How to Determine if Your Electric Vehicle Qualifies for the FBT Exemption

Published on January 27, 2026

How to determine if your electric vehicle qualifies for the FBT exemption is a key question if you want to offer car benefits to staff without a large fringe benefits tax bill. When your electric vehicles are set up correctly, you can often access an EV FBT exemption instead of having to pay FBT on the arrangement. Our team in the ACT helps employers understand the rules so they can make confident decisions and support their people with practical, tax‑effective benefits.

Why This Question Matters for Employers

The electric car exemption does not apply to every car or every situation. You need to check the type of vehicle, the timing of when it was first used, the luxury car tax threshold and how the car is provided to a current employee.

Across Australia, more businesses are adding EVs to fleets, salary packaging arrangements and novated lease setups. The federal government has used the electric vehicle exemption to encourage the move to zero or low emissions transport, especially for fuel efficient vehicles. If you understand how the FBT rules work now, you can plan before the next FBT year and avoid surprises in your fringe benefits tax return.

Worried your EV package might trigger unexpected FBT?

Schedule a complimentary consultation with us today to review your super balances and avoid excess transfer tax.

What Is the Electric Vehicle FBT Exemption?

The EV FBT exemption means that certain car fringe benefits provided to employees are exempt from FBT when they relate to an eligible electric car. In practice, this can reduce the taxable value of a package to zero for FBT purposes, so there is no FBT payable on that benefit. That can be great news for both the employer and the employee because the employer does not have to pay fringe benefits tax and the employee can still enjoy the use of the car.

This fringe benefits tax exemption generally applies to a battery electric vehicle, a hydrogen fuel cell electric vehicle and, in some cases, a plug-in hybrid electric vehicle. To be FBT exempt, the vehicle must meet several conditions, including timing and the luxury car tax rules. The exemption can also extend to many related running costs such as registration, insurance, servicing and some electricity and charging costs exempt from FBT.

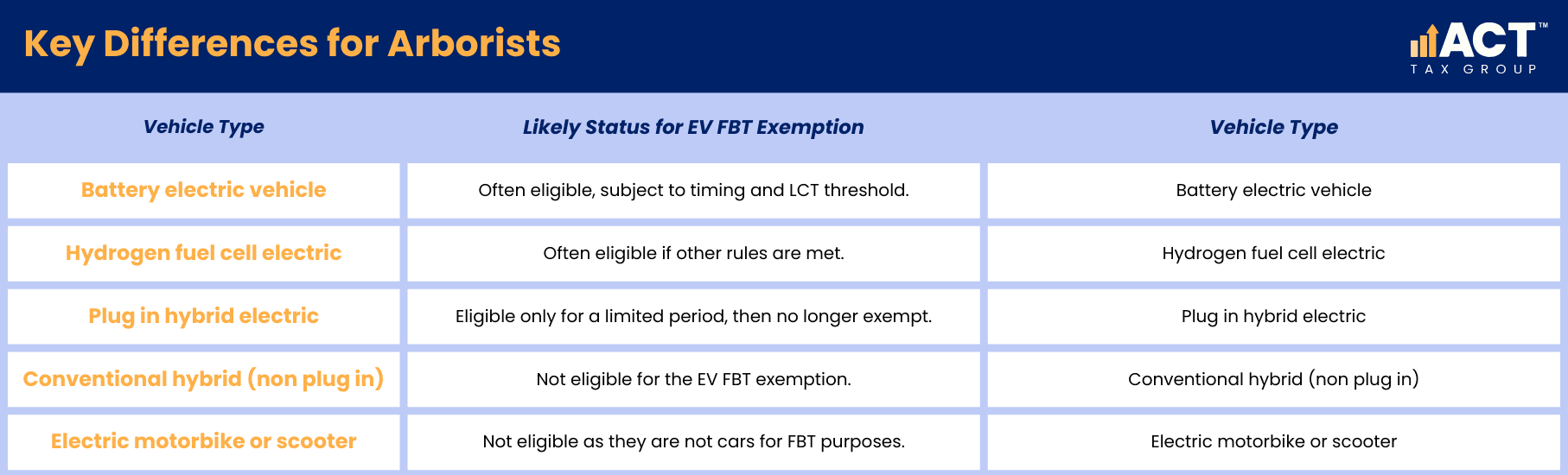

What Type of Vehicle Can Qualify as an Eligible Electric Car?

To be an eligible electric car, the vehicle must be a low emissions vehicle that meets the rules for FBT purposes. It must be a car designed to carry less than one tonne and fewer than nine passengers, including the driver. This means many standard electric vehicles and fuel-efficient vehicles can qualify, but some heavy utes and vans fall outside the rules.

The main EVs eligible are battery electric vehicles, hydrogen fuel cell electric vehicles and, until certain dates, some plug in hybrid electric vehicles. Electric motorbikes and scooters do not qualify because they are not treated as a “car” for FBT purposes. A second-hand electric car can also qualify as long as it meets the same conditions as a new vehicle.

When Must Your EV First Be Held and Used to Be Eligible for the FBT Exemption?

Timing is a key part of working out if your EV is eligible for the FBT exemption. The car must have been first held and first used as a car on or after 1 July 2022. This includes both new cars and a second-hand electric car that was first used after that date.

If the vehicle was first purchased and used before the start date, it will not qualify for the electric vehicle exemption, even if you only now start using it as part of a salary packaging arrangement. This rule can be easy to overlook when you buy a used vehicle or transfer a car within a group. It is worth confirming the original retail sale date and first registration so you can be sure about the timing.

How Does the Luxury Car Tax Threshold Affect Whether Your EV Is Exempt?

The luxury car tax threshold plays a major role in deciding whether an electric vehicle is eligible for the FBT exemption. If LCT has ever been payable on the vehicle, it cannot qualify for the EV FBT exemption, even if it is otherwise a low emissions vehicle. This is why the car’s original cost and the LCT threshold for that financial year matter.

For fuel efficient vehicles and many electric cars, there is a higher LCT threshold compared with other cars. You need to check whether the GST‑inclusive value of the vehicle at retail sale was below the relevant luxury car tax threshold for that year. If the vehicle’s cost was under the threshold and LCT was never payable, that part of the test is usually satisfied.

Recent Luxury Car Tax Thresholds – Fuel Efficient Vehicles

Financial Year | Fuel Efficient LCT Threshold | Comment |

|---|---|---|

2025–26 | $91,387 – High threshold for fuel efficient vehicles | Helps more EVs stay under the luxury car tax line. |

2024–25 | $91,387 – Similar high threshold | Many mid‑range EVs remained below this level. |

2023–24 | $89,332 – Slightly lower threshold | Some premium EVs crossed into LCT territory. |

If your EV’s cost was above the LCT threshold in the original year of purchase, LCT may have been payable, and the car will not be eligible for the FBT exemption. If the cost was below the threshold, you still need to work through the other conditions. For some employers, this makes mid‑range fuel efficient EVs more attractive than high‑end models.

Who Must Use The Car For The Electric Vehicle Exemption To Apply?

The car must be provided for the use of a current employee or their family members to be eligible for the EV FBT exemption. This may be through a novated lease arrangement, a salary sacrificed benefit or a company car provided mainly for private use. The key is that the benefit arises because of the person’s employment, not just because they are an owner or shareholder.

If a vehicle is only used by business owners who are not treated as employees, the car may not qualify for the fringe benefits tax exemption for EVs. In many small businesses, people wear multiple hats, so it is important to clearly document employment roles and any salary packaging arrangement. This can help show that the car fringe benefits are linked to employment and not a personal drawing.

What Changes Affect Plug in Hybrid Electric Vehicles From 1 April 2025?

Plug in hybrid electric vehicles are treated differently from battery electric cars and hydrogen fuel cell electric vehicles. From 1 April 2025, new PHEV arrangements are no longer eligible for the FBT exemption. Existing arrangements may still qualify where: (1) the PHEV was used or available for use before 1 April 2025, and (2) there is a financially binding commitment to continue providing the vehicle on or after that date.

This means employers using a plug-in hybrid electric vehicle under a novated lease or lease entered into before 1 April 2025 and used or available for use before that date may retain access to the FBT exemption for EVs until the end of the agreement. As of 1 April 2025, new PHEV salary packaging arrangements are no longer eligible for the FBT exemption. It is important to review the residual value and term of your lease so you know how long any FBT savings may last.

How Do You Confirm the Vehicle Meets the “Car” Definition for FBT Purposes?

To qualify as an eligible electric car, the vehicle must meet the FBT definition of a car. It needs to be a car designed mainly to carry passengers and to carry less than one tonne of load. It also must not be built to carry nine or more passengers.

This means some larger utes and vans may fall outside the EV FBT rules because their designed payload is more than one tonne. On the other hand, many compact and mid‑size EVs clearly meet the less than one tonne test. Checking the manufacturer’s specs is a simple but important step before you assume your electric vehicle exemption applies.

What Records Do You Need to Support Your EV FBT Exemption Position?

To show that your vehicle is eligible for the FBT exemption, you need clear, well‑kept records. These documents help you prove that you do not have to pay FBT on the benefit, and they support your calculations if any part of the benefit remains taxable. Good record‑keeping also makes your year‑end FBT process much easier.

You should keep purchase contracts, tax invoices, registration papers, lease or novated lease agreements, and evidence that the cost was below the relevant luxury car tax threshold. You may also hold internal policies about private use, travel between work and the employee’s home and any limits on car use by family members. Together, these documents build the story of why your EV is FBT exempt.

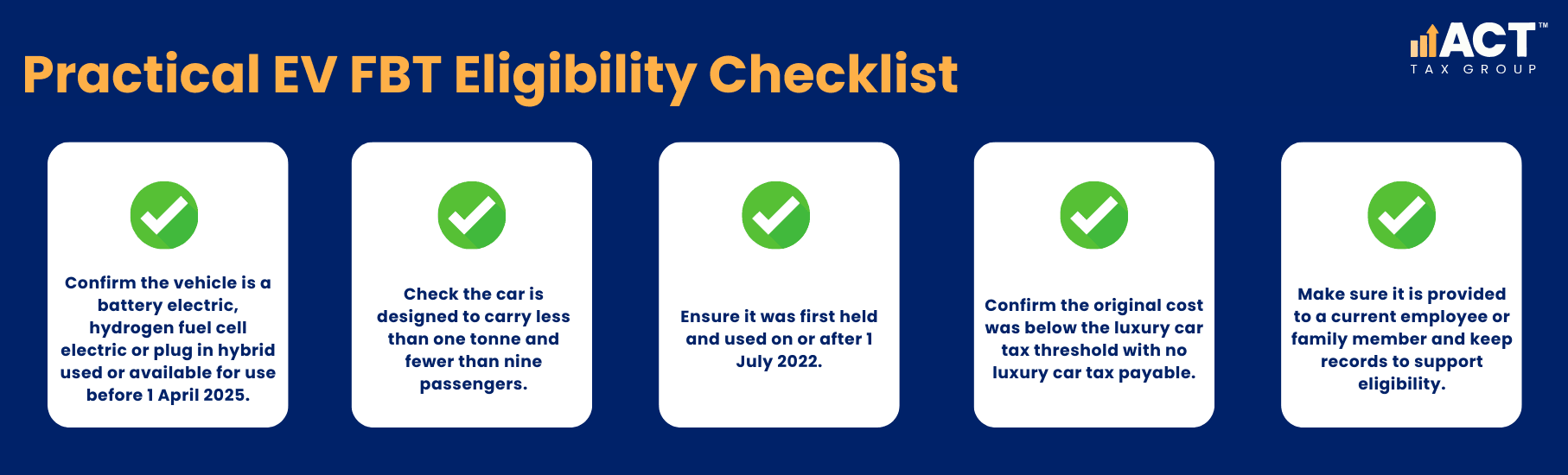

How Do You Work Through a Practical Checklist to See If Your EV Is Eligible?

A simple checklist can help you decide whether your EV qualifies for the electric car exemption. Working through these steps before you commit to a lease or purchase can help you avoid unexpected FBT payable later. It also supports clear planning around tax savings and running costs.

If you can answer “yes” to each step, there is a strong chance your vehicle is eligible for the FBT exemption and you will not have to pay fringe benefits tax on that car. You still need to consider the employee’s overall taxable income, the impact on Medicare levy and how the benefit fits with your broader package. It is also worth checking the residual value and end‑of‑term options so everyone knows what happens when the lease ends.

How Can ACT Tax Group Help You Make The Most Of EV FBT Savings?

Our team regularly helps employers assess whether an electric vehicle is eligible for the FBT exemption and what that means in dollar terms. We walk through the cost of the vehicle, its running costs, electricity use and any charging costs exempt from FBT to build a clear view of the overall benefit. We also compare different options, such as an outright purchase versus a novated lease arrangement, so you can see the practical tax savings over the full financial year.

We understand that every employer and every employee has individual circumstances, including cash‑flow needs, vehicle preferences and how much private use is expected. By combining this with the FBT rules, we can help you choose EVs that are more likely to stay exempt and avoid you having to suddenly pay FBT later. Our goal is to help you offer benefits that support your team, manage tax, and fit neatly with your long‑term plans.

Conclusion: What Should You Do Next To Check If Your EV Qualifies?

The key to working out how to determine if your electric vehicle qualifies for the FBT exemption is to test it step by step against the rules for vehicle type, timing, luxury car tax threshold and how the benefit is provided. When an EV is eligible for the FBT exemption, the employer does not have to pay FBT on the car, which can create meaningful tax savings and make salary packaging arrangement options more attractive. The right structure can also help employees access cleaner vehicles with lower running costs while keeping their overall taxable income in check.

If you are thinking about adding battery electric or hydrogen fuel cell vehicles to your fleet, setting up a novated lease for staff, or checking whether your current cars are still exempt, now is a good time to review your position before the current FBT year ends on 31 March 2026. Note that PHEV arrangements are no longer eligible if entered into after 1 April 2025. Our team at ACT Tax Group can help you assess your vehicles, model the after‑tax outcomes and make sure you are not missing out on an exemption you are entitled to. Reach out to us to discuss your EV FBT options so you can move forward with clarity and confidence.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)