Bookkeeping Tips for Working with Contractors vs Employees in the Electrical Industry

Published on February 17, 2026

Bookkeeping Tips for Working with Contractors Vs Employees in the Electrical Industry starts with understanding whether a worker is an employee or an independent contractor, because that decision shapes your payroll, super, and tax obligations for the whole financial year.

Why Employee vs Contractor Matters

When you’re engaging workers, it’s tempting to rely on basic shortcuts like “they’ve got an ABN, so they must run their own business” or “they send me an invoice, so they’re a contractor.” The Australian Taxation Office doesn’t see it that way. For ATO tax purposes, start with the written contract and identify the legal rights and obligations it creates. If the worker and the business have comprehensively set out their relationship in a written contract that is not a sham and has not been varied or displaced by other legal rights, the ATO view is that the contract terms are determinative, rather than a general review of day-to-day conduct.

The ATO looks at the legal rights and obligations and then considers indicators such as control, ability to delegate, and who provides tools, because those indicators usually reflect what the contract requires and how the rights operate. Treat these indicators as part of a contract-based analysis, not as a checklist that overrides the contract. A worker who turns up when you tell them, uses your tools, performs work side by side with your crew, and can’t send a replacement often looks more like an employment relationship than an independent contractor setup, no matter what you’ve written on the invoice.

Unsure how to handle PAYG and super when using both employees and subcontractors?

Schedule a complimentary consultation with us today to check EV eligibility and avoid surprise ATO bills.

Where Electrical Businesses Get Caught

The tricky part is that there’s no exhaustive list of rules that fits every job. The ATO and the courts focus on the terms of the contract. Subsequent conduct is most relevant where it shows the contract was varied, waived, or not followed, or where there is an issue such as a sham arrangement. Do not assume that day-to-day work patterns will override a comprehensive written contract for ATO tax classification.

That means even if your written contract says, “independent contractor,” the true nature of the relationship might still point towards a worker being an employee. The High Court guidance reflected in current ATO rulings is that labels are not determinative, and where parties have a comprehensive written contract that is not a sham, the classification turns on the legal rights and obligations in that contract. Practical performance matters mainly where it changes the contract or shows the contract is not operating as written.

For sparkies, the risk points include sham contracting (where someone is treated as a contractor but should be an employee) and missing super obligations for contractors who meet the tests for Super Guarantee in certain circumstances. Getting this wrong can lead to superannuation guarantee charge assessments, back payments, and a lot of clean-up work in your books.

Setting Up Your Bookkeeping for the Two Different Lanes

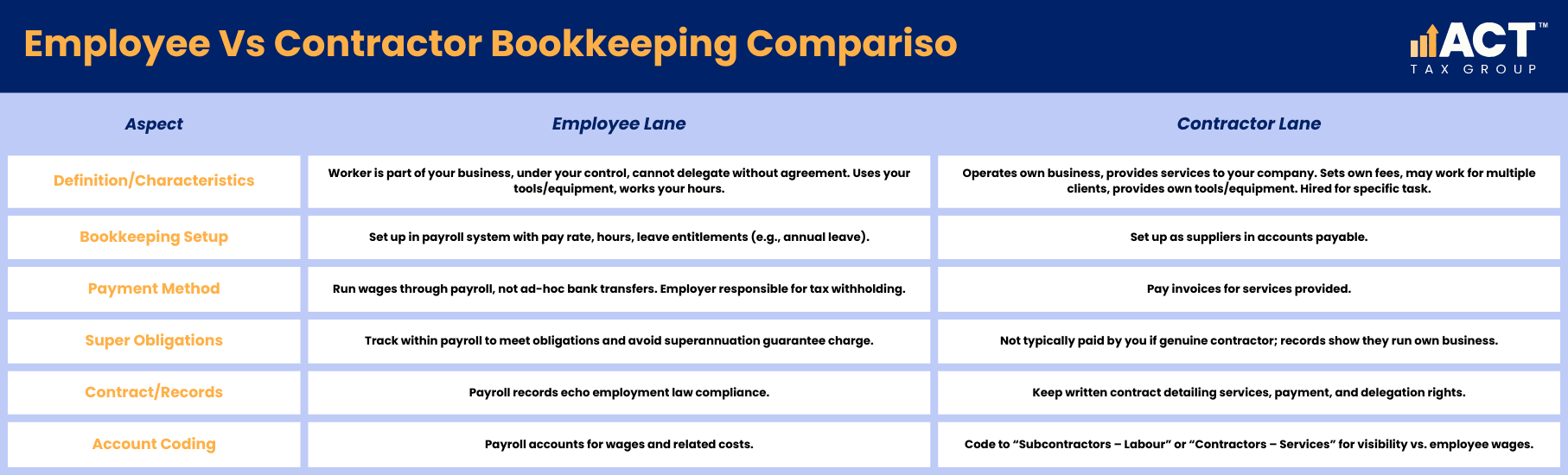

Once you’ve decided, based on the relationship test and ATO guidance, whether the worker is an employee or an independent contractor, your bookkeeping needs to follow two clear lanes. One lane is for employees where you run payroll, super, and leave. The other lane is for contractors where you pay invoices for services provided and record them as business expenses.

The key is that every person paid is set up correctly from day one. That way, when you reconcile the bank, run reports, or prepare for the end of the financial year, your numbers line up with your obligations. If the worker is an employee, treat them like one consistently. If they are a contractor running their own business and working for more than one client, your records should show that you are paying for services, not wages.

Employee Lane: Payroll, Leave, and Super

For employees, your bookkeeping should reflect that they perform work as part of your business and are under your control day-to-day. They usually cannot delegate their job to others, and they often use your materials, tools, and equipment.

Practical steps:

Put employees into your payroll system with clear details about hours, pay rates, and annual leave accruals.

Make sure super is tracked each pay run and calculated at the correct current rate. The SG rate is 12% from 1 July 2025. Also redesign your process for Payday Super from 1 July 2026 so contributions are paid on payday and received by the fund within 7 business days, subject to limited extensions.

Record all employee payments through payroll so STP reporting aligns with your general ledger. After year end, complete the STP finalisation declaration by 14 July each year so employees can access finalised information for their returns, or request a deferral if needed.

This lane suits workers where the nature of the relationship is clearly employment: you decide when and where they work, you provide the company equipment, and you’re responsible for tax, super, and leave.

Contractor Lane: Invoices and Subcontract Work

For contractors, you should be able to see that they operate their own business, charge their own fees, may work for more than one client, and often provide their own tools and equipment. In this lane, you pay for services provided under a contract rather than wages.

Practical steps:

Set each contractor up as a supplier so invoices sit in accounts payable, not payroll. Capture supplier details needed for compliance workflows, including ABN, GST status, and totals by financial year, so you can lodge a Taxable payments annual report when required. The TPAR is due by 28 August each year.

Make sure there is a written contract that clearly describes the specific task or services, including how they invoice and whether they can delegate.

Match each payment to a proper tax invoice that describes the job and any materials included, so you have a clear reference for what the payment covers.

This setup supports situations where the person is genuinely running a business of their own, such as a subcontract electrical company or a contractor who does personnel contracting across multiple builders.

PAYG, Super, and the Superannuation Guarantee Charge Risk

The big issue with mixing the lanes is that the ATO expects you to determine whether a worker is an employee or an independent contractor before you decide how to handle PAYG and super. If a worker is an employee, you are responsible for tax withholding and super. If they are a contractor, they usually manage their own income tax, but you still need to check for payer obligations. If the contractor does not quote an ABN and no exception applies, you generally must withhold at the top rate from the payment. Separately, you may still have super obligations for some contractors, including where the contract is principally for the person’s labor.

If you fail to pay required super, you can become liable for super guarantee charge. Under current law, ITAA 1997 section 26-95 denies an income tax deduction for SGC. From 1 July 2026, Payday Super legislation repeals section 26-95 and the new regime is designed so SGC becomes tax deductible, so do not rely on old deductibility assumptions when budgeting for late super.

That’s why it’s important to look beyond labels and think about the practical reality of the services provided. Ask yourself if the worker is really free to choose their own hours, hire their own people, and decide how to perform the work, or if it feels more like employees work under your direction.

If these factors lean toward employment, pause and reassess the classification using a contract-first review for ATO tax purposes. Also account for the increased after-tax cost of late compliance: from 1 July 2025, ATO interest charges incurred on or after that date are no longer deductible.

Job Costing When You Have a Mix of Workers

From a business perspective, you want to know if each job is making money. To do that, your bookkeeping needs to distinguish between employee labour and contractor labour for each client or project. Otherwise, you end up with one big labour bucket and no clear view of which jobs are actually profitable.

For employees, that means using your payroll system to track hours to jobs where possible, especially on larger projects. For contractors, that means coding each invoice to the right job and describing the services clearly. When you do this consistently, you can see whether bringing in extra contractors for a specific job protected your margin or just made the job look busier.

A simple example: two similar switchboard jobs, one done mostly by employees and one using more subcontract work. With clean records, you can compare labour costs for each and decide how to structure future work for that type of job.

Keeping Records That Match How You Actually Work

Good bookkeeping is less about complex law and more about setting up systems that match how your crews actually perform work on site. The Australian Taxation Office is interested in whether your records reflect what’s really happening, not perfect theory. So, if your working arrangements change over time, your records and contracts should keep up with that change.

Practical habits that help:

Keep all written contracts and key variation documents in one place, including any later written changes. For ATO tax purposes, this helps demonstrate the legal rights and obligations that govern the relationship, and whether they were varied over time.

Update your records if circumstances change. For example, if a contractor becomes more like an employee over time as their hours increase and they stop working with other clients.

Make sure each payment has enough detail attached to explain whether it relates to employment or services under a contractor agreement.

This is where the phrase “maximum extent permitted” often appears in contracts, but in reality, the way the parties perform the work and the legal rights and obligations that follow matter more than clever wording on its own.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

A Real-World Week Where This Matters

Imagine a busy week: you’re engaged on a light commercial job, you’ve got your core employees on site, and you bring in a contractor for a specific task on the switchboard upgrade. The contractor brings their own tools, quotes their own fees, and also works for other builders. Your employees work under your daily direction and use your materials and equipment.

If your records show:

Employees are on payroll, with hours, pay, and super tracked.

The contractor has a clear contract for services, invoices you for the specific task, and is coded as a contractor supplier.

Then, if the ATO or a union such as the Energy Union ever asks questions, you’ve got a clear picture of the relationships, payments, and obligations. The risk of a sham contracting claim is lower because your records support the real substance of how the people work and how you pay them.

Getting Help to Set This Up Properly

At ACT Tax Group, we help electrical business owners set up these lanes in their accounting software, refine their contracts and records to match the practical reality of each relationship, and keep an eye on super and tax obligations over the financial year. Our focus is on helping you record what’s actually happening on site so that, to the maximum extent permitted by law, your books are clean, your obligations are clear, and you can focus on running your business rather than worrying about what the Australian Taxation Office might decide later.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)