Should Australian Electricians Operate as a Company vs Sole Trader? Key Tax and Compliance Differences

Published on January 12, 2026

Should Australian Electricians Operate as a Company or Sole Trader? Key Tax and Compliance Differences often come into focus once you start hiring apprentices, buying utes, and turning over more than just a few small residential jobs each week. For many sparkies in the ACT, this question usually pops up after a stressful BAS period, a near-miss with an ATO deadline, or a sleepless night worrying whether the family home is on the line if something goes wrong on site.

When Structure Questions Usually Hit You

You rarely sit down and calmly decide “company vs sole trader?” at the perfect time. More often, it feels like this.

You have a small but busy Canberra-based electrical business, running as a sole trader business with an Australian Business Number. You have one apprentice, a couple of casual sparkies you call on, a ute on finance, and a mix of residential and light commercial work across ACT and nearby NSW. Things are busy, cash is lumpy, and you’ve just scraped through another BAS where GST, PAYG Instalments, and super payments all landed at once.

Right after you hit “lodge” on the BAS, an ATO letter lands asking for more detail on your deductions and reminding you about upcoming due dates. At the same time, a builder hints that the next contract will require a “Proprietary Limited Company” on the invoice and the bank wants to understand your business structure before extending your vehicle finance. That’s usually the moment you start asking: “Should I stay a sole trader or set up a company business structure?”

Should your electrical business stay a sole trader or become a company?

Schedule a complimentary consultation with us today to compare tax, PSI rules, and ATO compliance for your situation.

Core Tax Differences For Electricians

When you ask whether you should operate as a company or sole trader, what you really want to know is: what happens to tax, compliance, and take-home cash once your electrical business grows. This section breaks down how income tax, GST, and Personal Services Income rules interact with each structure for an electrician.

How Income Tax Works in Each Structure

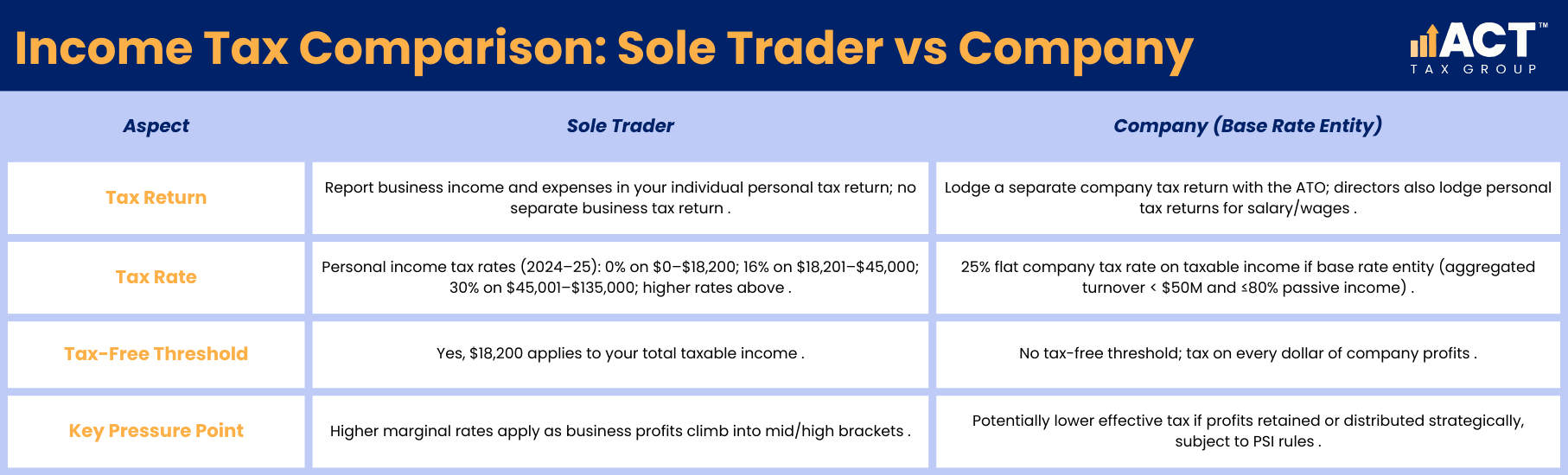

As a sole trader, all business income is simply part of your personal tax return, taxed at personal income tax rates for that year. You use your Australian Business Number, keep proper records, and report your business income and expenses in the business schedule of your personal income tax return, there is no separate business tax return.

As a company, the business is a separate legal entity and must lodge its own company tax return with the Australian Taxation Office. For the 2024–25 and 2025–26 income years, most small trading companies that are “base rate entities” pay a 25% company tax rate on their taxable income. A company is a base rate entity if its aggregated turnover is less than $50 million and 80% or less of its assessable income is passive income. Company directors still lodge a personal tax return to declare salary, wages, or other amounts received from the company.

For many electricians in the ACT bracketed around the middle to higher personal income tax rates, the key pressure point is when your business profits climb and you’re paying higher marginal tax as a sole trader compared to the company tax rate, even though the exact outcome depends on how you pay yourself and whether income is treated as business income or Personal Services Income. This information requires professional verification.

GST, BAS, And Day-To-Day Compliance

Whether you’re a sole trader or a company, GST registration for your electrical business follows the same basic threshold rules. The ATO states that you must register for Goods and Services Tax if your current or projected annual GST turnover is $75,000 or more, and you must register within 21 days of reaching this threshold. Before registering for GST, you need an Australian Business Number for the entity that is carrying on the business, either you as an individual (sole trader structure) or your company.

Once registered, both sole traders and companies charge GST on taxable supplies (for example, labour and materials on most electrical jobs), lodge Business Activity Statements (BAS) at the ATO-determined frequency (often quarterly for small trades businesses), and claim input tax credits for GST on eligible business purchases (for example, materials, tools, some vehicle running costs).

The difference in practice is administrative: with a company, you are now maintaining company BAS and GST records, a separate business bank account, and company payroll records if you pay yourself or others as employees, including Single Touch Payroll reporting. For a busy electrical contractor, this means more moving parts but also cleaner separation between personal and business assets when the bookkeeping is set up properly.

Personal Services Income (PSI) Pressure for Electricians

If most of your income comes from you personally doing electrical work, the ATO may treat that income as Personal Services Income, regardless of whether you are invoicing as a sole trader or through a company. The ATO describes PSI as income that is mainly a reward for an individual’s personal efforts or skills, rather than income generated from a business structure or business assets.

For sole traders, there are specific PSI rules that can limit deductions and affect how business income is reported where the income is PSI and you are not conducting a personal services business under the ATO tests. The ATO states that if PSI rules apply and you are not carrying on a personal services business, you cannot deduct certain expenses, such as rent, mortgage interest, rates or land tax for your home, or payments to your spouse (or associate) for support work.

For electricians operating through a company, the PSI rules can still attribute income back to you personally if the income is mainly for your own labour and the ATO tests are not met. This means that simply setting up a company does not automatically change how that income is taxed; the PSI rules can treat it as if it were earned directly by you as an individual. This information requires professional verification.

Risk, Asset Protection, And Legal Exposure

You don’t just worry about tax; you worry about what happens if something goes wrong on site, a serious fault, property damage, or an injury where fingers start pointing at you. Electricians carry more risk than many other small businesses, which is why the business structure question often becomes an asset protection question as well.

Liability Differences Between Sole Trader and Company

As a sole trader, there is no legal separation between you and the business; you are personally liable for all business debts and liabilities of the business. If the business cannot pay business debts, creditors can pursue your personal assets (for example, your home, personal savings) to settle business debts, subject to any consumer credit protections and bankruptcy law. This information requires professional verification.

In a company, the company is a separate legal entity and generally has limited liability, meaning shareholders are ordinarily liable only to the extent of any unpaid amount on their shares. Company directors can be personally liable in several situations, including where they provide personal guarantees on loans or where they are responsible for certain company obligations such as PAYG Withholding, net GST (from 1 April 2020), and Super Guarantee (from 1 April 2012) under the Director Penalty Regime. This information requires professional verification.

For an electrician with employees, vehicles, and higher-value contracts, operating through a company can provide an additional layer of separation between business operations and personal assets, although it is not a complete shield. This information requires professional verification.

Insurance, Contracts, And Perception

Builders, commercial clients, and government work providers often expect larger electrical contractors to operate through a company and hold appropriate insurances. In practice, some contracts and tenders specify that the contracting party must be a proprietary limited company and may require evidence of Workers Compensation Insurance, Public Liability, and Professional Indemnity where applicable.

While insurance, not structure, is your primary risk control for accidents and defects, some electricians find that operating as a company helps align with contract requirements and separates business finances and decision-making from personal finances. That said, structure alone never replaces the need for proper insurances and safety procedures for electrical work.

Compliance Workload and Admin Realities

You’re probably thinking: “I’m already drowning in BAS, STP, and super, will a company just make this worse?” The honest answer is that the compliance workload shifts rather than disappears, and the right business structure depends on how much admin you’re prepared to systemise.

What A Sole Trader Has to Keep Up With

As a sole trader electrician with an Australian Business Number and GST registration, your core compliance workload usually includes keeping detailed financial records of income and expenses (invoices, receipts, bank feeds, job management software export), lodging BAS at the required frequency (often quarterly) to report GST, PAYG Withholding if you have staff, and PAYG Instalments where applicable, lodging a single personal tax return each year, including your business schedule, and meeting tax and superannuation obligations and STP reporting if you employ staff or apprentices under the relevant award.

The upside is simplicity: one tax return, fairly straightforward bookkeeping if you have decent software, and less ASIC-level admin. The downside is that as the business grows, your personal tax return becomes more complex, and your unlimited personal liability remains high.

What A Company Has to Keep Up With

If you operate your electrical business through a company, the compliance picture changes shape: the company must lodge its own annual company tax return each year with the Australian Taxation Office, you still lodge a personal tax return to declare any salary, wages, director fees, or other amounts received from the company money, the company handles BAS, GST, PAYG Withholding, and super obligations for employees (including you where relevant), and the company must meet Australian Securities and Investments Commission obligations, such as paying an annual review fee, keeping company details up to date, and maintaining statutory registers, as required under the Corporations Act.

For an ACT electrical business with multiple employees, vehicles, and regular commercial contracts, a company structure tends to align better with the scale of operations, but it does require robust bookkeeping systems, a separate business bank account, clear separation of personal and business assets, and consistent compliance workflows. Company registration and ongoing costs are higher, but this suits businesses where the business grows and needs to raise capital or handle more complex business structures.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

How To Think About Your Next Step

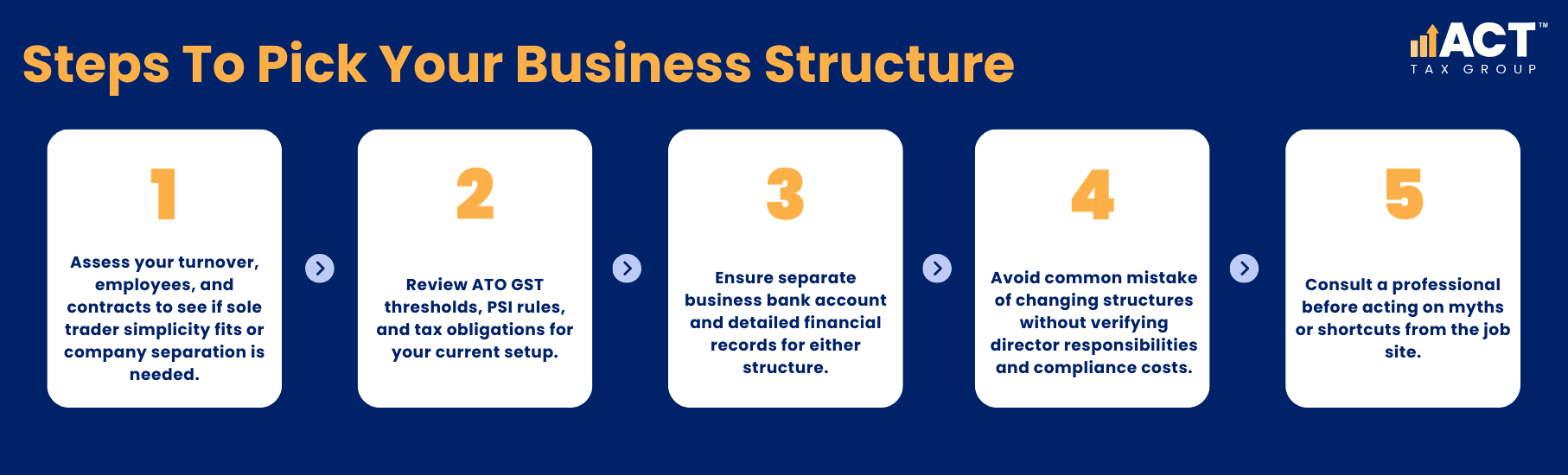

Standing back from the details, the business structure decision is really about matching the way your electrical business runs to the legal obligations the ATO and regulators already have in place. It is not about finding a shortcut; it is about choosing the right business structure that you can keep compliant without burning yourself out.

If you are an ACT electrician who is just starting out, doing most of the work yourself, and keeping turnover modest, staying as a sole trader may keep things simpler while you focus on building consistent work and getting your BAS and detailed financial records under control. If you have several employees or apprentices, regular commercial contracts, higher turnover, and worries about how much personal risk, a company may provide a clearer separation between business account and personal assets, with the understanding that PSI and company directors responsibilities still apply.

Either way, the real wins come from clean job costing and record-keeping that make BAS and tax time less stressful, clear separation between business bank account and personal banking, and understanding how PSI, GST thresholds, company tax rate, and other business structures actually apply to your specific situation, using official ATO language and thresholds, not myths from the job site. This information requires professional verification.

Where ACT Tax Group Fits In

If you are reading this after another stressful BAS or an ATO letter that made your stomach drop, you are not alone, many ACT sparkies are in the same position. Choosing between a sole trader and a company structure is not a one‑size‑fits‑all decision and must be made with the 2025–26 ATO rules and your actual numbers in front of you.

ACT Tax Group works with electrical contractors who want clear, operational steps to keep BAS, GST, STP, and super running smoothly, whatever structure you use, from sole trader company to more complex business structures. They provide straight talk on how ATO rules like GST registration, PSI, and company tax rates affect you.

This article is general in nature, for illustration only and does not constitute financial or personal advice. For ATO-compliant support that looks at your actual turnover, risk profile, and growth plans, book a consult with ACT Tax Group before you make any structure changes or sign major contracts.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)