate tax. They are part of your income tax situation. After you work out your capital gains and capital losses for the income year, you end up with a net capital gain or a net capital loss.

Your net capital gain is added to your assessable income and forms part of your taxable income for the year. If you are an individual, trust, or complying superannuation fund and you have owned the CGT asset for at least 12 months, you may be eligible for a CGT discount, subject to the rules.

If you have a net capital loss instead, it is not used against wages or normal business income. Instead, it can be carried forward to offset capital gains in future income years, provided the rules are met.

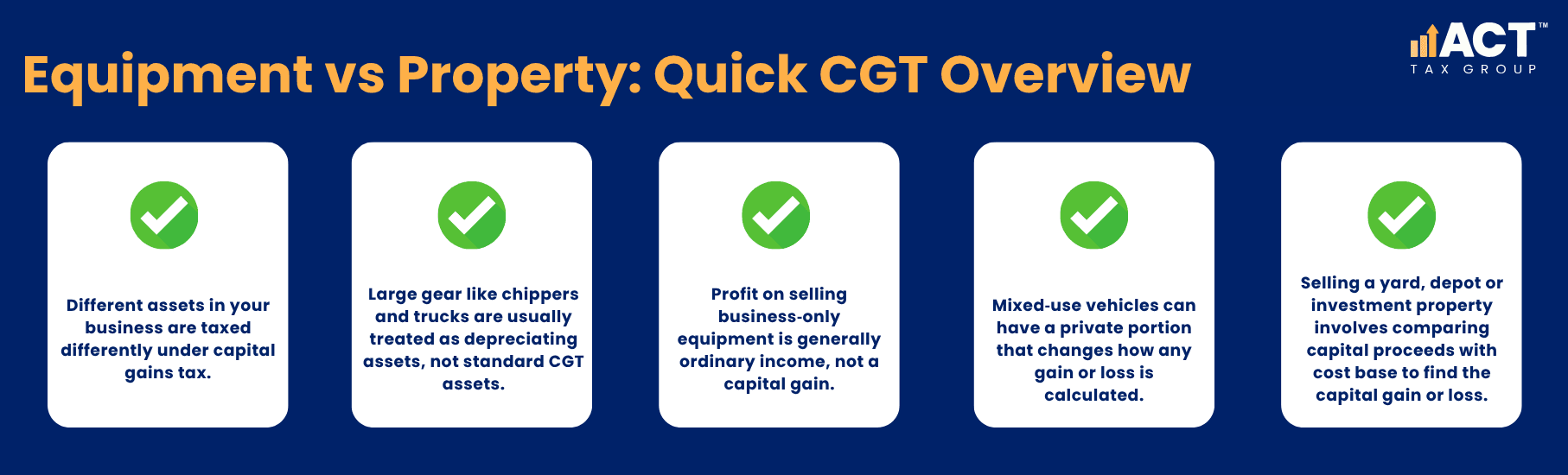

Equipment vs Property: Not All Assets Are Treated the Same

When you look at your business, you have a mix of assets: heavy gear, vehicles, and property. The way capital gains tax applies will vary depending on the type of asset, how it is owned, and how it has been used.

Selling Equipment Used in the Business

Most larger pieces of gear are depreciating assets. If an asset has been used wholly for taxable business purposes, any difference between its termination value and adjustable value is generally dealt with as a balancing adjustment in assessable income or as a deduction, rather than under the CGT rules.

In other words, you still may need to pay tax on that amount, but it is not counted in the same way as a gain on property. If you have used a vehicle for both business and private driving, the personal use assets portion can affect how any gain or loss is treated, so keeping good usage records is important.

Selling a Yard, Depot or Investment Property

A different story applies when you sell property, such as a yard, depot or investment property. Here you are firmly in capital gains tax territory.

When you sell a property, you first need to know your cost base. This usually starts with the purchase price you paid when the asset was acquired. You then add eligible incidental costs such as legal fees and stamp duty, along with some other costs depending on the rules. The capital proceeds will generally be the selling price under the contract, and the CGT event usually happens on the contract date, not settlement.

Once you subtract the cost base from the capital proceeds, if the result is a gain, that is your capital gain before any CGT discount or other adjustments. If the result is a loss, you have a capital loss. These figures are then used to calculate how much CGT you might pay, once all your gains and losses on other assets for that year are taken into account.

Special Situations: Homes, Inherited Assets and Exempt Assets

Some assets are treated differently to support basic living needs and certain life events. For an arborist, that usually shows up when your family home or inherited assets are involved.

If a property is your main residence, there may be a full or partial exemption. Using part of the home for business can affect the exemption especially where an area is set aside exclusively as a place of business and occupancy expenses are claimed. The same goes if the property has been used as a dedicated business depot, or if it has been converted into short term rental accommodation.

Inherited Assets and How They Are Treated

If you have inherited property and other assets, rules exist to work out the cost base and timing of the CGT event. In some cases, an exemption can apply if conditions are met. Whether you need to pay capital gains tax when you eventually sell will depend on how the asset has been used since you inherited it, and how the law applies to your specific case.

It is important to remember that rules around exempt assets, the family home, and inherited assets are detailed. This is where you should seek expert advice before signing a contract so you can make informed decisions that match your goals and your financial situation.

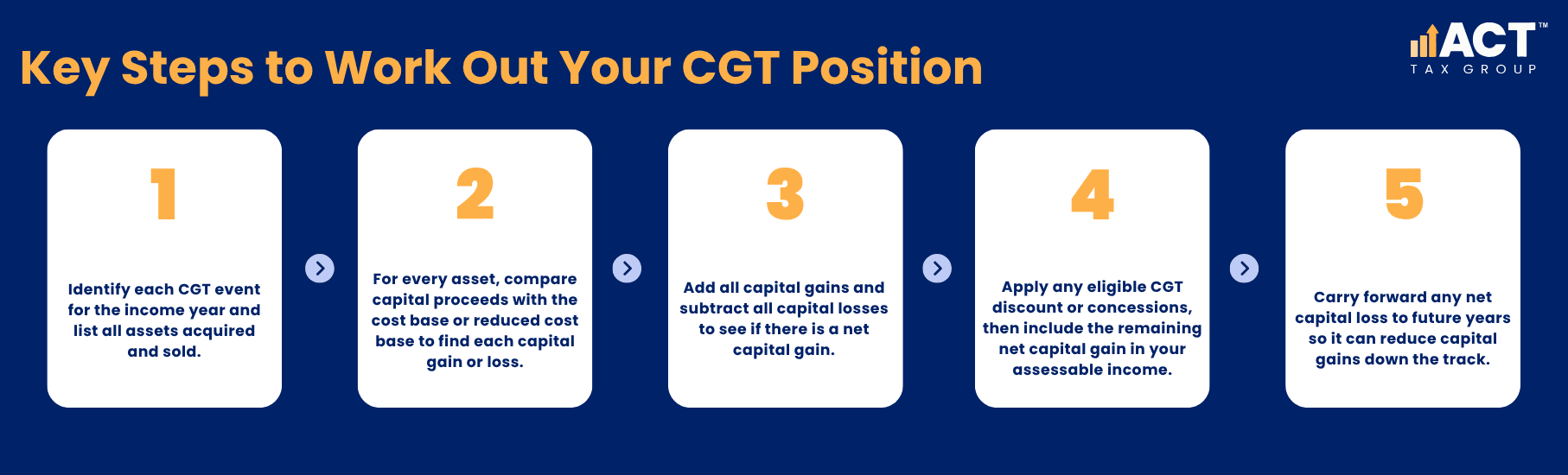

How Capital Gains Tax Is Calculated in Practice

When you sit down with your accountant at the end of the financial year to review your overall tax return position, they do not simply plug numbers into a capital gains tax calculator and call it a day. They follow a series of steps, so your tax obligations are handled correctly.

From Capital Gains and Losses to Your Taxable Income

First, they identify each CGT event for the income year. This covers assets acquired and later sold such as properties, some business assets, and other investments. For each asset, they work out the capital gain or loss by comparing the capital proceeds with the cost base or reduced cost base.

Next, they add up all your capital gains and then subtract any capital losses for that year. If you have a net capital gain, they apply any relevant CGT discount or concessions if you meet the eligibility criteria. That remaining amount becomes your net capital gain, which is included in your assessable income. It then combines with your other income to determine your taxable income and how much you pay tax overall.

If instead you have a net capital loss, it is not used against wages or business profit. It is kept and carried forward into future years to reduce capital gains down the track. Your tax return will reflect these details so that the systems at the Australian Taxation Office show your position clearly for that year. This is the core of calculating capital gains tax. There is no magic behind it, just a structured process, based on contracts, numbers, and the rules on the ATO website.

Why Arborists Should Plan Ahead Before Selling Assets

For many arborists, the decision to sell gear or property is driven by pressure in the moment – quiet months, rising expenses, and stress, rather than longer term cash flow planning for arborists. But how much CGT you might pay can vary depending on timing, how long you have owned the asset, whether you have carried forward losses from previous years, and how the asset has been used.

This is why it helps to plan ahead. Before you decide to sell a property or trade in a big piece of equipment, it is worth sitting down with someone who can give you clear, factual tax advice, not just a rough estimate from a calculator. Together, you can look at how the sale will interact with your current taxable income, whether you have any carried-forward capital losses, and what the timing of the sale may mean for your broader financial position.

Instead of guessing how much CGT you might pay, you can work with estimated results that are based on your actual numbers. That allows you to make more informed decisions about whether to sell now, wait until a later income year, or explore other options that do not involve selling a key asset at the worst possible time.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

How ACT Tax Group Supports Arborists with CGT and Asset Sales

As an arborist, your strengths are in managing crews, doing safe work, and keeping clients happy, not in checking every rule on the ATO website. That is where we come in.

At ACT Tax Group, we sit alongside arborists to help them understand the tax side of profit from selling gear and property. We look at the way your equipment and properties have been used, how long you have owned them, which parts may be exempt, how you are using ATO online services for your business, and how any gain will feed into your tax position. We help you calculate what different options might mean in the current or future years, and we present it in simple terms so you can focus on running your business.

Our role is not to push complicated schemes, but to make sure your tax obligations are met, your tax return is accurate, and your decisions around selling assets fit your long‑term goals. That includes helping you manage related areas such as GST credits and ATO compliance, BAS and GST reporting for your business, and whether it makes sense for your turnover to stay under the GST registration threshold. That leaves you free to get back to what you do best, knowing that your CGT position has been thought through carefully.

Conclusion

Capital gains tax is not a separate tax but part of your overall income tax picture. When you sell significant assets such as a yard, depot or investment property, any capital gain or loss flows through to your assessable income under rules set by the Australian Taxation Office. The final result depends on your cost base, capital proceeds, timing, and how the asset has been used.

By keeping good records, planning before you sell, and getting the right tax advice, you can make better informed decisions about when and what to sell, how much you may need to pay, and how to keep your arborist business on stable ground through both busy and quiet seasons.

If you would like clear and practical support that speaks your language as an arborist, you can talk to ACT Tax Group about your next sale before you commit, so you understand the tax impact and feel confident about your next step.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)