What Plumbers Need to Know About Assessable Government Industry Payments

Share this article

Published on September 29, 2025

What plumbers need to know about assessable government industry payments starts with understanding how these amounts fit into your business income and affect your tax return. When you run a plumbing business, government grants and support payments can kick in at different times—whether it’s apprentice wage subsidies, fuel tax credits, or disaster relief assistance. Knowing which government payments are treated as assessable government industry payments versus exempt income or non-assessable amounts can save you from surprises at tax time and help you plan for quarterly instalments or your annual income tax return.

Government Payments That Count as Business Income

Plumbing businesses often receive a range of government payments designed to support specific activities or help cover costs. The key is to work out whether each payment feeds into your ordinary income or whether it can be treated as exempt income or a capital injection.

Are you unsure which government payments count as taxable income?

Schedule a complimentary consultation with us today to clarify assessable versus exempt payments for ATO compliance.

Apprentice Wage Subsidies and Other Grants

When you employ an apprentice, you may qualify for wage subsidies or training incentives under federal programs. These amounts are paid to help offset the costs of training and mentoring a new plumber, but they’re not a one-off handout. Under tax rules for small business entities, apprentice wage subsidies and similar grants count as other business income in the income year you receive them. You include them alongside fees for service in your net income, as they directly relate to carrying on a business.

If you receive a lump-sum government grant to purchase a depreciating asset—say, a new camera for leak detection or a van—you still recognise that payment as assessable income, even if you later claim depreciation deductions on the asset. The grant increases your capital assets, but you don’t exclude it from your income tax return just because it’s spent on equipment.

Fuel Tax Credits and Rebates

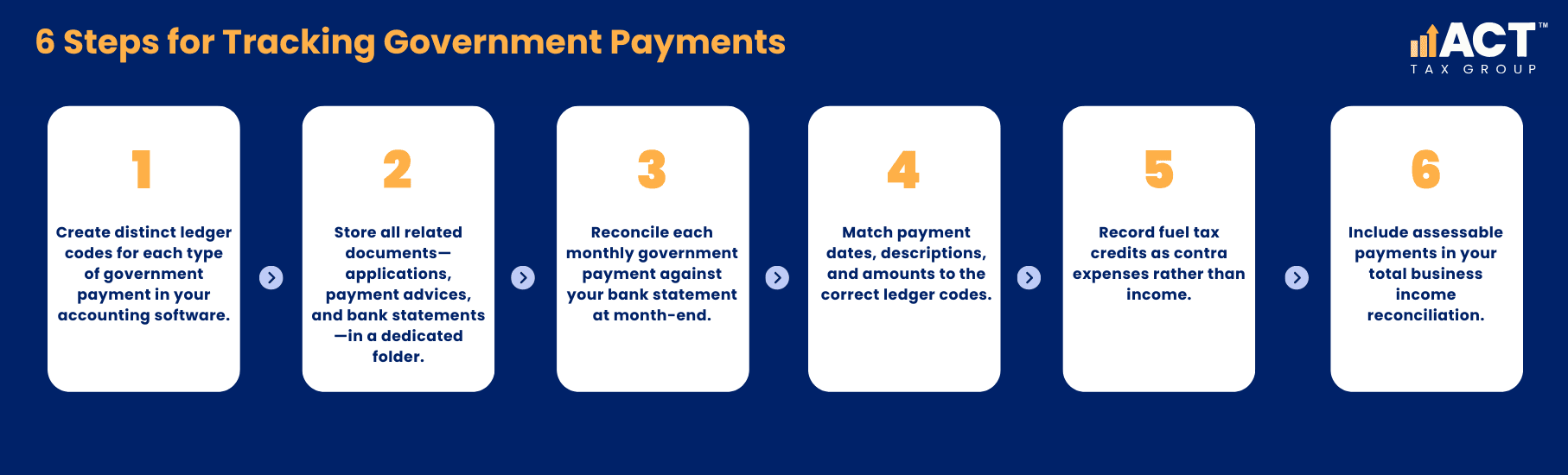

Fuel tax credits work differently from wage subsidies. Rather than paying you directly as income, the government refunds the excise or customs duty paid on fuel used for business activities. You claim fuel tax credits through your activity statement, offsetting them against the GST or PAYG instalments you owe. These credits don’t count as assessable income because they’re refunds of tax already paid on fuel for carrying on a business. However, they do reduce your net fuel expenses and should appear in your accounting records as a contra expense, not as a boost to gross income.

Disaster Recovery and Special Assistance Payments

From time to time, plumbing businesses may qualify for special assistance payments after natural disasters or during public health emergencies. Some of these payments are classified as non-assessable non-exempt income, meaning you don’t include them in your assessable government industry payments or other business income. Confirm the ATO’s ruling or the payment guidelines: if the assistance is genuinely relief-focused rather than income-support, it can be exempt income and won’t affect your income tax return.

How Assessable Payments Affect Cash Flow and Tax Planning

Failing to treat government payments as assessable can leave a plumbing business with a nasty tax bill when you least expect it. Here’s how to stay on top of those incoming funds.

Timing and Recognition in Your Financial Year

Most plumbing businesses use a cash-basis method for bookkeeping, which means you recognise income when it lands in your bank account. Government payments received before 30 June are assessable in that financial year. That’s true whether the payment relates to ordinary course business activities—like service fees and industry grants—or capital support for equipment purchases. If you get a payment in, say, July but it relates to June work, it’s still counted in the year it was paid, not the year it was earned.

Setting Aside Funds for Income Tax

When a government payment arrives, calculate your marginal tax rate and set aside at least that percentage of the payment into a separate “tax” bank account. For example, a $10,000 apprentice subsidy at a 30% tax rate means $3,000 should be reserved for income tax. That prevents you from spending the tax portion on trading stock, wages, or other business expenses and then chasing the money later.

Impact on Business Activity Statements

Even if you handle fuel tax credits separately, assessable government industry payments increase your total assessable income on your activity statement. Higher gross income can affect your PAYG instalments and GST obligations. It may also push your total turnover over thresholds that require additional reporting as a small business entity. Watch your running total and adjust your BAS projections accordingly.

Practical Record-Keeping for Government Payments

Good record-keeping underpins accurate tax preparation. It’s all too common for plumbing businesses to lump government payments into a catch-all category and then struggle to reconcile them come tax time.

Separate Coding and Documentation

Create dedicated ledger codes in your accounting software for each type of government payment—one for wage subsidies, one for training grants, one for reimbursed expenses, and so on. Store all application forms, approval letters, payment advices, and bank statements in one folder, whether digital or physical. That way, when your accountant asks for details about assessable income for your income tax return, you won’t have to hunt through invoices and receipts.

Reconciling Monthly Payments

Government payments often arrive as monthly payments. Reconcile these against your bank statements at month-end. Match the date, description, and amount to the ledger code. For fuel tax credits, reconcile the credit against the fuel expense code. For payments that boost gross income, include them in your reconciliation of total business income.

Avoiding Common Pitfalls

Even experienced plumbers can trip up when it comes to government payments. Here’s how to dodge the mistakes.

Treating Grants as Exempt Income

It’s tempting to think of grants and subsidies as funds you don’t have to include in your income tax return, especially when the paperwork labels them “assistance.” Unless the payment documentation explicitly states the amount is non-assessable non-exempt income, assume it’s assessable and include it in your ordinary income.

Skipping GST Checks

Most government payments don’t carry GST because they’re not payments for taxable supplies. However, if you receive a payment that is reimbursement for services you provided—such as a fuel purchase reimbursement from a local council—it may include GST. If in doubt, check the payment advice. Recording the wrong GST treatment can trigger BAS errors and overpayments.

Ignoring Capital Gains and Depreciation

If you receive a grant to upgrade a depreciating asset—like heavy-duty equipment—you record the payment as assessable income but then claim depreciation deductions on the asset’s cost, reduced by the grant amount. That increases your net cost base and lowers your depreciation deductions but ensures your income tax return shows the correct capital gains position if you ever sell the asset.

Integrating Government Payments into Business Planning

Government payments can provide a welcome boost, but they also need to be factored into your ongoing planning for sustainable growth.

Forecasting and Cash Flow Models

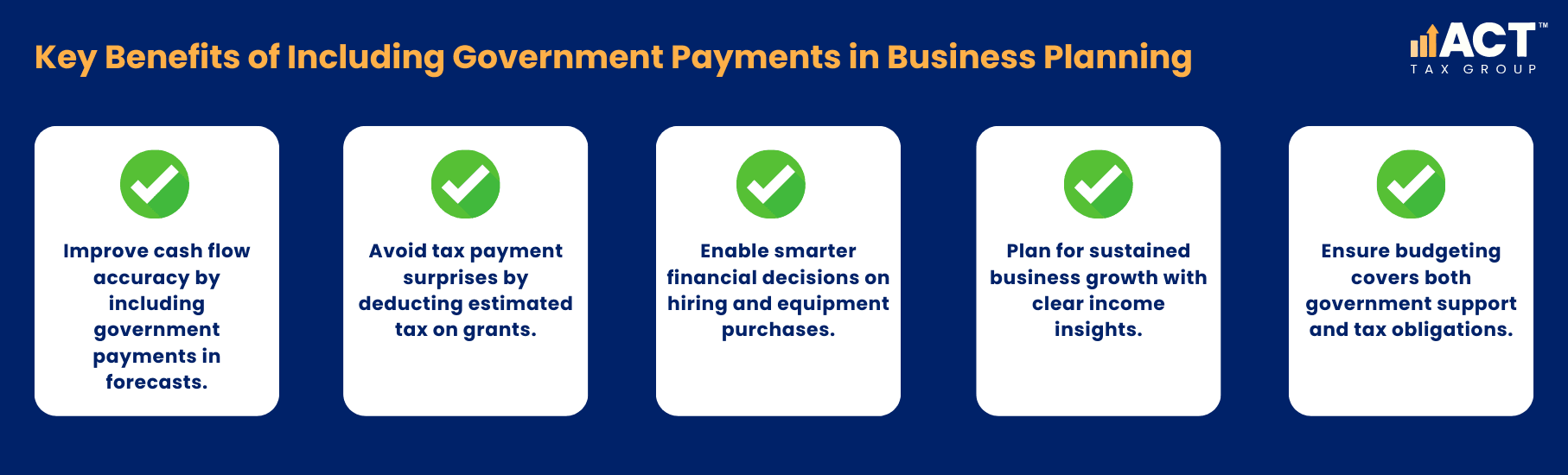

When building cash flow forecasts, include expected government grants and subsidies alongside revenue from contracts. Then deduct estimated tax on those payments and forecast the remaining available cash. This approach helps you avoid cash shortages when tax instalments come due and ensures you can budget for new tools, vehicles, or wage costs without surprises.

Decision-Making for Growth

Knowing which payments are assessable income or exempt income can influence decisions like hiring more apprentices, investing in new equipment, or expanding service areas. If you anticipate a capital grant to purchase a van, model the impact on both cash flow and your net income after tax. That analysis helps you make informed choices about whether to take on the grant or seek alternative financing.

Bringing It All Together

Assessable government industry payments are an essential part of a plumbing business’s financial picture. From apprentice wage subsidies to fuel tax credits and disaster relief grants, each payment type has its own tax treatment and cash flow implications. By treating government payments as assessable income unless explicitly exempt, keeping dedicated records, setting aside tax, and integrating these payments into your cash flow forecasts, you can avoid unwelcome surprises at tax time.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Share this article

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)