Which Electric Vehicles Qualify for the FBT Exemption and How to Check

Published on February 2, 2026

Which Electric Vehicles Qualify for the FBT Exemption and How to Check is a key question if you want to use electric cars without unexpected Fringe Benefits Tax. Choosing the right vehicle and structure can mean you do not need to pay fringe benefits tax on car benefits at all. In this updated guide, we explain which electric vehicles qualify, how the rules work, and how to check before you commit.

Electric vehicles are now a central part of federal government policy to encourage cleaner transport across Australia. The great news is that the government has linked this to real tax savings through the FBT exemption for EV. With a bit of planning, the EV FBT exemption can reduce car expenses for both employers and employees while supporting sustainability goals.

What is the Electric Vehicle FBT Exemption?

The electric vehicle exemption is a specific fringe benefits tax exemption that applies to certain car fringe benefits. In simple terms, if your car and arrangement meet the rules, the FBT exemption means you do not pay FBT on private use of that vehicle. This usually covers driving between the employee’s home and work and other personal trips.

Under this FBT exemption for EVs, the car must be an eligible electric car, and the arrangement must involve a current employee or their family members. The exemption can apply whether the business buys the vehicle outright, enters into a lease, or uses a novated lease arrangement. Even though the benefit can be FBT exempt, some details may still flow through as reportable amounts that can affect taxable income and Medicare levy tests.

Worried your plug‑in hybrid will lose its FBT exemption after 1 April 2025?

Schedule a complimentary consultation with us today to check timing, usage dates and protect your exemption position.

Which Vehicles Count as Zero or Low Emissions?

For FBT exemption electric vehicles, the car must be a zero or low emissions vehicle. This usually means a battery electric vehicle, a hydrogen fuel cell electric vehicle, or in some cases a plug in hybrid electric vehicle. Standard hybrid electric vehicles that cannot be plugged in generally do not qualify under these rules.

The car must also be designed to carry less than one tonne and fewer than nine passengers. This condition focuses on how the car is designed, not how you actually use it. It means most regular passenger electric cars are in, while many larger utes and commercial vehicles fall outside the exemption.

Common Types of Eligible Electric Cars

Battery electric cars powered only by electricity

Hydrogen fuel cell electric vehicles used as passenger cars

Certain plug in hybrid electric cars within the time limits

Second hand electric car that still meets all conditions

How Do The PHEV Rules Change After 1 April 2025?

Plug in hybrid electric vehicles have extra timing rules you must watch. From 1 April 2025, new plug-in hybrid electric cars are no longer eligible for the FBT exemption. Only PHEVs under a financially binding commitment made before 1 April 2025 may remain covered under transitional rules. Only certain PHEVs that were first purchased, held and used before that date may remain covered.

If you plan to use a plug-in hybrid electric car for your business or novated lease, you need to check exactly when it was first held and used. Note that changing employers after 1 April 2025, even within the same corporate group, creates a new commitment and ends the transitional exemption for that PHEV. Past that date, an employer may need to pay FBT again unless another concession applies. Because these details are sensitive, it is wise to get advice for your individual circumstances.

What Role Does the Luxury Car Tax (LCT) Threshold Play?

A major condition for electric vehicle exemption is that Luxury Car Tax has never been payable on the car. The LCT threshold for fuel efficient vehicles acts as a practical cap on the cost of EVs eligible for the exemption. If the value of the car at retail sale is over the fuel efficient LCT threshold in the relevant financial year, the car will usually fall outside the exemption.

This means even fuel-efficient vehicles can miss out if the price is too high. The LCT threshold, sometimes called the LCT threshold, changes over time, so you need to check the right year. Staying safely under the LCT limit is often one of the simplest ways to ensure a car is eligible for the FBT exemption threshold.

Which Popular Electric Vehicles Commonly Qualify?

Many mainstream electric vehicles fall under the LCT threshold and qualify as zero or low emissions. These include a wide range of battery electric vehicles and some hydrogen fuel cell electric models. A number of second-hand electric car options can also qualify, as long as they meet the timing and price rules and have not been subject to Luxury Car Tax.

Not every electric car will be eligible, even if it is clean and modern. Some premium models go above the LCT threshold, and some hybrid electric vehicles do not meet the zero or low emissions definition. The safest approach is to treat each vehicle as unique and test it against the rules before signing a lease or purchase contract.

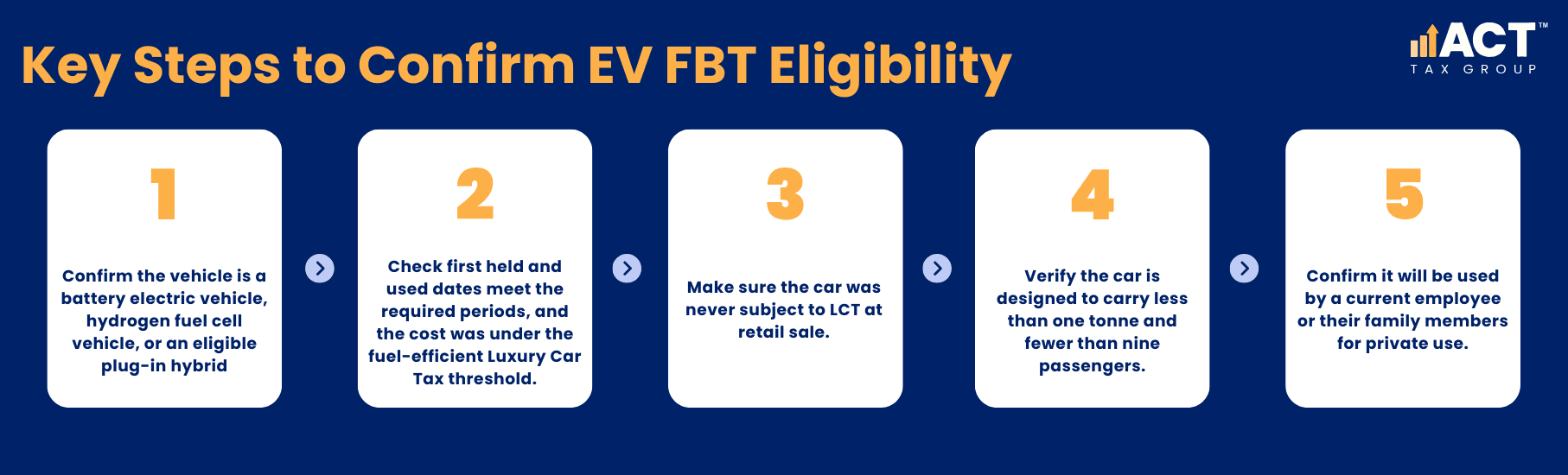

How Can You Check If a Specific EV Is Eligible?

To check whether a vehicle is eligible for the FBT exemption for EVs, start with the basics. Confirm the car is a zero or low emissions vehicle and that it was first held and used in the right financial year window. Make sure the car is designed to carry less than one tonne and fewer than nine passengers.

Next, confirm the car has never attracted Luxury Car Tax and that its value was below the fuel efficient LCT threshold at the time of retail sale. You should also confirm the car will be provided to a current employee or their family members, and that they will have private use, such as parking it at the employee’s home. Keeping written evidence of the car’s cost, dates and design details makes it easier to show the car is eligible for the FBT exemption.

How Does the Exemption Work with a Novated Lease?

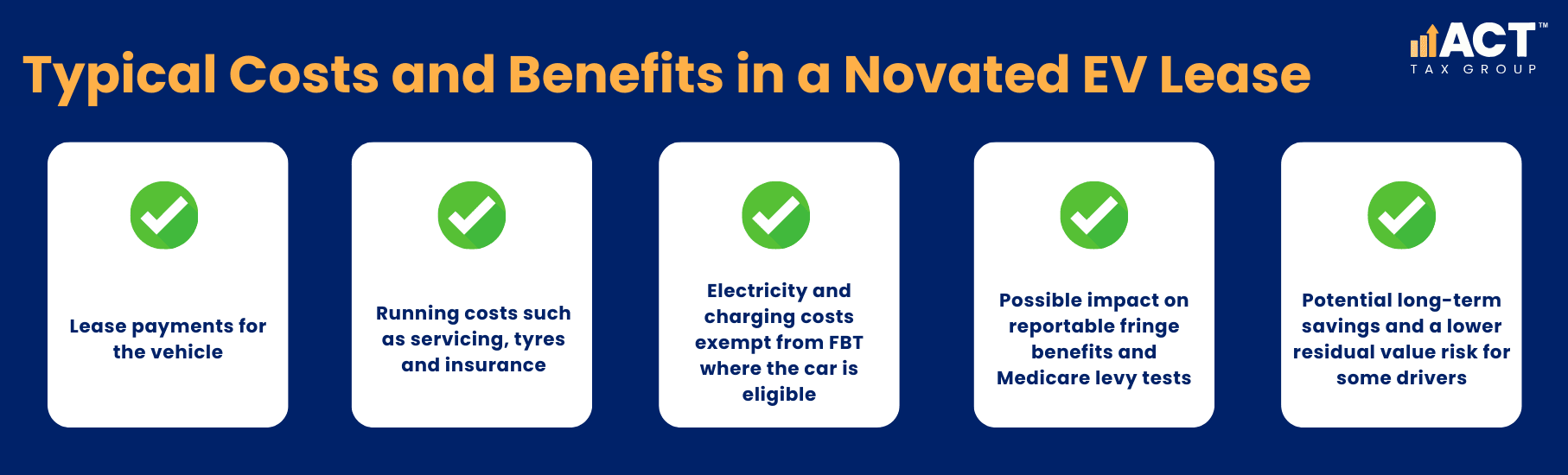

One of the most common ways to use the EV FBT exemption is through a novated lease. A novated lease arrangement is a salary packaging arrangement where an employee agrees that the employer will make the lease payments from their salary. When the car is an eligible electric car, this can mean the employer does not pay FBT on the car fringe benefits at all.

Because these car benefits are FBT exempt, the taxable value of the car fringe benefits can still be worked out but there may be no FBT payable. For many workers, the ability to have running costs, such as registration, insurance and some EV car expenses, packaged into the lease can lead to real tax savings. In many cases, the employee’s salary sacrificed amount comes from pre-tax income, which can reduce taxable income and improve take-home pay.

Are EV Car Expenses and Charging Costs Exempt Too?

If a vehicle is exempt from FBT as an eligible electric car, many related car expenses can also be covered. This may include running costs, registration, insurance, servicing and electricity costs used for charging the car. Charging at an employee’s home may require records or a separate meter to support the claim. When packaged through a novated lease or similar salary packaging arrangement, these costs can be bundled in a simple and predictable way.

It is important to track what is truly related to the car, especially when charging at an employee’s home. Some arrangements may require a meter or other records to support claims that charging costs are exempt. Because each lease and home setup is different, it is best to match the method of claiming to your individual circumstances.

What are Common Mistakes with the FBT Exemption?

One common mistake is assuming any electric car or hybrid electric vehicle will be FBT exempt. In reality, many hybrid electric vehicles that are not plug in models and some plug-in hybrid electric vehicles after 1 April 2025 do not qualify. Another error is overlooking the LCT threshold, which can make an otherwise clean and modern car ineligible for the exemption.

Businesses also sometimes forget that even when a car is exempt from FBT, they may still need to calculate a notional taxable value and report it for fringe benefits tax FBT purposes. If this is not done, there can be issues later with taxable income tests and Medicare levy adjustments for employees. Small oversights in paperwork can turn into bigger costs if FBT payable is later assessed.

How Does This Affect Employers and Employees In Practice?

For an employer, the main benefit is being able to provide car fringe benefits without having to pay FBT on eligible vehicles. This can help attract and retain staff, especially where workers value modern electric vehicles and flexible benefits. It also allows the business to align its fleet with government and community expectations on emissions at a manageable cost.

For an employee, the benefits often show up as easier access to a newer vehicle and better control over car expenses. Packaging car expenses through a novated lease and using an FBT exempt EV can provide tax savings compared to paying for all costs after tax. While some amounts may still be counted when working out taxable income for certain tests, the overall position is often more favourable than a non-exempt vehicle.

When Should You Seek Professional Advice?

You should seek advice whenever you are unsure if a car is eligible for the FBT exemption, or when you are dealing with higher value models near the LCT threshold. Advice is also important when dealing with plug in hybrid electric vehicles near the 1 April 2025 timing rules. A specialist can also help you work out taxable value, deal with reportable benefits, and plan around residual value at the end of a lease.

For ACT and Australia-wide employers, this is an area where a little planning goes a long way. At ACT Tax Group, we help you compare options, review vehicle details and choose structures that are more likely to be eligible for the FBT exemption threshold. This approach helps you reduce the risk of unexpected FBT payable and makes sure the benefits of electric vehicles flow through to your business and your team.

Conclusion: How Should You Approach FBT Exemption For EVs?

To make the most of the FBT exemption for EVs, start by checking whether your chosen vehicle is a zero or low emissions vehicle under the rules. Confirm that its cost is under the LCT threshold and that it has never been subject to LCT. Check that the car is designed within the weight and passenger limits and that it will be used by a current employee or their family members.

From there, consider whether a straightforward purchase or a novated lease arrangement gives you better tax savings and flexibility. Make sure you understand how car expenses, electricity and other running costs will be treated, and how any reportable amounts may affect taxable income. Our team can guide you through which electric vehicles qualify for the FBT exemption and how to check, so you can move forward with confidence and avoid paying fringe benefits tax where the law provides an exemption.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)