Accrual vs Cash Accounting: Which Method Suits Your Plumbing Business Best?

Published on September 22, 2025

Accrual vs cash accounting affects everything from your Business Activity Statement (BAS) lodgements to your business cash flow, yet many plumbing business owners aren’t sure which accounting method they’re using or whether they’ve chosen the right one. With feast-or-famine workloads, late payments from builders, and constant pressure to keep apprentices paid and suppliers happy, your choice between cash or accrual accounting can make the difference between smooth operations and sleepless nights worrying about money.

Why Your Accounting Method Choice Matters More Than You Think

Your accounting method isn’t just paperwork – it directly impacts when you pay taxes, how your BAS looks, and whether you have actual cash available when your apprentices need their wages paid on time.

Are unpaid invoices making your BAS harder to manage?

Schedule a complimentary consultation with us today to align your accounting method with your ATO obligations.

The Real Impact on Your Daily Operations

Small business owners often discover their accounting method choice affects everything from job pricing to equipment purchases. When you use cash basis accounting, you only record transactions when actual payments move in or out of your bank accounts. This means when you complete a hot water installation in June but don’t receive payment until August, that income doesn’t appear on your financial records until August under the cash method.

The accrual accounting method works differently by recording income when you’ve earned it and record expenses when you incur them, regardless of when actual cash changes hands. For plumbers, this means recording revenue as soon as you complete the job or send the invoice, even if payment comes weeks later.

How This Affects Your Tax Liabilities

Cash basis accounting lies in its simplicity for managing when you pay taxes. The cash basis method means you record revenue when customers actually pay their invoices, not when you send them. For Goods and Services Tax (GST) purposes, this means you only account for GST on the BAS covering the period when you actually receive payment for your jobs.

Under the accrual method, you must report GST on all sales during the BAS period, even if customers haven’t paid their invoices yet. This can create business cash flow challenges because you might owe GST to the Australian Taxation Office (ATO) before you’ve received payment from your customers.

Finding the Right Accounting Method for Your Plumbing Business

Choosing between cash and accrual accounting depends on your business size, customer mix, growth plans, and cash flow patterns. Each method creates different advantages depending on how your business actually operates day-to-day.

When Cash Accounting Works Best

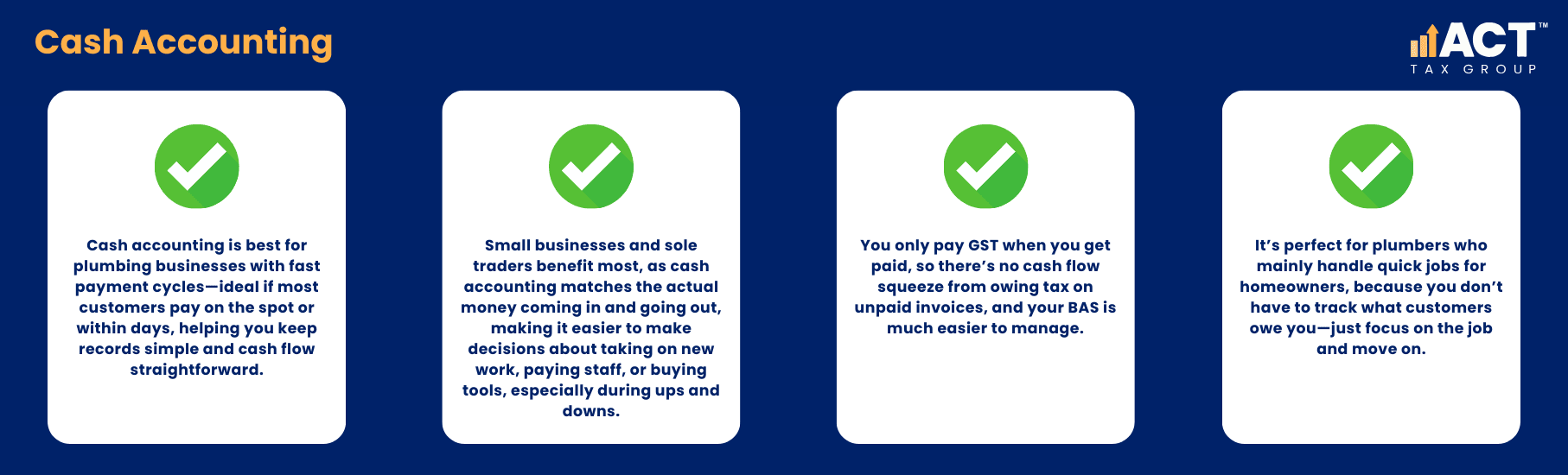

Cash accounting works particularly well for plumbing businesses with quick payment cycles and straightforward operations. If most customers pay straight away or within a few days of job completion, cash basis accounting keeps your record keeping simple and your cash flow predictable. Very small businesses and sole traders often benefit from cash accounting because it matches their actual cash position, helping with decision-making about taking on additional work, paying apprentices, or investing in new equipment during feast-or-famine workloads.

The cash method provides significant GST advantages for plumbing businesses with irregular payment patterns. You only pay taxes to the ATO after you’ve received payment from customers, which helps avoid the cash flow squeeze that comes from owing GST on unpaid invoices. Cash transactions are easier to track, and you don’t need sophisticated accounting software to maintain accurate records, making it ideal for businesses that want to keep things simple.

For plumbing businesses working mainly with residential customers who pay promptly, cash accounting eliminates the complexity of tracking accounts receivable. The method suits businesses where most financial transactions involve immediate payment, such as emergency repairs or maintenance work quoted and completed on the same day, allowing you to focus on the job rather than complex bookkeeping requirements.

When Accrual Accounting Provides Better Control

Accrual based accounting becomes more valuable as plumbing businesses grow in size and complexity, particularly when working with commercial clients, builders, or on larger residential projects with extended payment terms. If your plumbing business regularly invoices work with 30, 60, or 90-day payment terms, the accrual system provides a much more accurate picture of your business’s finances by showing total committed income rather than just cash received.

Plumbing businesses with multiple crews, apprentices, and subcontractors often find accrual accounting helps with budgeting and planning because it matches revenue and expenses with the accounting period when work was actually performed. This becomes important for job costing, profitability analysis, and understanding which types of projects generate the best returns, especially for commercial plumbing operations working on long term contracts.

Accrual basis accounting follows generally accepted accounting principles and provides advantages when applying for business financing or working with investors. Banks and lenders typically prefer accrual-based financial statements because they show committed income and outstanding obligations through accounts payable and accounts receivable, giving them a better view of your true financial position than cash accounting alone.

How Each Method Affects Your BAS and GST Management

Your accounting method choice directly affects how you prepare quarterly BAS returns and manage GST obligations. Understanding these practical implications helps avoid surprises and cash flow problems during BAS periods.

Managing BAS Under Cash Accounting

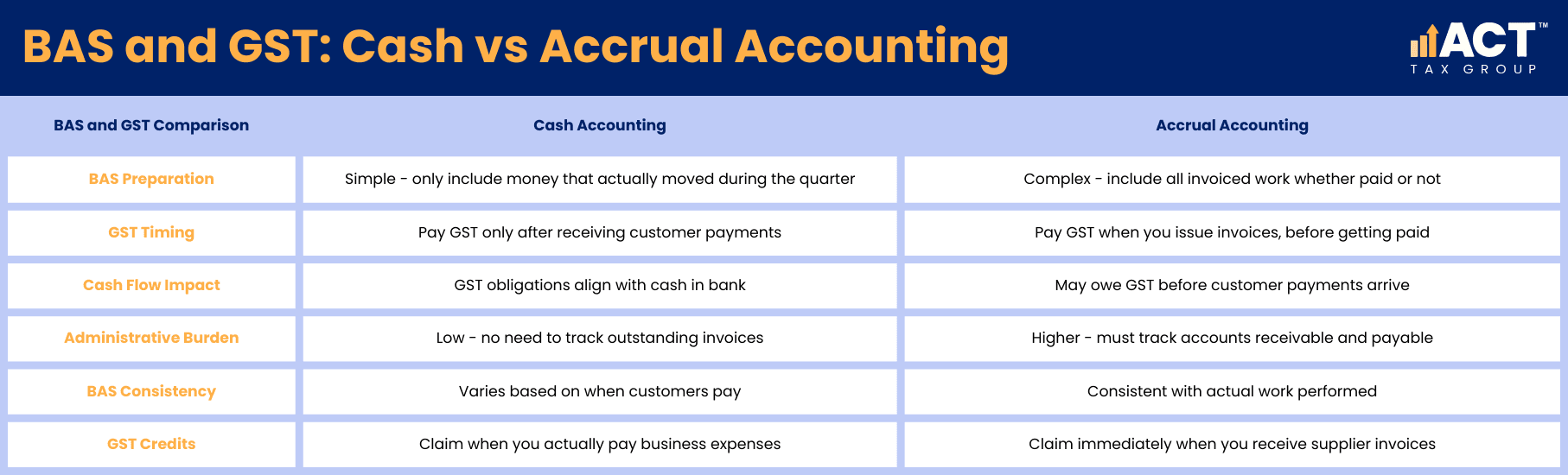

Cash accounting simplifies BAS preparation because you only include business transactions where money actually changed hands during the BAS period. This approach aligns your tax liabilities with your actual cash position, making it easier to pay BAS amounts when they’re due.

If you collected $2,000 in GST from customers and paid $800 GST on business purchases during the quarter, you owe $1,200 to the ATO – and you’ve already received the customer payments to cover this amount. Cash basis method also reduces the administrative burden of tracking what customers owe you and what you owe suppliers for GST purposes.

However, cash accounting can create timing variations in BAS amounts depending on when customers pay their invoices. A quarter with several large customer payments might show high GST obligations, while a quarter where customers delay payments might show lower obligations despite similar work levels.

Handling BAS Under Accrual Accounting

The accrual method requires more careful BAS management because you must pay GST on invoiced work regardless of whether customers have paid. For plumbing businesses with net 30 or net 60 payment terms, this can create significant cash flow challenges during BAS periods.

Under accrual accounting, your quarterly BAS includes GST on all invoices issued during the quarter, even if customers haven’t paid yet. This means you need separate cash flow management to ensure you have funds available to pay GST obligations before customer payments arrive.

The advantage of accrual BAS reporting is more consistent GST obligations that match your actual business activity level. Instead of fluctuating based on customer payment timing, your BAS reflects the work you actually performed during each quarter. Accrual accounting also allows you to claim GST credits for business expenses as soon as you receive invoices, even if you haven’t paid them yet.

Making Smart Decisions About Your Business’s Future

Not all businesses fit neatly into one category, and as your business grows, you might find your needs change. The accounting method that works when you’re starting out might not suit your operations after adding employees and taking on larger commercial contracts.

Evaluating Your Current Business Situation

Start by analysing your typical payment patterns and customer mix over the past financial year. If most customers pay within two weeks of job completion and you primarily work on residential projects under $5,000, cash accounting likely provides the best match for your operations.

Small business owners working with significant commercial work, retainer arrangements, or regular monthly service contracts should consider whether accrual accounting provides better financial visibility. The key question is whether you need to track committed income and outstanding invoices to make good business decisions about your company’s finances.

Consider your current cash flow challenges and whether they relate to timing mismatches between work performed and payments received. If you frequently struggle to pay BAS amounts because customers are slow to pay invoices, cash accounting might reduce this pressure by aligning your tax obligations with actual cash receipts.

Understanding ATO Requirements and Making Changes

Review your aggregated turnover to ensure you’re eligible to choose your accounting method. Remember that businesses with turnover exceeding $10 million must use accrual accounting for GST, regardless of preference. Most plumbing businesses stay well below this threshold and can choose either method. Business owners need to understand that changing accounting methods can only happen at the start of a new financial year or tax year, so this isn’t a decision you can reverse quickly if it doesn’t work out as expected.

Your balance sheet needs matter when applying for loans or working with investors, as they often prefer the more comprehensive view that accrual accounting provides, showing both money owed to you and money you owe others. The matching principle under accrual accounting means you record revenue when you earn it and expenses when you incur them, even if the actual cash movements happen in different periods. Recording income and expenses consistently within your chosen method helps avoid complications during tax time and ensures your taxable income is managed properly.

Professional bookkeeping services become particularly valuable under accrual accounting because of the complexity involved in tracking outstanding invoices, prepaid expenses, and accrued expenses. Many plumbing businesses find the cost of professional support is offset by improved cash flow management and reduced ATO compliance risks. Understanding the key differences between methods and how they affect your specific situation helps you make informed decisions about your business’s financial management, saving time and money while ensuring your business’s finances accurately reflect your true financial health throughout each given period.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)