How Carpenters Can Calculate the Medicare Levy on Their Income

Published on October 28, 2025

How carpenters can calculate the Medicare Levy on their income is a real concern for many working in Australia, especially when it comes time to estimate how much tax you’ll pay. Whether you’re running a small business, working solo, or employing others, calculating your Medicare Levy and any possible Medicare Levy Surcharge (MLS) is an important step in understanding your annual income and making sure there aren’t any surprises on your tax return.

What Is the Medicare Levy and Why It Matters

Almost every taxpayer in Australia is required to pay the Medicare Levy, unless they’re exempt or qualify for a reduction. The money contributes to the national Medicare system; the hospital cover all Australians benefit from. For the 2024-25 financial year, if your taxable income is above a certain amount, you’ll generally pay the standard rate – currently 2% of your taxable income.

Carpenters often wonder how much tax is actually withheld, especially when income fluctuates due to jobs finishing late or progress payments arriving outside of expected periods. The Medicare Levy is calculated as a percentage, separately from income tax, but included on your tax notice when you lodge your return.

Unsure if you’re paying the correct Medicare Levy?

Schedule a complimentary consultation with us today to accurately calculate your levy and avoid ATO errors.

Understand Your Taxable Income and Periods That Count

Your taxable income is the total amount you’ve earned – after claiming all allowable deductions for tools, vehicle, or business expenses. It’s important to estimate your income carefully, as the Australian Taxation Office (ATO) uses your annual income for calculations.

If you’re a sole trader, business owner, or have a spouse, dependants, or even a child after the first, keep in mind that family income threshold rules apply. The ATO website provides a calculator to help estimate your levy and whether your family or personal situation changes the amount you’ll pay.

Medicare Levy Thresholds and Reductions for Families

The ATO sets an income threshold each year for when you need to pay the Medicare Levy and when you might be eligible for an exemption or reduction. For the 2024-25 financial year, the basic thresholds are:

Singles don’t pay the levy if their annual income is below $27,222.

Families, including your spouse and dependent children, have a higher family income threshold. For MLS purposes, each child after the first raises the threshold by a set amount.

If income sits within a reduced range, you may be eligible for a smaller levy charge. These calculations are automatic when you lodge your return – the ATO runs the numbers and confirms your eligibility for any reduction or exemption.

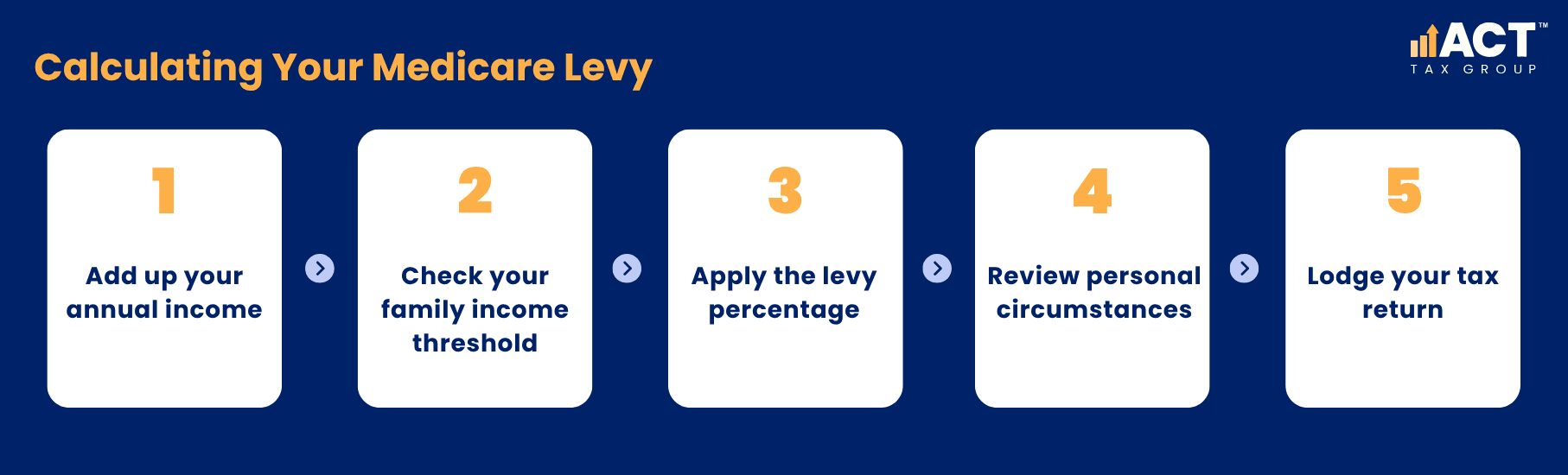

Step-By-Step: Calculating Your Levy

Here’s the practical workflow ACT carpenters can use to work out potential liability for the Medicare Levy and the Medicare Levy Surcharge (MLS):

Add up your annual income – Check your taxable income after expenses, using your preferred bookkeeping system or the online calculator from the ATO website.

Check your family income threshold – If you have a spouse or dependants, combine incomes and factor in any children for MLS purposes. This only affects the thresholds for families, not singles.

Apply the levy percentage – For those earning above the basic threshold, the standard rate is 2%. If you’re not eligible for a reduction or exemption, multiply your taxable income by 0.02 to estimate your levy.

Review personal circumstances – Having private hospital insurance or cover at the appropriate level might lower your MLS or even exempt you from it. If you don’t have suitable private health insurance, and your income is higher than the MLS threshold, you could pay an extra surcharge.

Lodge your tax return – The ATO will confirm your final liability, including the Medicare Levy and any MLS, and separate it from your regular income tax.

What If You Don’t Have Private Hospital Insurance?

Many carpenters ask whether they need an appropriate level of private hospital cover. The answer is specific to your circumstances. If your family income – including any spouse and all eligible dependants – goes above MLS thresholds, and you don’t have private hospital insurance, you’ll pay the Medicare Levy Surcharge in addition to your regular levy.

Private health insurance rebate may also apply to eligible payments, reducing your insurance costs.

Not having cover when required means you pay the MLS, so it’s important to check eligibility each period.

Exemptions and Special Situations for ACT Carpenters

Some taxpayers become exempt if they have special medical conditions, are non-residents for part of the year, or meet other criteria specified by the Australian Taxation Office. If you think you might be exempt, consult the ATO website or your accountant to review your eligibility.

If you have a child after the first, make sure you add the set amount to your family income threshold for accurate calculations. For those with variable income or periods working overseas, adjustments may apply to the overall benefit and levy.

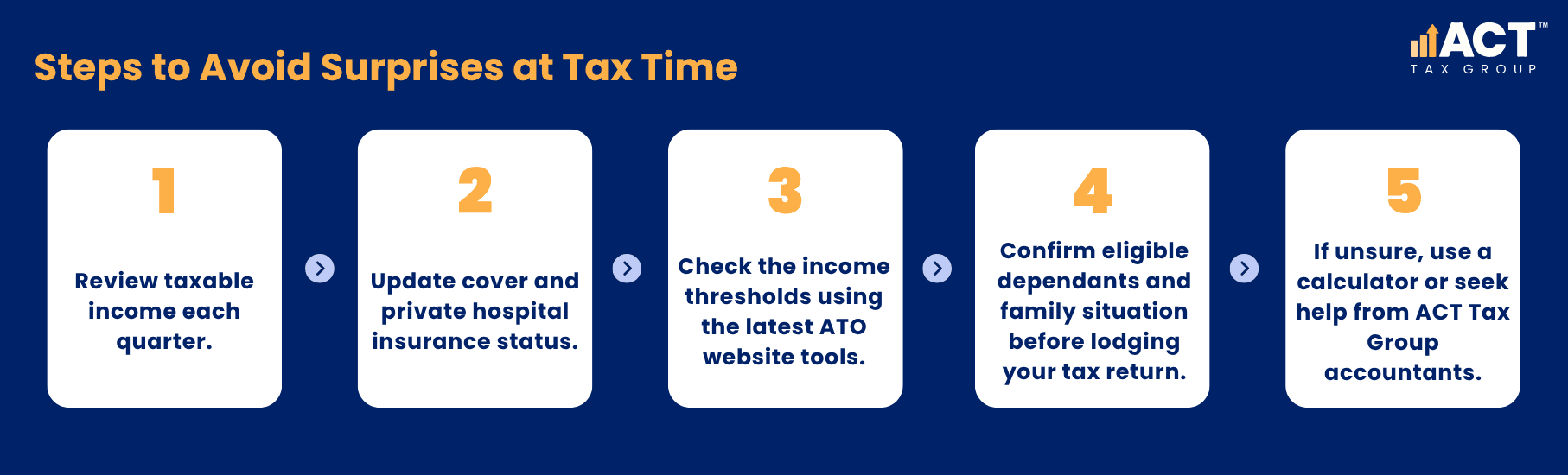

What to Do if Your Medicare Levy Estimate Seems Wrong

If your expectations for how much tax or Medicare Levy you pay don’t align with the ATO’s calculations, double check your income, eligible dependants, and periods worked. Sometimes the issue is missing information, or private health insurance not registered for MLS purposes. Lodge any corrections immediately and contact your accountant for support.

Conclusion

Calculating your Medicare Levy or any surcharge doesn’t have to be a headache. Understanding how your annual income, personal circumstances, family, and private health insurance all come together simplifies tax time and reduces uncertainty. Whether it’s checking eligibility, using a calculator, or reviewing the family income threshold, accurate records and timely review are the key.

ACT Tax Group is here to help you get your income, hospital cover, deductions, and levy right—so you stay in control, pay the correct amount, and spend less time worrying about calculations. If you’re uncertain about any benefit, liability, or exemption, our accountants keep the process straightforward.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)