What Counts as Assessable Income for Australian Carpenters?

Published on October 8, 2025

What counts as assessable income for Australian carpenters? This question keeps many carpenters up at night, especially when they’re juggling multiple jobs, dealing with retentions, and trying to stay on top of their tax obligations. Cash is tied up in progress claims, you’re never quite sure which payments need to declare in this income year, and the paperwork keeps piling up. However, the Australian Tax Office (ATO) expects a complete and accurate report of every dollar earned.

Understanding Assessable Income for Carpenters

When the tax office talks about assessable income, they’re referring to all income you need to declare on your tax return that’s subject to taxation. For carpenters, this includes your ordinary income—the money you earn regularly from your skills and efforts—plus any amounts specifically defined under tax law as income. The basic formula is straightforward: Assessable income minus allowable deductions equals taxable income.

As a carpenter working in ACT or anywhere across Australia, you’re dealing with income that falls into different categories. Your ordinary income typically includes salary, payments, and regular business earnings from carpentry work. Non assessable income covers specific amounts that don’t need to be included in your tax return, while exempt income refers to amounts that are assessable but not subject to tax.

Understanding these categories matters when you calculate your final tax bill. Assessable income forms the starting point, then you subtract allowable deductions to determine your taxable income. Your taxable income is what determines how much tax you actually pay, which makes understanding assessable income crucial for accurate tax planning and avoiding paying more than necessary.

Unsure which payments to include as income this year?

Schedule a complimentary consultation with us today to clarify what counts as assessable income for carpenters.

The Real-World Impact on Your Business

For carpenters running their own operations, assessable income determination affects when you pay GST and income tax. If your annual turnover reaches $75,000, you must register for GST within 21 days and start including GST in your assessable income calculations. This threshold isn’t based on financial years alone—it’s calculated on any consecutive 12-month period.

The timing of income recognition also matters significantly. Whether you use cash or accruals accounting determines when progress payments become assessable income. Under cash basis accounting, you include payments when received in your bank accounts, while accruals basis requires including income when work is completed, regardless of payment timing.

This timing difference can create cash flow challenges. You might pay tax on money you haven’t actually received yet, or you might receive money this year that relates to work done last year. Proper planning helps manage these timing differences and maintain healthy cash flow.

Main Types of Assessable Income for Carpenters

Understanding what qualifies as assessable income helps you track earnings accurately and avoid missing reportable amounts. The tax office uses sophisticated data matching systems, and contractors who omit income face penalties and potential audits.

Employee Wages and Contractor Payments

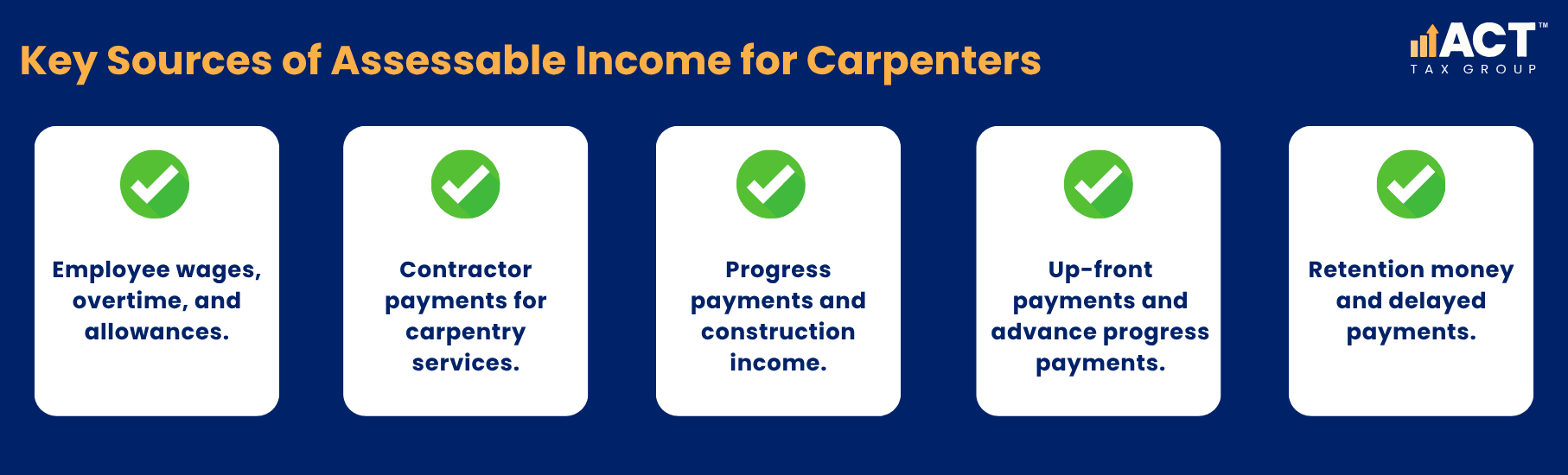

If you’re employed as a carpenter, your salary, overtime, and allowances are all assessable income. This includes any bonuses, commission, or performance payments your employer provides. Even non-cash benefits like tools, clothing allowances, or vehicle usage can be considered assessable income at their market value.

When you’re an employee, your employer withholds tax from your pay and provides a payment summary at year end. These amounts automatically appear in your tax return, making it easier to ensure everything is included correctly.

For contractors providing carpentry services, all payments received for your work are assessable income. This is particularly important because businesses hiring carpenters for building and construction services must report these payments to the tax office through annual reporting systems. If you’re a contractor, these amounts will be pre-filled in your tax return, making omission difficult and penalties likely.

Progress Payments and Construction Income

Long-term construction contracts create specific assessable income obligations that many carpenters find confusing. All progress payments and final payments received during the financial year must be included in assessable income, whether you’ve actually received the money or you’re entitled to receive it under the contract. Tax office rulings clarify that you cannot defer income by delaying billing when you’re entitled to invoice under the contract terms.

Up-front payments and advance progress payments are also assessable income that must be recognised when received. These amounts should generally be included in assessable income between receipt and when the next progress payment is due. This creates cash flow challenges if you receive large advance payments early in a project, as you’ll pay tax on money before completing the actual work.

For example, if you receive a $20,000 advance payment in June for work starting in August, that $20,000 becomes assessable income in the current financial year. You’ll pay tax on it this year, even though the actual carpentry work happens next year. Understanding this timing helps you plan cash flow and set aside money for tax obligations on advance payments.

Retention Money and Delayed Payments

Retention payments create particular challenges for carpenters because they affect both assessable income timing and cash flow. Amounts retained under retention clauses should not be included in assessable income until you either receive them or become entitled to receive them from the customer.

This timing difference is crucial for tax planning. If you’re using accruals accounting, retention amounts may not become assessable until the defects liability period expires and payment becomes due. For GST purposes, you don’t pay GST on retention amounts until you issue the retention invoice or receive payment, depending on your GST accounting method.

Understanding retention timing helps you plan cash flow and tax obligations more effectively. You won’t pay income tax on retentions until they’re actually due, which can be months or even years after completing the work.

How Different Employment Arrangements Affect Assessable Income

Your employment structure significantly impacts how income is assessed and taxed. Whether you’re an employee, independent contractor, or running a carpentry business determines your obligations and available deductions.

Employee vs Contractor Status

The distinction between employee and contractor isn’t just about having an ABN—it affects your entire tax position. Employees receive salary with tax withheld, while contractors manage their own tax obligations and can claim broader deductions.

Key factors the tax office considers include control over work methods, financial risk, ability to subcontract work to others, and provision of tools and equipment. If you’re genuinely contracting, you bear commercial risks and are responsible for fixing defects in your work. Employees work under direction and control with no financial risk.

Getting this classification wrong can be expensive. Employees misclassified as contractors might miss out on superannuation, workers compensation, and other benefits. Contractors treated as employees might face restrictions on deductions and different tax obligations.

Personal Services Income Rules

Many carpenters working as contractors fall under Personal Services Income rules. These rules apply when more than 50% of your payment is for your personal skills, knowledge, or efforts rather than for goods or equipment.

If these rules apply and you don’t qualify as a Personal Services Business, your income is taxed as personal income at individual tax rates. To qualify as a Personal Services Business, you need to pass either the results test or meet other specific criteria.

For carpenters, the key distinction is whether you’re mainly selling your labour and skills versus selling goods or using significant income-producing assets. A carpenter who builds and sells furniture primarily earns income from goods sales, not personal services income. However, a carpenter contracted mainly for labour earns personal services income.

Business Structure Considerations

Carpenters operating through companies, partnerships, or trusts face additional complexity around Personal Services Income rules. The starting point is that personal services income should be taxed to the individual providing the services, regardless of the business structure used.

However, proper structuring and meeting Personal Services Business tests can provide more favourable tax treatment. This might include access to a wider range of deductions, different timing of tax payments, and potential for income splitting in some circumstances.

Investment Income and Other Assessable Amounts

Carpenters often have income sources beyond their carpentry work that also count as assessable income. Understanding these helps ensure complete and accurate tax returns.

Investment Property and Rental Income

Many carpenters invest in property as a long-term wealth building strategy. Rent received from investment property is assessable income that must be included in your tax return. This includes any money received from tenants, whether it’s regular rent payments, bond money that you keep, or payments for property damage.

The gross amount of rent is assessable income, but you can claim allowable deductions for property expenses like interest on investment property loans, property management fees, repairs and maintenance, and depreciation on assets within the property.

If you’re renovating properties as part of your carpentry business, you need to assess whether this is business income from your carpentry services or investment income from property development. The distinction affects both income tax treatment and GST obligations.

Bank Interest and Investment Returns

Interest earned on bank accounts, term deposits, and other savings is assessable income. This includes interest from business bank accounts as well as personal savings accounts. Banks report interest payments to the tax office, so these amounts appear automatically in your tax return.

Dividends from shares and distributions from managed investments are also generally assessable income. However, dividends often come with franking credits that reduce your overall tax liability.

If you’ve invested in shares or managed funds as part of your wealth building strategy, you’ll receive annual statements showing the assessable income amounts. Keep these statements with your tax records to ensure accurate reporting.

Government Payments and Assistance

Various government payments can be assessable income depending on their purpose and your circumstances. Payments designed to replace lost income are generally assessable, while payments for specific costs or hardship might be exempt income.

For example, if you received JobKeeper payments during business disruptions, these were assessable income that needed to be included in your tax return. Similarly, business grants received to help with costs or expansion are usually assessable income.

However, genuine reimbursements for specific expenses you’ve incurred are typically not assessable income. The key is understanding whether the payment is compensating you for lost income or reimbursing you for costs you’ve paid.

GST Implications for Carpenter Income

GST registration significantly affects how you handle assessable income. Once your annual turnover reaches $75,000 in any 12-month period, GST registration becomes mandatory within 21 days.

GST Turnover Calculations

Your GST turnover includes all business income before expenses, including GST-free sales and government grants. It’s calculated on a rolling 12-month basis, not just financial years. This means monitoring income monthly becomes essential as you approach the threshold.

For carpenters, GST registration means charging 10% GST on most services and lodging Business Activity Statements quarterly. The GST you charge customers becomes part of your assessable income calculations, though you can also claim credits for GST paid on business expenses.

Understanding GST timing helps with cash flow planning. You’ll collect GST from customers throughout the quarter, then pay the net amount to the tax office when your Business Activity Statement is due.

Voluntary GST Registration Benefits

Registering for GST below the $75,000 threshold can provide cash flow benefits. If you purchase tools, materials, or equipment that includes GST, voluntary registration allows claiming input tax credits on these business purchases. This can save thousands annually on equipment purchases.

However, voluntary registration requires charging GST on all services and maintaining detailed records. You must also lodge regular Business Activity Statements, adding administrative burden.

The decision to register voluntarily depends on your specific circumstances. If you’re purchasing significant amounts of tools and equipment, the GST credits might outweigh the administrative costs. If you’re mainly providing labour with minimal equipment purchases, voluntary registration might not provide net benefits.

Record Keeping and Compliance Requirements

Accurate record keeping becomes critical for managing assessable income obligations. The tax office uses sophisticated data matching capabilities to identify unreported income, making complete records essential.

Essential Documentation

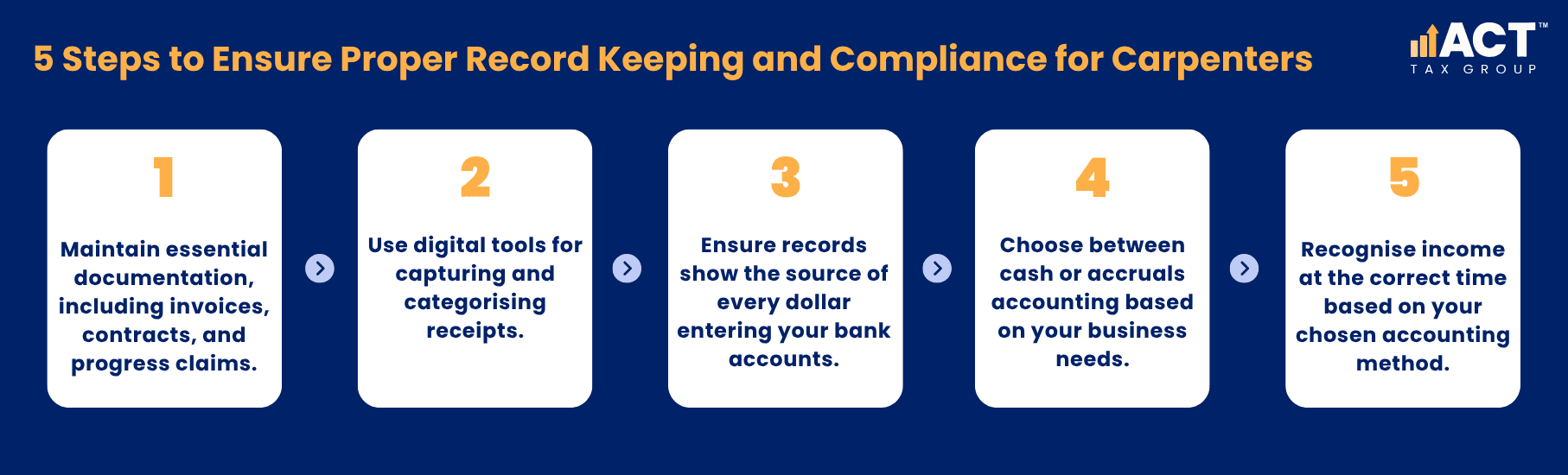

Maintaining proper records helps ensure all assessable income is captured correctly. This includes invoices issued and received, bank statements, contracts, progress claim documentation, and retention release notices. For contractors, keeping detailed records of all payments received prevents issues when the tax office matches reported payments with your tax return.

Digital receipt capture and cloud-based accounting systems can simplify record keeping while ensuring nothing falls through the cracks. Many carpenters find apps that photograph and categorise receipts particularly useful for maintaining complete records.

Your records should show the source of every dollar that went into your bank accounts. This helps distinguish between assessable income, loans, transfers between your own accounts, and other non-assessable receipts.

Timing of Income Recognition

Understanding when income must be included in your tax return prevents costly errors. Cash basis accounting includes income when received, while accruals basis includes income when earned. The choice affects tax timing but not total tax over the long term.

For carpenters working on projects spanning multiple years, accruals accounting often provides better matching of income and expenses. However, cash accounting can be simpler for smaller operations with straightforward transactions.

The timing choice becomes particularly important for large projects. Under cash accounting, you might have very little assessable income while work is in progress, then large amounts when progress payments are received. Under accruals accounting, income is spread more evenly as work progresses.

Common Mistakes and How to Avoid Them

Many carpenters encounter problems with assessable income reporting that are easily preventable with proper systems and understanding.

Omitting Contractor Payments

The tax office specifically targets contractors who omit income, using data matching to identify discrepancies. All payments reported by businesses through annual reporting systems must be included in your tax return. Using the tax office’s pre-filling service helps ensure these amounts are captured correctly.

If you discover you’ve missed income from previous years, it’s better to voluntarily disclose the error rather than wait for the tax office to identify it. Voluntary disclosures typically result in reduced penalties compared to tax office audits.

Incorrect Retention Timing

Including retention amounts in assessable income before they’re due creates unnecessary early tax payments. Only include retention when you’re entitled to receive it, not when the work is completed. This timing difference can significantly impact cash flow and tax obligations.

Understanding your contracts helps determine when retentions become assessable. Some contracts release retentions automatically after defect liability periods expire, while others require you to claim the retention before it becomes due.

Mixing Personal and Business Transactions

Carpenters operating through business structures must correctly separate personal and business income. Personal services income should generally be taxed to the individual providing the services, not retained in business entities unless specific tests are met.

Similarly, personal expenses can’t be claimed as business deductions, and business income can’t be treated as personal gifts or loans. Maintaining separate bank accounts and clear records helps avoid these issues.

Forgetting Investment Income

Many carpenters focus on their carpentry income but forget to include investment income like bank interest, dividends, or rental income. While these amounts might seem small individually, they add up over time and the tax office receives copies of all these payments.

Using tax return software or professional assistance helps ensure all income sources are included. The tax office’s pre-filling service automatically includes most investment income, making omission less likely but not impossible.

Working with Professional Support

Tax professionals familiar with construction industry issues can help understand reporting requirements for your gross income, including carpenter payments, bank accounts dividends, and any employment termination payment you might receive. They understand how nonexempt income from various sources affects your overall tax position and can ensure nothing gets missed when calculating your total assessable amounts.

Professional assistance becomes particularly important when you have financial assets generating other income alongside your carpentry work. Whether you earn deemed income from investments, receive education payments for training, or have income that puts you above the tax-free threshold, experienced professionals can help structure your affairs properly.

Professional advisers can identify when your income mix changes, help you understand what qualifies as only income versus assessable amounts, and ensure proper treatment of all income types.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)