The Benefits of Consolidating Your Super: Save on Fees and Grow Your Balance

Published on November 25, 2025

Consolidating your super into one fund is one of the smartest money moves you can make for your retirement savings and financial future. When you have multiple super accounts scattered across different funds, you’re often paying multiple fees that quietly eat away at your balance every single year. By bringing everything together into one super fund, you can cut costs, simplify your life admin, and let your money grow the way it should.

Many Australians end up with multiple super accounts simply by changing jobs, and it’s easy to lose track of your super when each employer sets up a new account by default. The problem is that each fund keeps charging you fees and insurance premiums, even if you’ve forgotten the account exists. Understanding how to consolidate your super can make a real difference to your financial future.

What Does Consolidating Your Super Actually Mean?

Consolidating your super means moving all your money from your other super accounts into one main super fund that you choose to keep. You transfer the super balance from each of your other funds into one account, and then close those extra accounts once transfers are complete. This process is straightforward and can usually be done online through ATO online services or directly with your chosen fund.

When you consolidate your super, you’re bringing together all your employer contributions and personal contributions you’ve made over the years. Instead of having your money scattered across multiple funds, you get one clear picture of your account details and how your money is growing. This makes it much easier to track of your super and understand what your account means for your retirement savings.

Maximising your Stage 3 tax cut benefits?

Schedule a complimentary consultation with us today to identify all your super funds and reduce unnecessary costs.

Why Do Multiple Super Accounts Cost You So Much Money?

When you hold multiple super accounts, you’re paying multiple sets of fees every single year, and those costs compound over time. Each fund charges administration fees, investment fees, and may charge insurance premiums, so having three accounts instead of one can mean you’re paying significantly more in total costs. Over a working lifetime, paying multiple fees can take thousands of dollars away from your retirement savings.

The real danger is that you might have lost track of your super, and forgotten super sitting in old accounts keeps charging you fees even when you’re not paying money in. When you have unclaimed super or other accounts you don’t remember, those funds are still deducting fees from your balance. Consolidating your super eliminates this problem by bringing everything into one place where you can actively manage it.

How Can Consolidating Your Super Help You Save On Fees?

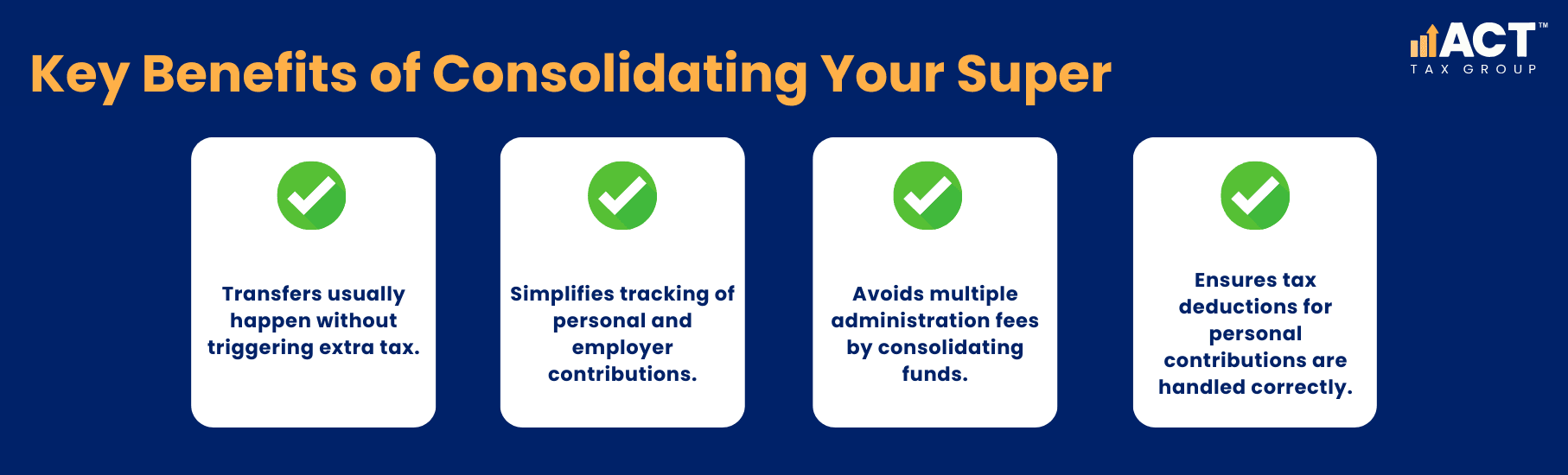

Consolidating your super into one account means you pay only one set of administration fees and investment fees instead of multiple sets across different funds. When you transfer super from your other fund into one main account, you immediately stop paying duplicate costs that were quietly reducing your balance. More of your money can now stay invested and working for your financial future.

The real benefit becomes clear when you look at numbers over time—even saving just a couple of hundred dollars a year in fees can add up to many thousands of dollars more by retirement. When you combine your super, your total balance in one fund might also make you eligible for different fee structures or investment options that larger balances can access. This means consolidating your super isn’t just about cutting costs—it’s about giving your money the best chance to grow.

What Should You Check Before You Consolidate Your Super?

Before you submit a consolidation request, it’s important to review the insurance cover you have in each of your existing super funds. Some funds include life insurance, total and permanent disability cover, or income protection that might not be available in your new fund. If you close an account without checking what insurance you’ll lose, you could end up unprotected or paying more for cover elsewhere.

You should also take time to compare your funds and past performance to choose the best fund to keep as your main account. Look at the fees, investment options, and services offered by each fund, and consider seeking professional advice if your situation is complex. Understanding what each fund offers helps you make a consolidation request with confidence.

How Do You Find All Your Super Accounts Using myGov?

If you suspect you have multiple super accounts but aren’t sure, your myGov account is the best place to start looking. When you log into myGov and link to the Australian Taxation Office, you can see all the super funds linked to your tax file number. This ATO online services tool shows you any lost super, forgotten super, unclaimed super, or other accounts that might be held for you.

Once you’re in ATO online, you can look at your super section and see all your other super accounts listed with their balances. This gives you a complete picture of where your money is scattered across different funds. From here, you can usually start the process to transfer super or submit a transfer request directly without contacting each fund individually.

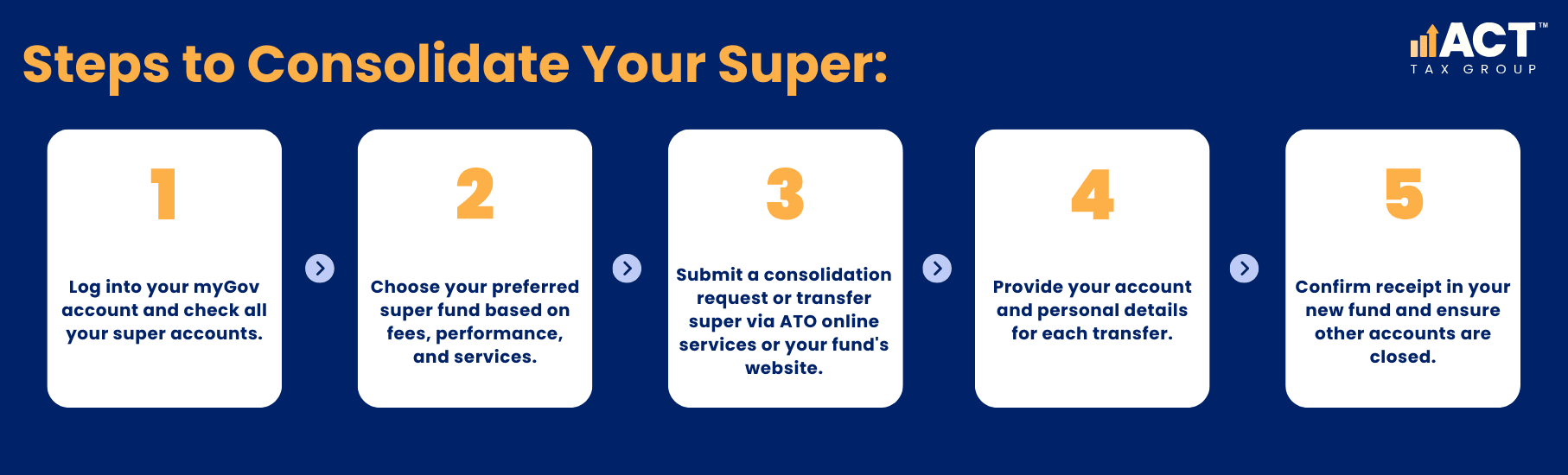

What Are The Simple Steps To Actually Consolidate Your Super?

Consolidating your super follows a few simple steps that most people can complete online without needing to visit an office. First, log into your myGov account and use ATO online services to find all your super accounts and check your account details are correct. Decide which super fund you want to keep as your main account based on fees, performance, and services.

Next, you can submit a consolidation request or select transfer super through either ATO online services or directly through your chosen fund’s website. Provide your account details and personal details for each account you want to transfer, and authorise the transfer. You should receive confirmation when the money arrives in your new fund and then verify that your other accounts are closed.

How Does Tax And Personal Contributions Work When You Consolidate?

When you consolidate your super, the money transfers between complying funds usually without triggering extra tax, which is good news for your retirement savings. However, if you’ve made personal contributions to any of your super funds and want to claim a tax deduction, you need to make sure that’s sorted before you transfer super. Let your new fund know about any personal super contributions you’ve made so they can help you claim the deduction correctly.

You should also check how each fund records your employer contributions and personal contributions to ensure everything is tracked properly in your new account. Make sure your tax file number and personal details are completely correct in your chosen fund before the transfer happens. If you’re uncertain about any tax matters, seeking professional advice can help you avoid problems later.

When Might It Make Sense To Keep More Than One Super Fund?

While consolidating your super into one fund is usually the best choice, there are situations where keeping more than one super account might be right for your personal situation. For example, if you have a defined benefit fund or a fund with unique insurance features, you might want to keep those separate and only consolidate your other accounts. You could move your multiple accumulation accounts into one fund while keeping your special fund separate.

You might also decide to delay consolidation if you’re waiting on an insurance claim, dealing with a dispute, or need further information about one of your accounts. In these complex situations, it’s worth seeking independent advice from a financial adviser who can look at your personal situation. The right decision depends on your specific circumstances.

How Can A Financial Adviser Help With Consolidating Your Super?

A financial adviser can help you work through the decision of which fund to keep, and which accounts to close based on your personal situation. They can compare fees, investment performance, insurance options, and services across all your funds to show you exactly what you’d gain by consolidating. This guidance is especially valuable if you have large balances, complex insurance needs, or aren’t sure which fund is best for you.

An adviser can also help you think about how consolidating your super fits into your broader financial strategy and retirement planning. They can explain how different choices about which fund to keep might affect your tax position and investment returns. Having professional advice means you can move forward with confidence rather than guessing what’s best for your retirement savings and financial future.

Conclusion

If you think you might have multiple super accounts, the first step is simple: log into myGov and link to the Australian Taxation Office using ATO online services. This takes just a few minutes and immediately shows you exactly what super accounts exist in your name. From there, you can see your super balance in each account and check whether any money is sitting as lost super or forgotten super.

Once you’ve seen all your accounts, gather your latest statements and information from each fund so you can compare fees and performance. If you feel confident making the choice yourself, you can submit a consolidation request online and be done within a few weeks. If you’re uncertain or your situation feels complicated, reaching out to a financial adviser for independent advice is a smart move that could save you time and help you avoid mistakes.

Consolidating your super is genuinely one of the most effective ways to protect your retirement savings and take control of your financial future. By bringing all your money into one account, you cut multiple fees, simplify your life admin, and make it easier to grow your super balance over time. The process is straightforward, the benefits are real, and the sooner you take action, the sooner your money can work harder for you.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)