Choosing the Right Business Structure: Company vs Sole Trader for Australian Carpenters

Published on December 9, 2025

Choosing the right business structure: company vs sole trader for Australian carpenters can feel like a big decision when your cash is tied up in retentions, crews are on the books, and your family home is on the line if something goes wrong. You might be wondering whether staying as a sole trader business structure is still enough, or if it’s time to shift to a company structure that separates your personal and business assets.

Why Your Business Structure Matters More Than You Think

As a sole trader, there is no separate legal entity. You and the business are the same legal person. All business income is taxed under your personal income tax rates on your personal tax return, and you use your individual tax file number for tax reporting. That simplicity comes with unlimited personal liability. If there are business debts in the business—for example, unpaid suppliers, tax debts, or a big claim from a builder—you are personally responsible. Creditors can pursue your personal assets, not just your business assets.

With a company structure, you create a separate legal entity. A proprietary limited company is registered with ASIC (the Australian Securities and Investments Commission), with its own Australian Business Number and often its own business name. The company owns the business assets and business bank account, and it signs contracts in its own name. In most cases, this structure gives you asset protection: you’re less likely to lose your personal and business assets if the business cannot settle business debts, because the company is the one that owes the money.

Paying too much tax as your carpentry profits grow?

Schedule a complimentary consultation with us today to compare sole trader and company tax outcomes.

How a Sole Trader Structure Works Day to Day

When you’re operating as a sole trader, you’re using the simplest business structure available. You apply for an Australian Business Number and, if needed, register a business name. You use your own individual tax file number for taxes and often start with a personal bank account rather than a clearly separate business bank account. Each year, you lodge one personal tax return that includes your business income and expenses, which means your business finances flow directly into your own tax reporting.

Income and Tax for Sole Traders

Your business income is taxed at personal income tax rates, which increase as your income rises. As profit grows, you may find you pay more tax than a similar business in a company, because companies pay a flat company tax rate (often 25% for many small trading companies). There is no separate business tax return for the business itself—everything gets rolled into your own return. The tax liability falls on you personally, and you’re responsible for paying income tax, any tax debts, and managing your own tax reporting through the ATO.

Simplicity and Low Costs

The upside is low ongoing costs and less admin. There’s no annual review fee to ASIC, no company registration to maintain, and no company directors’ duties. You can often manage your business finances from a personal bank account without needing separate accounting systems, though it’s still wise to keep a clear business bank account so you can see what belongs to the business and what is personal.

The Unlimited Liability Problem

The downside is that you are personally liable for all business debts and legal liabilities. If you’re sued, or you can’t pay business debts or tax debts, there’s no line between your business money and your personal money unless you’ve been very disciplined about keeping a separate business bank account and clear business finances. This means your home, car, savings, and other personal assets are all at risk if the business faces a major claim or cannot settle its debts.

How a Company Structure Changes Things

A company structure is one of the most common business structures used once a carpentry business grows beyond just the owner and a mate. When you register a proprietary limited company, you register with ASIC and pay a company registration fee. You have one or more company directors who are responsible for running the company and will need to open a separate business bank account for company money. Going forward, you’ll keep more detailed financial records, including income, expenses, and assets held by the company. Each year you’ll lodge a separate company tax return in addition to your own personal tax return.

The Separate Legal Entity

The company is a separate legal entity and is treated differently for tax purposes. This separation is the key advantage: the company owns itself, signs its own contracts, and holds its own business assets. The company is the entity that owes money and faces legal claims, not you personally, which changes how much personal risk you carry day to day.

Tax Rate and Profit Distribution

Companies pay a company tax rate on profits (commonly 25% for base‑rate entities and 30% for other companies). You then decide how to distribute profits to yourself: wages, director’s fees, or dividends. This gives more flexibility for tax planning, as you can manage when and how you take income out of the business and how much to retain within the company to build reserves or reinvest in equipment and vehicles. It also means companies pay tax at a flat rate, which may be lower than the highest personal income tax rates.

Ongoing Compliance and Costs

There are, however, ongoing costs. You must pay an ASIC annual review fee (currently $329 for a proprietary company as of July 2025) to keep the company registered, and you usually face higher accounting costs due to a separate company tax return and more complex tax reporting. For many carpenters, this extra cost is justified by having company debts and legal claims contained in the company, not on you personally, and by having clearer separation of personal and business assets.

Cash Flow, Retentions, GST and Tax Reporting

Retentions and progress claims are where the real pain often shows up. Under a typical contract, a builder might retain 5–10% of each payment, holding it until practical completion or even longer. That means you could be funding the job, wages, and materials out of your own pocket while waiting months to be paid. On a $100,000 progress claim, retaining $5,000 to $10,000 means your cash flow gets stretched thin while you’re still paying your crew, suppliers, and subcontractors from your business account.

The GST Timing Problem

Once your business turnover reaches the threshold for Goods and Services Tax, you must register for GST and charge 10% services tax on your invoices. Whether you are a sole trader or a company, you then need to lodge Business Activity Statements and pay GST collected back to the ATO. If you’re accounting on an accrual basis, you can end up paying GST on invoices that haven’t been paid yet, including the retained amounts. This means you might owe the ATO $10,000 in GST while you’ve only received $55,000 of a $110,000 invoice, with the rest held as retention or not yet paid.

Managing Cash Flow Across Both Structures

This is where a clearly separate business bank and tight cash‑flow planning become essential. As a sole trader, if you mix your personal and business finances, it’s easy to lose track of how much needs to be set aside to pay GST, income tax and super. With a company structure, you’re more likely to keep company money in a business account, track those obligations properly, and avoid nasty financial or tax debts later. A separate business bank account makes it clearer what’s available and what needs to be reserved for tax and superannuation obligations.

Risk, Legal Liabilities and Asset Protection

The big question for most carpenters is “how much personal risk am I carrying?” On a busy site, things can go wrong: defects, injuries, property damage or contract disputes. If you operate as a sole trader, you are personally responsible for legal liabilities and business debts. Even with public liability insurance and other policies, there can be gaps and excesses that fall back on you. A major claim that exceeds your insurance could wipe out your savings and put your home at risk.

How Company Structure Protects You

With a company, company debts are generally separate from your personal finances. Creditors claim against company assets first. While banks and suppliers may still ask for personal guarantees in some cases, having the company in place still provides an extra layer of asset protection around your personal assets, especially your home. Company directors do have obligations under the law, but the starting point is that the company, as a legal entity, carries the risk and is the one that owes money when things go wrong.

The Real-World Difference

If you are serious about protecting your personal and business assets, and you want clearer lines between your business account and your home finances, a company structure is usually stronger than continuing as a sole trader arrangement where everything is in your personal name and flows through your personal tax return. This separation becomes especially important once you’re running crews, managing multiple contracts, and facing the kinds of liability risks that construction work naturally carries. The family home stops feeling vulnerable when business risk is carried by the company, not by you as an individual.

Tax Implications, Tax Benefits and Ongoing Costs

From a tax angle, both sole trader and company options have pros and cons. Understanding how each one affects your take-home money is crucial to the decision.

Tax Rates for Sole Traders

As a sole trader, you report all business income in your own return and pay tax at personal rates, which can climb as income grows. You may feel tax is high once profits increase, but your admin is simpler because there’s only one personal tax return to lodge and no separate company tax return. Your tax liability is calculated at marginal rates, meaning higher profits attract higher tax rates. If you earn $200,000 as a sole trader in carpentry, you could pay significantly more in personal income tax than a company earning the same profit.

Tax Rates and Flexibility for Companies

As a company, you lodge an annual company tax return that covers all company income and expenses. You pay tax at the company tax rate, which can be lower than top personal rates, and you still lodge your own personal return for wages or dividends you receive. You may access some tax benefits through timing of dividends, reinvestment in the business, and clearer tax planning. If you earn $200,000 profit as a company, you pay company tax rate (25%) on that profit, leaving $150,000 retained in the company. As a sole trader earning the same amount, you’d pay personal income tax rates, which can be much higher, leaving far less to reinvest.

The Cost-Benefit Analysis

You must also factor in extra costs: accounting fees for a separate company tax return, ASIC annual review fee, and higher bookkeeping expectations to maintain detailed financial records. These ongoing costs are part of the trade‑off for lower personal risk and more flexible ways to distribute profits. For most carpenters turning over $500,000 or more, the tax savings and asset protection usually justify these extra costs within a year or two.

Payroll, Workers and Super: Being Personally Responsible vs Company Employer

Once you start hiring, the way you structure your business affects how you handle tax and superannuation obligations, workers compensation insurance and payroll admin. The responsibility and liability shift depending on whether you’re a sole trader or a company.

Sole Trader Payroll Responsibility

As a sole trader, you are personally responsible for paying staff correctly, including super and any fringe benefits tax if you provide certain benefits. You’ll often manage wages from your business bank account and report payroll through Single Touch Payroll under your ABN. Mistakes with wages or super fall directly back on you, not a separate entity, and the Fair Work Ombudsman will pursue you personally if there are underpayments or compliance breaches. The personal liability means you’re on the hook for back pay, penalties, and fines if something goes wrong with staff entitlements.

Company Payroll Structure

As a company, the company is the employer and the entity that holds the legal responsibility for payroll compliance. Company directors must make sure staff are paid correctly, tax and super are withheld and reported, and that you meet any requirement to hold workers compensation insurance. The company’s payroll reporting feeds into both company tax and staff own tax return details, tying into the ATO systems. While directors still have duties and obligations, there’s at least a separation between personal liability and the business liability in the company’s name.

Growing Team Complexity

In both cases, you need to keep on top of pay rates, awards and super rules. But as the operation grows and you’re running multiple crews, most carpenters find a company structure fits better with the size and risk level of the team they’re running. The more people you employ, the more important it becomes to have clear payroll systems, proper tax reporting, and a business structure that protects you personally if there are payroll mistakes or disputes.

When Carpenters Usually Shift from Sole Trader to Company

Most carpenters don’t switch structure on day one. The pattern is usually starting as a sole trader structure with just yourself, then adding a labourer or apprentice and a couple of subbies, hitting the GST threshold and starting to lodge BAS, taking on bigger jobs with retentions and tighter contract terms, and eventually realising that the business has outgrown the original setup.

Warning Signs It’s Time to Move

Signs it may be time to move from a trader and a company comparison stage into actually forming a company include business income that’s grown to the point where you’re regularly in higher personal income tax brackets, worry about being personally liable for large legal claims or business debts, desire for a clearer way to separate personal and business finances, and thinking about future growth, bringing in partners, or how to raise capital. Many carpenters also move to a company structure when they want to buy vehicles or equipment and keep those business assets clearly separate from personal assets.

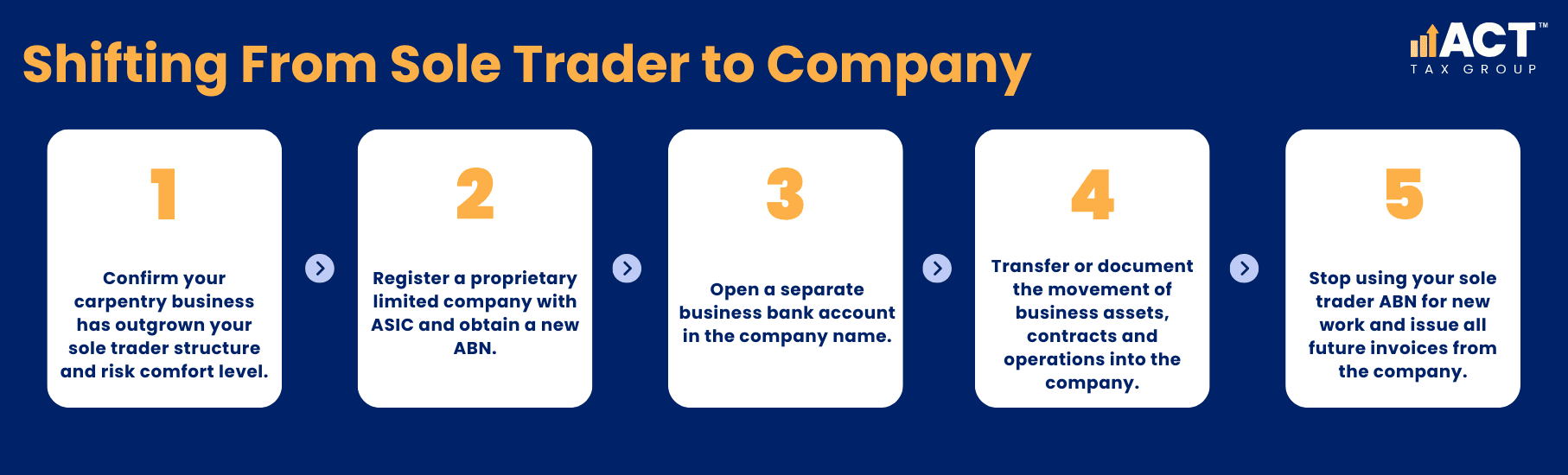

The Transition Process

When you change structure, you don’t lose everything you’ve built. You can transfer your existing carpentry work into the company, use the same business name (with the right registrations), and keep trading—just under a different legal entity, with a separate business tax return and clearer lines between business and personal money. The transition itself is straightforward: incorporate with ASIC, get a new ABN for the company, set up a company bank account, and formally transfer or document the shift of your business assets. Your old sole trader ABN stays registered but stops being used for new work; all future invoices come from the company.

Which Option Fits Your Carpentry Business?

Both sole trader and company options are part of the most common business structures used by small businesses in Australia. There aren’t “right” and “wrong” choices in isolation—only better fits for where your carpentry business is now and where you want it to go.

Sole Trader When Starting Out

If you’re just starting out, operating as a sole trader may give you the low‑cost, flexible start you need. There’s minimal paperwork, no registration fees, and you can focus on building your reputation and winning work without worrying about complex business structures.

Company Structure Advantage on Growing Business

As your turnover, risk, and responsibilities grow, a company business structure gives you separation between your personal and business assets, a separate legal entity that carries most company debts, a separate tax return and company tax rate that can help you manage tax as profits grow, and a clearer base for long‑term tax planning, profit distribution, and possibly selling the business down the track. The extra cost and complexity become worthwhile investments in your family’s financial security and your business’s future.

Conclusion

The choice between a sole trader structure and a company structure isn’t something you need to stress about forever. Most carpentry businesses naturally move to a company once the numbers and risks justify the extra complexity. Talk to an accountant who understands construction, who knows about retentions, progress claims, and the kind of payroll and compliance issues that carpenters actually face. They can run your specific numbers and help you decide whether now is the right time to shift, or whether staying as a sole trader still makes sense for your situation. The decision often comes down to three things: how much profit you’re retaining in the business, how much personal liability you’re comfortable carrying, and how much you want to protect your family home and personal assets from business risk.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)