ATO Guidelines for Substantiating Home Office Expense Claims

Published on February 3, 2026

ATO Guidelines for Substantiating Home Office Expense Claims matter if you want to maximise home office tax deductions without unnecessary stress at tax time. When you understand how the Australian Tax Office expects you to approach claiming home office expenses, the whole process becomes much more manageable. You can then confidently claim expenses you incur while keeping your record keeping simple and consistent.

What Do ATO Guidelines for Home Office Claims Actually Require?

The ATO expects that any home office expenses you claim are clearly linked to earning your income, either as an employee or as a business owner. You must have actually incurred the work-related expenses yourself, and you need to show the work-related portion where there is personal use. In short, you want your total deductible expenses to be reasonable, well supported, and easy to explain.

The rules also distinguish between home office running expenses and occupancy expenses. Running expenses include day‑to‑day costs such as energy expenses and internet expenses, while occupancy expenses include rent or mortgage interest, property taxes, land taxes, and house insurance premiums. You can only claim occupancy expenses in limited circumstances where part of your home is genuinely used as a place of business, not just a convenient spot to check emails.

Unsure whether to use the fixed rate or actual cost method?

Schedule a complimentary consultation with us today to determine which method gives you the best return.

How Do the ATO’s Home Office Claim Methods Work?

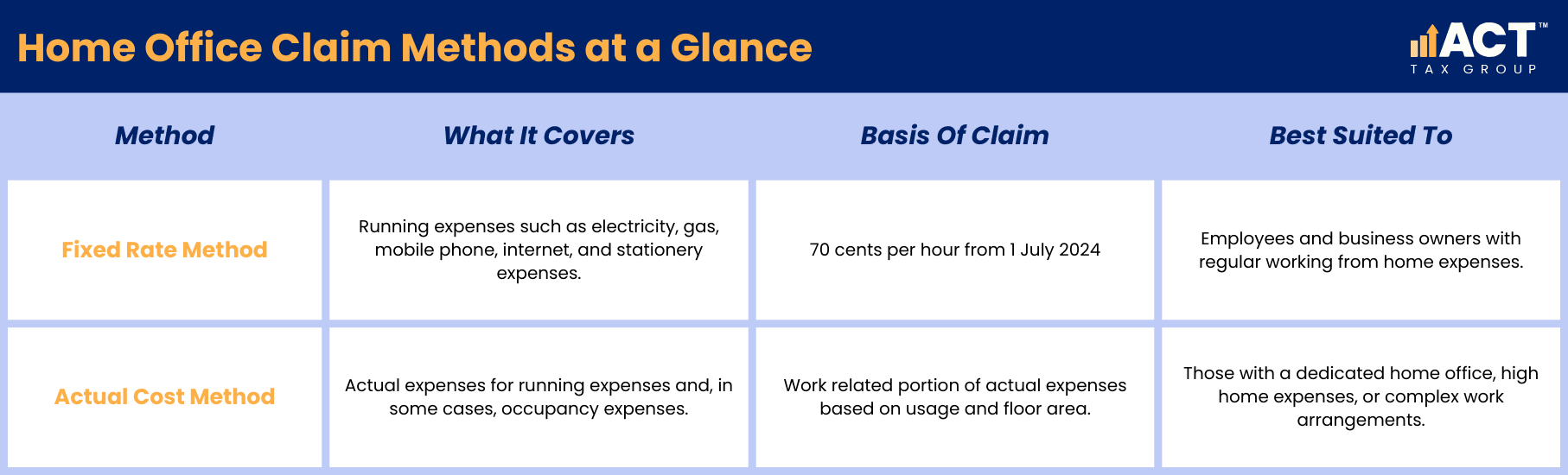

You generally choose between the fixed rate method and the actual cost method when claiming home office deductions. The fixed rate method uses a cents per hour approach for working from home expenses, while the actual cost method uses actual expenses and more detailed calculations. Both can be effective if they suit your personal circumstances and you follow the rules.

Under the revised fixed rate method, you claim 70 cents per hour for each actual hour you work from home from 1 July 2024 onwards. This rate is designed to cover several home office running expenses such as energy expenses, mobile phone expenses, internet expenses, and stationery and computer consumables. The actual cost method, on the other hand, can be better where home expenses are high or where you have a dedicated home office that you use mainly for work.

How Does the Fixed Rate Method Affect Substantiation?

The revised fixed rate method is designed to simplify claiming home office expenses by bundling many running expenses into one rate of 70 cents per hour from 1 July 2024. This means home office running expenses like electricity, gas, mobile phone, mobile internet, data expenses, internet bills, and stationery expenses are all treated as covered by the cents per hour rate. Because these costs are grouped together, you do not make separate claims for these same expenses.

You still may be able to claim an additional separate deduction for certain home office equipment and office furniture. Examples include a desk, office chair, computer, printer, or office plant where the decline in value is claimed over time. In some cases, smaller items may qualify for an immediate deduction, depending on their cost and how you use them.

What Evidence is Needed for the Actual Cost Method?

The actual cost method requires more detailed record keeping but can produce better home tax deductions where expenses are higher. Under this approach you work out the work-related portion of each relevant cost, including energy expenses, internet expenses, data expenses, stationery and computer consumables, and cleaning of your dedicated home office. You can also look at occupancy expenses such as rent or mortgage interest and property taxes if your home genuinely operates as a place of business.

This method often relies on a mix of bank statements, bills, diaries, and floor plans. For example, you might calculate the percentage of your home’s floor area used by your home office, then consider how many hours that room is used for work compared with personal use. You then apportion costs like mortgage interest, house insurance premiums, and land taxes based on that percentage.

How Should You Track Hours and Usage for The ATO?

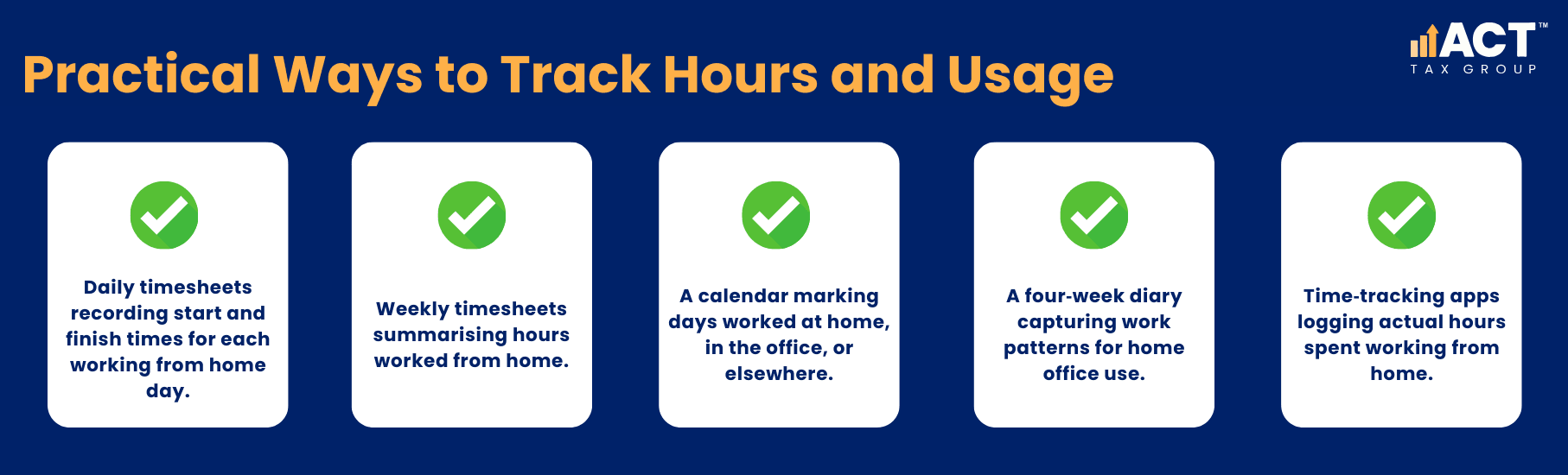

Strong record keeping is central to substantiating home office tax deductions, regardless of the method you choose. For the revised fixed rate method, you need records of actual hours you spend working from home throughout the year, not just a four‑week sample. That means you need a simple system rather than relying on memory at tax time.

You might track work hour details using a calendar, spreadsheet, timesheet, or time‑tracking app. Many business owner clients use job management software, while employees may rely on employer timesheets or online log‑in reports. The key is that your records clearly show when you were working from your home office so your cents per hour claim is well supported.

What Counts as a Work‑Related Home Office Expense?

Work-related home office expenses generally fall into three broad categories: running expenses, occupancy expenses, and office expenses. Running expenses include energy expenses, internet expenses, data expenses mobile, mobile phone expenses, and cleaning costs related to your home office. Office expenses include stationery expenses, computer consumables, and small home office equipment used mainly for work.

Occupancy expenses cover rent or mortgage interest, property taxes, land taxes, and house insurance premiums. You can only claim occupancy expenses and claim occupancy expenses where part of your home is clearly set up as a place of business and not just used casually. In many cases, you claim running expenses and office expenses but do not claim occupancy expenses because your home is still mainly private.

How Long Should You Keep Home Office Records?

To support claiming home office expenses, you should keep accurate records for at least five years from when you lodge your tax return. This applies whether you use the fixed rate method or the actual cost method. In some cases, such as where you claim occupancy expenses on your main home, you may need to keep records longer because these may affect future capital gains calculations.

Digital record keeping is usually the easiest way to stay organised. You might store internet bills, phone bills, energy bills, and bank statements in an annual folder, along with your hour logs and any calculations used to apportion costs. By keeping everything together, you can quickly respond if the ATO asks questions about your home office deductions.

What are Common ATO Red Flags for Home Office Claims?

Home office tax deductions can attract ATO attention when they do not match a taxpayer’s role, income level, or work pattern. Very large home office deductions, large jumps from one year to the next, or claims that ignore obvious personal use are all common warning signs. Claims that rely on rough estimates instead of accurate records can also cause issues.

Using the fixed rate while also making separate claims for the same home office running expenses is another red flag. Another issue is claiming occupancy expenses such as mortgage interest and property taxes where your home is not clearly a place of business. The ATO also notices when people claim working from home expenses for a full year even though they only worked from home for part of that year.

How Can ACT Tax Group Help You Substantiate Home Office Claims?

Getting home office deductions right can feel complex, but you do not need to handle it alone. As a registered tax agent, we help you choose between the fixed rate method and the actual cost method based on your personal circumstances. We then help you set up simple record keeping so you can claim deductions with confidence.

We also review your tax return to make sure your home office tax deductions, work related expenses, and other tax deductible expenses are correctly calculated. Our team can assist you when you lodge your tax return online or through our office, making sure that claiming home office expenses supports, rather than harms, your overall taxable income position. With the right tax advice, you can claim expenses you are genuinely entitled to while keeping fully aligned with Australian Tax Office expectations.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)