Fringe Benefits Tax (FBT) on Electric Vehicles: Rules and Exemptions

Published on January 27, 2026

Fringe Benefits Tax (FBT) on electric vehicles can be fully exempt when you meet clear eligibility criteria, delivering meaningful tax savings for both employers and employees. This electric vehicle exemption removes the need to pay FBT on an eligible electric car while still allowing broad private use by a current employee and their family members. Used well, the EV FBT exemption turns electric cars and company cars into practical, cost-effective benefits rather than tax headaches.

What Makes an Electric Vehicle Eligible for FBT Exemption?

An eligible electric car must be a zero or low emissions vehicle, which generally covers battery electric vehicles, hydrogen fuel cell vehicles, and specific plug-in hybrid electric vehicles. The car has to be designed to carry a load of less than one tonne and fewer than nine passengers to qualify for car fringe benefit rules. It also needs to be first held and used as a car after 1 July 2022 and never exceed the LCT threshold for fuel efficient vehicles at its first retail sale, currently $91,387 for the 2025-26 financial year.

To be exempt from FBT, the car must be provided to a current employee for their private use, which includes use by their family members. The vehicle must not have had Luxury Car Tax (LCT) paid on it at any point in its history, including the first retail sale, even if you purchase it second-hand later. If LCT was ever paid, the car is no longer exempt, even if the current price is below the luxury car threshold.

Unsure if your plug-in hybrids still qualify after April 2025?

Schedule a complimentary consultation with us today to review lease agreements and avoid unexpected FBT costs.

How Have Plug-In Hybrid Electric Vehicles Changed From 1 April 2025?

From 1 April 2025, plug-in hybrid electric vehicles (PHEVs) are no longer exempt from FBT, even though some remain classified as fuel efficient vehicles for other tax purposes. Before this date, these low emissions vehicles often enjoyed the same electric vehicle exemption as fully electric vehicles. After this date, they may once again attract FBT and lead to FBT payable unless a specific condition is met.

The main exception applies where an employer agrees to a lease agreement or novated lease agreement for a plug-in hybrid electric car before 1 April 2025 and that agreement continues beyond that date. In that case, the car can remain eligible for the FBT exemption until the end of that lease agreement or novated lease arrangement. New plug-in hybrid electric cars provided after 1 April 2025 are generally not eligible for the FBT electric vehicles concession.

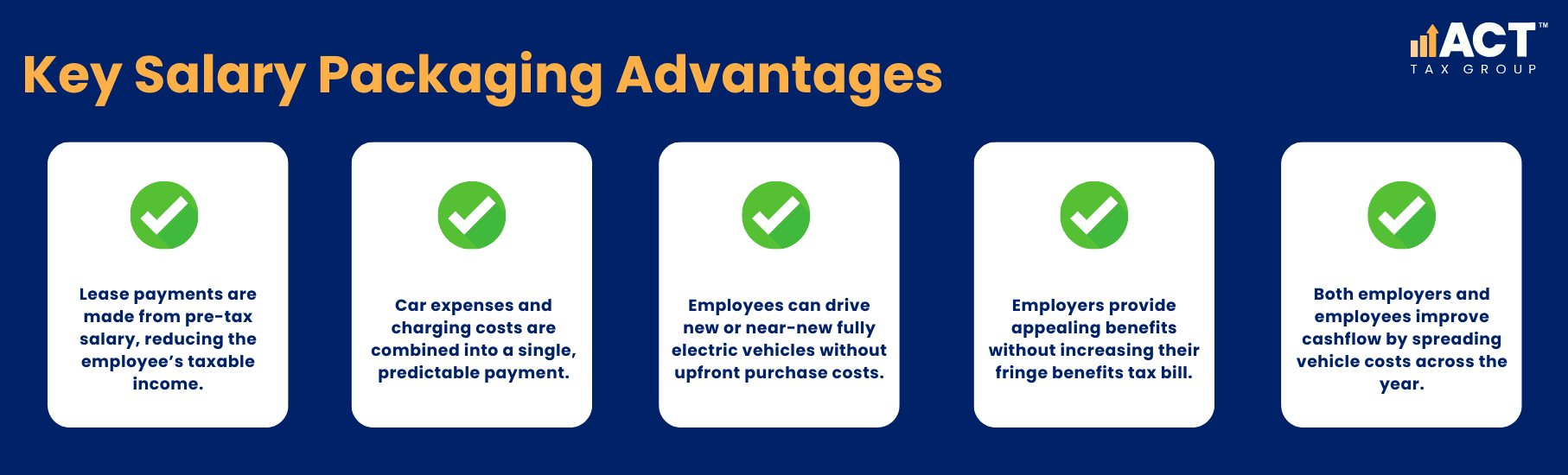

How Does the FBT Exemption Work with Novated Leases and Salary Packaging?

A novated lease is a three-way arrangement where an employee, employer and finance company enter into a lease agreement for a car. Lease payments and car expenses such as registration, insurance, servicing and some running costs are usually paid from the employee’s pre-tax salary. When the car is an eligible electric car, these employer-provided benefits can be FBT exempt, creating strong tax savings without needing the employee contribution method.

Under a novated lease arrangement, the employee’s taxable income reduces because pre-tax salary is used to cover lease payments and many EV car expenses. For eligible electric cars, you do not pay FBT on these running costs, which might include on-road costs such as registration and some electricity costs for charging. (Note: Stamp duty is typically paid at vehicle purchase and is not an ongoing fringe benefit cost.) You still need to keep clear records, but an FBT exemption means you do not pay FBT even though it is a car fringe benefit.

Which Expenses are Covered and Which are Separate Fringe Benefits?

When a car is eligible for the electric car exemption, many EV car expenses and running costs are treated as charging costs exempt from FBT. These include registration, insurance, servicing, repairs, tyres and up to date on road costs. Many of these car expenses form part of the total taxable value for reportable fringe benefits, even though they are FBT exempt.

However, some items are treated as a separate fringe benefit. For example, if your business pays for the purchase and installation of a home charging unit at an employee’s home, that benefit is not covered by the electric car exemption and will attract FBT as a separate fringe benefit valued at its capital cost.

Common Expense Categories

Included in the exemption: registration, compulsory insurance, servicing, repairs, tyres, and most day-to-day running costs.

Charging costs: electricity costs for charging, including EV home charging rate calculations, may be treated as car expenses when linked to business use.

Separate fringe benefits: home charging hardware, certain ancillary benefits not directly tied to the car’s use.

What About Home Charging Costs and the EV Home Charging Rate?

The Australian Taxation Office recognises that many electric cars are charged at an employee’s home using their own electricity. To simplify this, the ATO introduced an EV home charging rate that allows employers and employees to estimate charging costs without complex electricity meter splits. This rate can be used to calculate the electricity consumed for business and private use for FBT purposes.

Using the approved rate (currently 4.20 cents per kilometre as of April 2022) helps you accurately determine car expenses for electric vehicles without needing a dedicated meter or sophisticated monitoring. It’s especially useful where an employer reimburses charging costs or includes an allowance for charging costs in a novated lease arrangement. However, it remains important to keep odometer readings and basic log records so you can show how much of the car’s use is business versus private use.

How Do Reportable Fringe Benefits Work for FBT-Exempt Electric Vehicles?

Even though EVs eligible for the FBT exemption are exempt from FBT, they can still give rise to reportable fringe benefits. The taxable value of the car fringe benefit is calculated under normal rules, but instead of paying FBT, the employer reports this amount on the employee’s income statement for the year. This amount is not added to the employee’s taxable income for income tax purposes, but it is included in the employee’s adjusted taxable income for means-tested government benefits such as Medicare levy surcharge, family assistance payments, and child support assessments.

These reportable fringe benefits affect calculations such as Medicare levy, some family assistance payments, and other income-tested benefits. For example, having a high reportable fringe benefits amount may impact your access to some services, or change repayment levels on certain obligations. Understanding how the taxable value flows through to reportable fringe benefits helps employees make informed decisions about the level of private use they choose.

What Is the Key Record Keeping and Compliance Requirements?

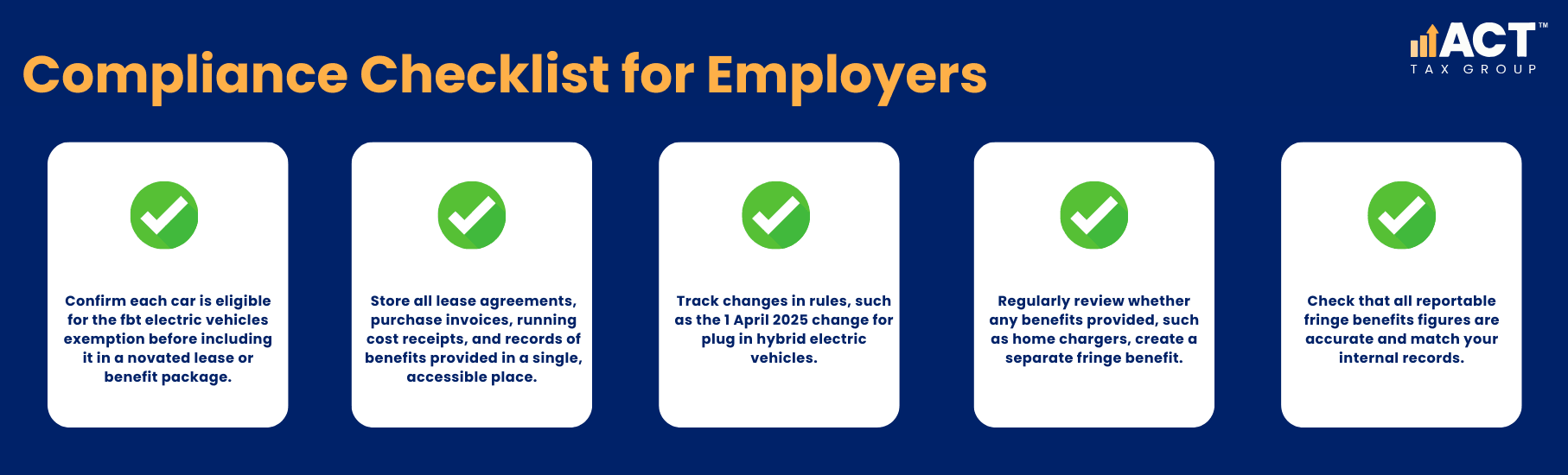

To keep your position strong with the Australian Taxation Office, you need solid record-keeping for any electric vehicles and electric cars you provide. This includes lease agreements, invoices, evidence of on road costs, and logbooks or other tools that show business and private use. Even though the EV FBT exemption means you pay no FBT on eligible cars, you still need to show why they are exempt and how you calculated taxable value for reporting.

For hybrid electric vehicles, plug in hybrid electric models, and fuel-efficient vehicles that are not eligible for the exemption, traditional FBT rules apply. This means you may need to choose between the statutory formula method and operating cost method to determine taxable value. Keeping good records also helps you plan for residual value at the end of a lease and assess whether to renew, buy the car, or move to a new vehicle.

How Can Businesses and Employees Make the Most of the EV FBT Exemption?

For many businesses, offering electric vehicles as part of a car fringe benefit package is now one of the most effective ways to provide value without driving up fringe benefits tax. When the employer agrees to a well-structured novated lease arrangement for an eligible electric car, both the business and employee can share in the tax savings. The key is to ensure the vehicle meets all eligibility criteria and remains under the relevant luxury car tax threshold.

On the employee side, a novated lease on a fully electric vehicle can improve cashflow by lowering taxable income and spreading costs throughout the financial year. When employees understand how reportable fringe benefits work and how they affect things like Medicare levy, they can make better decisions about private use and car choice. For employers, electric cars signal a commitment to sustainability while keeping FBT exposure low and benefits competitive.

As federal government policy and Australian Government guidance continue to evolve, it is essential to revisit your approach often. Whether you already provide company cars or you’re considering your first battery electric or hydrogen fuel cell vehicle for staff, now is a strong time to review your options. With the right advice and careful planning, you can align your fleet, your benefits strategy, and your tax position in a way that genuinely supports your people and your business.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)