Understanding the Corporate Tax Rate: How It Affects Carpentry Companies in Australia

Published on December 22, 2025

Understanding the corporate tax rate is essential if you want your carpentry company to keep steady cash flow, stay ahead of the Australian Taxation Office, and avoid nasty surprises at tax time. When you know how the company tax rate is set, how taxable income is worked out, and why different tax rates apply to different companies, it becomes much easier to plan for your financial year instead of reacting at the last minute.

When Company Tax Collides with Carpentry Cash Flow

Imagine this: you have several builds on the go, big progress claims out to builders, and money tied up in retentions, but your bookkeeper tells you the company will still have to pay tax soon. You look at the bank account and think, “How much tax can there really be when cash is this tight?” This is where understanding your total assessable income, company tax deductions, and timing across the entire year becomes critical.

For a carpentry company, corporate income is not just about what is in the bank today. It includes trading income from jobs, any interest income in the company bank account, and even net capital gains from selling an asset. When business owners miss how these pieces add up to total assessable income, the final company tax returns can feel completely out of step with day‑to‑day reality on site.

Struggling to match project income with ATO tax obligations?

Schedule a complimentary consultation with us today to align your WIP, progress claims, and BAS reporting for accuracy.

What Is the Corporate Tax Rate for Carpentry Companies?

In Australia, there are currently two main company tax rates for most trading companies: a 25% lower company tax rate for companies that qualify as a base rate entity, and a 30% full company tax rate for companies that do not. There is a lower company tax rate for eligible companies that meet the base rate entity test, and a full company tax rate for others that do not. Your carpenter crew might be working flat out, but the way your income is classified, and your company’s aggregated turnover are what decide whether your company pays the lower tax rate or the higher one.

The base rate entity test is determined annually based on two main points: the aggregated turnover threshold (currently less than 50 million for the relevant income year) and whether 80% or less of the company’s assessable income is base rate entity passive income. Aggregated turnover is broadly your annual turnover from all connected entities and Australian operations grouped together, not just one company on its own. To access the lower 25% company tax rate, your company’s aggregated turnover for that income year must be less than 50 million, and no more than 80% of its assessable income for that year can be base rate entity passive income.

If your carpentry company is mainly earning trading income from decks, frames, fix‑outs, and similar work, and not from investment properties or other passive income sources, you are more likely to qualify as a base rate entity. On the other hand, many property investment companies or investment companies with high passive income from rental income, interest income, and certain trust distributions will often end up on the full company tax rate. The company tax your carpentry business pays is therefore linked to both size and the mix of income, not just the fact that you are a trades business.

How Taxable Income Is Worked Out for a Carpentry Company

Many business owners want a simple answer to ‘How much tax will my company pay this year?’ but the starting point is understanding taxable income, not just gross income or annual turnover. Taxable income is generally your total assessable income for the income year (including trading income, some investment income and net capital gains) minus allowable deductions. Assessable income normally includes trading income from jobs, interest income, rental income if the company holds investment properties, dividends and franking credits, and any net capital gains where gains arise from selling certain business or investment assets.

On the deduction side, you claim items like materials, subcontractors, wages, Super, insurance, and professional fees that are directly tied to earning that income. For carpentry companies, this also includes things like tools and equipment that may use instant asset write off where the rules apply in the specific financial year. The key is that every tax return is based on records that cover the entire year, not just what happened in the last quarter.

If your company has multiple entities or connected entities, income and deductions may also need to be considered across the group when working out aggregated turnover and other eligibility requirements. This is where many business owners miss important details that change their tax position. Working through your worldwide income, Australian operations, and any foreign shareholders or corporate distributions is something a registered tax agent can help with so your company pays the correct amount and can access any available lower company tax rate.

Why Passive Income and Investment Activity Matter

You might think, “We are a carpentry business, not an investment company, why should passive income matter?” The reason is that the base rate entity test looks at base rate entity passive income compared with total assessable income. If your carpentry company also owns investment properties, receives rental income, or holds shares that generate dividends and franking credits, that passive income can change which tax rate applies.

High passive income can push a company away from the lower tax rate and into the full company tax rate band, even if the trading side of the business is solid. Rental income, interest income, and some trust distributions are counted in the passive income test. For many property investment companies, rental income counts as a key driver of their tax rate, while for a carpentry business it might be a smaller part of total income but still important if it grows over time.

For Australian companies with foreign shareholders or overseas investments, new international tax measures such as the income inclusion rule and the undertaxed profits rule may also affect how some overseas profits and corporate distributions are taxed, particularly for larger or multinational groups. These rules are complex and targeted at ensuring companies pay their fair share of income tax rather than shifting profits to low‑tax locations. While most local carpentry companies will not deal with them directly, they are a reminder that the tax rate is always linked to the mix of income and where it is earned.

How Corporate Tax Shows Up in Everyday Carpentry Jobs

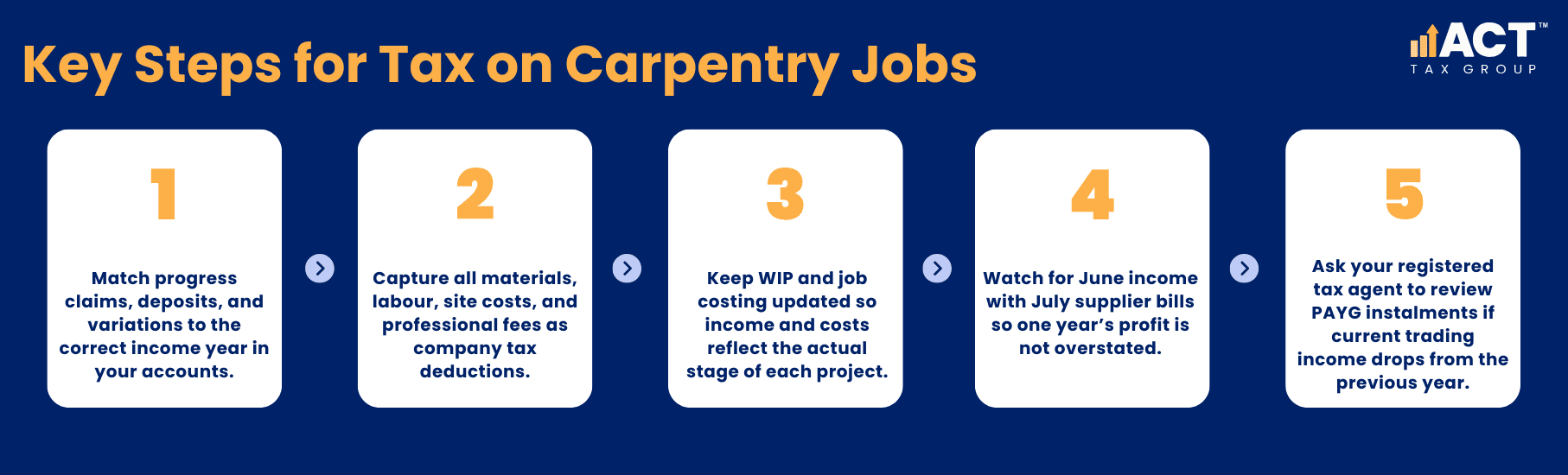

In practice, your company tax is driven by how trading income from jobs, company tax deductions, and timing all stack up in the financial year. When you issue progress claims, receive deposits, and finalise variations, that business income builds up your total assessable income for that income year. At the same time, your materials, labour, site costs, and professional fees build up your deductions.

If WIP and job costing are not kept up to date, you can end up with a mismatch between the income recorded in the accounts and the actual stage of the work. This affects taxable income and the company tax you pay. For example, if a large part of the gross income from a project lands in June but key supplier bills do not get processed until July, the previous income year may show higher profit than you expect. Over time this can distort your tax position, especially if it happens across several jobs.

Your most recent tax return affects how PAYG income tax instalments are set for the next year. If the company had strong profit in the last lodged return, the ATO will often base PAYG instalment amounts or rates on that taxable income, adjusted by a GDP factor for expected growth. If the following year is weaker or has slower trading income, you might need your registered tax agent to review these instalments, so the company pays a fair share of tax but not more than needed through the year.

Working with Company Tax Returns, Franking Credits, and Different Tax Rates

Once the financial year ends, the company tax return pulls everything together: total assessable income, allowable deductions, and the correct company tax rate (25% or 30%) based on whether the company qualifies as a base rate entity for that income year. This is also where franking credits and franking rates come into the picture for owners who take dividends. Franking credits work by passing on some of the company tax that the company pays to shareholders, so they are not taxed twice on the same income.

For carpentry owners who draw dividends as part of their overall income, it is important to understand how company tax, franking rates, and your own income tax fit together. Your personal tax depends on your specific circumstances, including your share of voting power, any trust distributions you receive, and your other income outside the company. Many business owners use a registered tax agent to keep track of these links so that the company and owners together pay tax at the correct amount.

Because there are different tax rates for different types of companies and different owners, it is important not to assume that what works for larger businesses or investment companies is suitable for your carpentry business. Your structure, your annual turnover, your GST turnover, and how your income is split between business income and passive income all matter in how your tax position is worked out.

Getting Practical Help So Company Tax Does Not Derail Your Next Project

As a carpentry business owner, you do not need to become a tax expert, but you do need clear, simple systems that make your income, expenses, and tax position visible throughout the year. This includes keeping trading income, instalment income, and any rental income or interest income clearly separated and well recorded so that the company pays tax using accurate figures rather than estimates.

This is general information, not financial or personal advice, and it does not cover all tax rules that may affect your business. Company tax outcomes always depend on your specific circumstances, including previous income year results, any multiple entities or connected entities in your group, and how your income is split between Australian companies and any overseas interests. For ATO‑compliant support tailored to your carpentry business, book a consult with ACT Tax Group so you can stay focused on running profitable jobs while your company tax is handled properly.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)