Cash vs. Accrual Accounting: Which is Best for Your Carpentry Business?

Published on September 23, 2025

Cash vs. accrual accounting isn’t just about bookkeeping—it’s about choosing a financial reporting method that matches how your carpentry business actually operates. If you’re running multiple crews, dealing with long term contracts that tie up your cash for months, and struggling to track whether each job is actually profitable, the accounting method you choose can make or break your ability to manage business cash flow and stay compliant with ATO requirements.

Understanding How Each Accounting Method Affects Your Daily Operations

The choice between cash or accrual accounting impacts every aspect of your carpentry business, from when you pay taxes to how you track job profitability. These aren’t just different ways to keep books—they’re fundamentally different approaches to recording income and determining your true financial position for tax purposes.

Is your carpentry business at risk of ATO non-compliance?

Schedule a complimentary consultation with us today to ensure your accounting method meets tax rules.

What Cash Basis Accounting Means for Your Carpentry Business

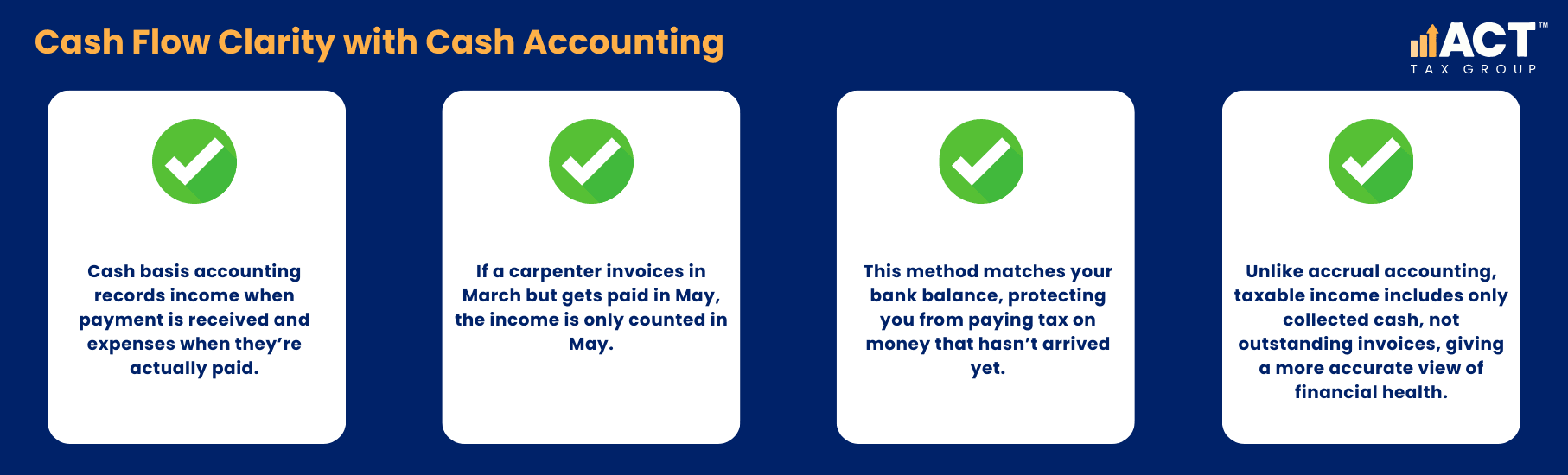

The cash method records income when money actually hits your bank accounts and expenses when you physically pay them. For carpenters, this means if you invoice a client for completed work in March but don’t received payment until May, that income doesn’t count toward March’s financials—it gets recorded in May when the actual cash arrives.

Cash basis accounting aligns perfectly with your actual cash position. When progress payments are delayed or retentions are held for months after completion, the cash basis method ensures you’re not paying tax on money you haven’t actually received. This gives a business owner much more accurate picture of their actual financial health from a cash perspective.

The primary difference becomes clear when dealing with delayed payments. Under cash basis accounting lies the reality that your taxable income only includes money you’ve actually collected, not money owed to you through outstanding invoices. This protects small businesses from the false sense of security that can come from counting unpaid invoices as current income.

How Accrual Basis Accounting Changes the Game

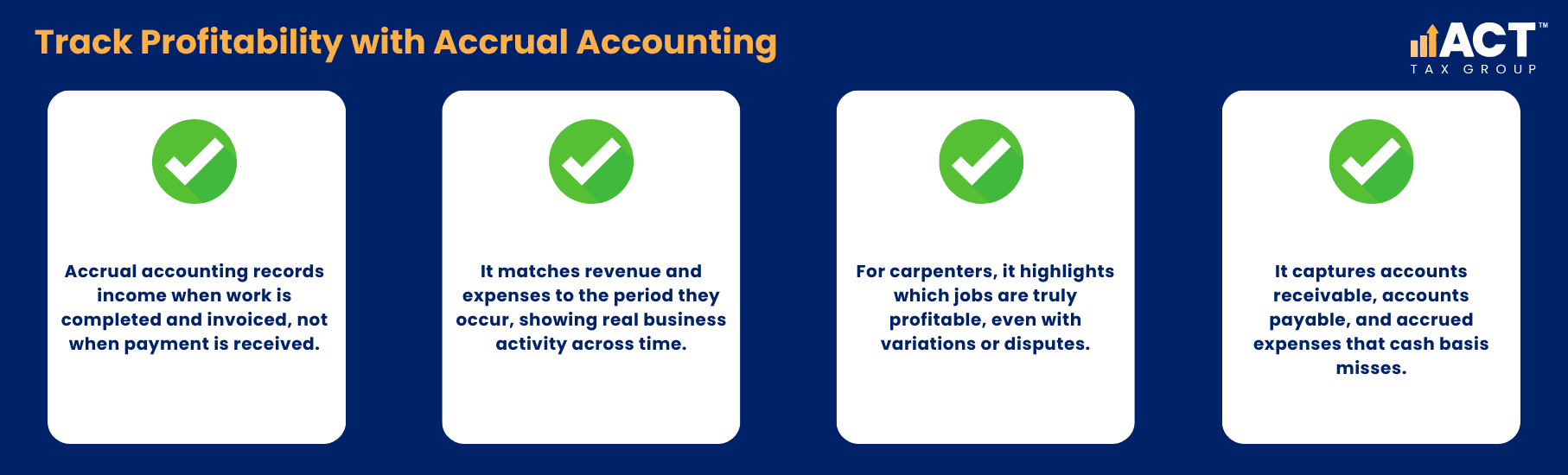

Accrual based accounting records revenue when work is completed and invoiced, regardless of payment timing. This accounting method tracks your true business activity rather than just cash transactions. Every progress claim gets recorded as income when you submit it, creating accounts receivable entries for amounts not yet collected.

Accrual accounting recognises revenue based on when you complete work, not when you receive cash. This means accrual accounting records revenue and expenses in the accounting period when they occur, giving you an in depth understanding of business performance across different time periods. The accrual method provides a much more accurate picture of your company’s finances by matching revenue and expenses to the periods when work actually happens.

For carpenters managing multiple jobs simultaneously, the accrual system shows which projects are actually profitable and when. This becomes crucial when dealing with variations, cost overruns, or disputes that could affect project profitability. The accrual basis method creates a clearer view of your business’s finances by including accounts payable and accrued expenses that cash basis accounting simply doesn’t capture.

The GST Reporting Reality Check

Your choice between cash and accrual extends to GST reporting through your Business Activity Statement. Under cash-based GST reporting, you only report GST when you actually receive payment from clients or pay suppliers. This approach aligns with actual cash flow rather than invoiced amounts, providing breathing room when clients delay payments.

However, businesses with aggregated turnover over $10 million must use accrual-based GST reporting. This threshold often catches growing carpentry businesses off guard, forcing them to report and pay GST on invoiced work even when payment is still outstanding. The key differences in GST timing can create significant cash flow pressure for businesses transitioning between methods.

Making the Right Choice Based on Your Business Size and Complexity

The decision between cash basis and accrual accounting depends heavily on your business’s current size, growth trajectory, and operational complexity. Understanding these factors helps ensure your accounting method supports rather than hinders your business goals.

When Cash Basis Method Makes Sense for Carpenters

The cash basis method works best for smaller carpentry operations with straightforward payment arrangements and minimal outstanding invoices. If most of your clients pay within 30 days and you don’t carry significant amounts of work in progress across multiple months, cash accounting’s simplicity can be a major advantage.

Very small businesses particularly benefit from cash basis accounting because it reduces administrative burden while providing natural cash flow protection. Small business owners can focus on the work rather than complex record keeping requirements when their operations remain straightforward. The cash method eliminates the complexity of tracking accounts receivable and accounts payable, making it ideal for carpenters who get paid straight away for completed work.

However, cash basis accounting has limitations that become problematic as your business grows. The method doesn’t track money owed to you or outstanding supplier invoices, making it difficult to assess your true financial position. When you’re dealing with retentions and extended payment terms, cash accounting can severely distort your apparent profitability from month to month.

Why Growing Carpentry Businesses Need Accrual Method

The accrual accounting method becomes essential once your operations reach a certain level of complexity. If you’re managing multiple crews across several job sites, dealing with significant retentions, or working on projects that span multiple months, accrual accounting provides the visibility you need to make informed decisions.

The accrual method allows you to track Work in Progress accurately, showing exactly how much profit each job has generated regardless of payment timing. This visibility becomes crucial when dealing with variations, cost overruns, or disputes that could affect project profitability. Banks and bonding companies typically require accrual-based financial statements, making this method necessary for securing larger contracts or business financing.

Accrual accounting also simplifies compliance as your business grows. The method integrates better with professional accounting software and provides the detailed financial transactions tracking required for larger operations. When your business grows beyond simple cash transactions, the accrual system provides the framework needed to maintain accurate financial records.

The $10 Million Threshold Reality

The $10 million aggregated turnover threshold serves as a critical decision point for carpentry businesses. Below this threshold, you can choose either cash or accrual accounting for income tax purposes. Once you exceed $10 million, several requirements change that affect how you record transactions and pay taxes.

You must use accrual-based GST reporting, meaning GST becomes payable when you issue invoices rather than when clients pay. This shift can create significant cash flow pressure if your clients typically pay slowly or if you’re dealing with substantial retentions. Your business also loses access to certain small business concessions, making tax planning more complex.

Many carpentry businesses find it beneficial to switch to accrual accounting before hitting the $10 million threshold to avoid sudden compliance changes mid-growth. The transition allows time to adapt systems and processes without the pressure of mandatory changes.

Practical Implementation and Compliance Considerations

Successfully implementing your chosen accounting method requires understanding both the technical requirements and practical implications for day-to-day operations. The transition process and ongoing compliance demands vary significantly between cash basis and accrual basis methods.

Setting Up Cash Accounting Systems

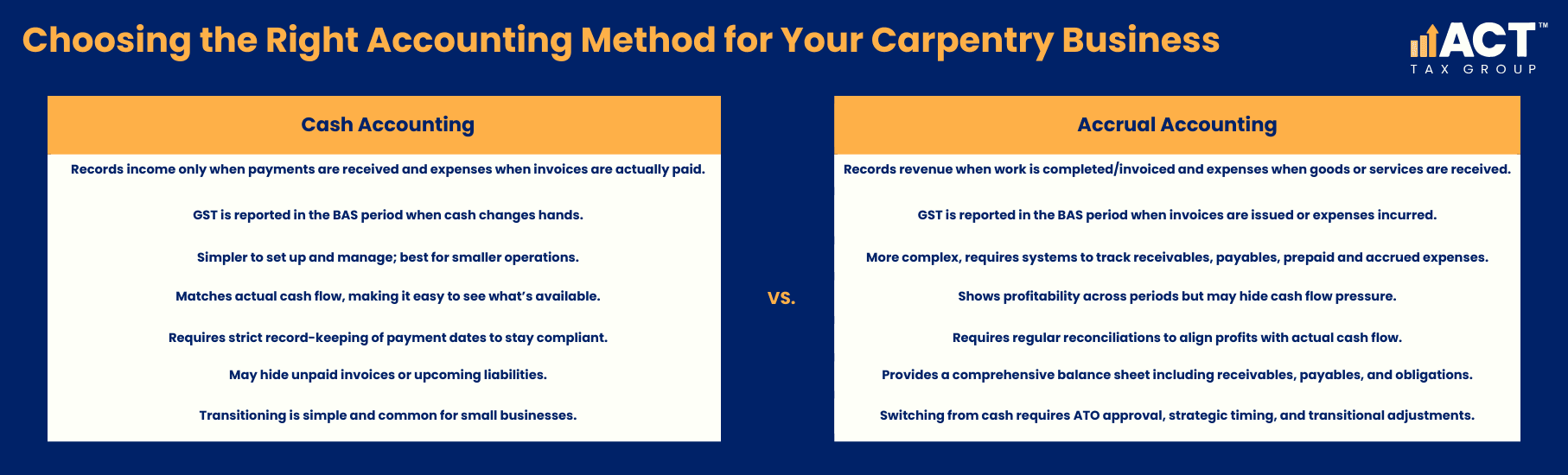

Cash accounting implementation focuses on tracking actual payments rather than invoice dates or work completion. Your system needs to record income when payments are received and record expenses when invoices are actually paid. This means maintaining clear records of bank accounts activity, with income and expense recognition tied directly to your bank statement dates.

For GST purposes under cash accounting, you report GST in the BAS period when cash actually changes hands. If you invoice a client in June but receive payment in August, the GST gets reported in your August BAS rather than June. This timing difference can provide cash flow benefits but requires careful tracking to ensure compliance.

The simplicity of cash accounting makes it accessible for smaller operations, but you must maintain discipline around record keeping. Every transaction needs proper documentation showing the actual payment date, as this determines the correct reporting period for tax purposes.

Implementing Accrual Accounting Effectively

The accrual accounting method requires more sophisticated systems to track both actual cash movements and outstanding receivables or payables. Your setup must record revenue when work is completed and invoiced, creating accounts receivable entries for amounts not yet collected. Similarly, expenses get recorded when goods or services are received, creating accounts payable for unpaid invoices.

This method demands regular reconciliation between your accounting records and actual cash position. You might show strong profits in your accounts while experiencing cash flow pressure due to slow-paying clients or significant retentions. Effective accrual accounting systems provide separate reports for profitability and cash flow to help manage this disconnect.

The accrual basis requires tracking prepaid expenses and accrued expenses that don’t exist in cash accounting. Prepaid expenses like insurance paid in advance get spread across the periods they cover, while accrued expenses like unpaid subcontractor invoices get recorded when services are received rather than when paid.

Managing the Transition Between Methods

Switching from cash to accrual accounting requires ATO approval and careful management of transitional adjustments. The change cannot be made mid-year, and timing the switch strategically can minimise tax implications. Many carpentry businesses find professional guidance essential during this transition to avoid compliance issues or unexpected tax liabilities.

The switch often reveals previously hidden aspects of business performance. Outstanding invoices that weren’t reflected in cash accounting suddenly appear as current income, while unpaid supplier bills get recognised as current expenses. This adjustment can significantly impact your reported profit for the transition year, affecting tax planning and business decisions.

Your balance sheet becomes much more comprehensive under accrual accounting, showing the true financial position including money owed to you and money you owe to others. This complete picture helps with business planning but requires more sophisticated record keeping than cash basis methods.

Making Your Decision and Moving Forward

Choosing between cash and accrual accounting shapes how you manage your business’ finances and should match your daily operations, plans for growth, and need for clear financial information. Cash basis works best for carpenters with fast payments and simple jobs, as it tracks money actually received and reduces the recordkeeping load. Accrual method is better for businesses with complex projects or significant retentions, giving you a clearer picture of true job profitability and helping you meet accepted accounting standards.

Your chosen method affects both income tax and GST, and the ATO expects you to stick with it for the whole financial year. Many carpentry businesses start on the cash basis for simplicity, then move to accrual accounting as their operations become more complex and a deeper level of financial detail is needed.

Accrual accounting uses the matching principle, so revenue and costs from each job appear in the same period, making it easier to see real profitability across projects and over time. Not all businesses need accrual accounting from the start, but understanding the strengths of both methods helps you make smart choices now and in the future.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)