Understanding Salary Packaging for Arborists: How It Can Save You Tax

Published on April 14, 2026

Understanding salary packaging for arborists: how it can save you tax matters when you’re already worrying about cash flow, winter slow-downs, and keeping your crew safe on every job. You might have heard other business owners talk about using salary packaging to pay less income tax, but it can be hard to see how it actually fits your tree services business without adding more admin or risk, especially when you’re also juggling broader cash flow management for arborists.

How Does Salary Packaging Work for Arborists?

Imagine it’s the end of a big summer, you’ve had strong months of pre-tax income, and your senior climber asks whether they can use salary packaging to get more money in their super fund or help with car repayments. At the same time, your bookkeeper mentions that some not-for-profit organisations and other employers use salary sacrifice to help staff pay less tax without changing the full salary too much.

Worried salary packaging could add ATO risk or extra admin?

Schedule a complimentary consultation with us today to set up simple, compliant salary packaging that suits your arborist crew and cash flow.

What Salary Packaging Actually Is

Salary packaging (also called salary sacrifice) is when an employee agrees to give up part of their pre-tax salary in exchange for specific benefits that the employer offers. Instead of all of their pay going as cash into their bank account, some of their pre-tax dollars are used for approved expenses or non-cash benefits.

In a basic salary sacrifice arrangement, an employee’s pre-tax income is reduced by the value of the selected benefits. Because tax is calculated on the lower salary, they may pay less income tax. However, salary packaging does not always reduce Medicare Levy Surcharge or other income-tested obligations, because reportable fringe benefits and reportable employer super contributions can still count for those tests. The employer pays the cost of the benefits out of the reduced salary, and in some cases may also have to pay FBT if certain benefits are not exempt benefits.

For an effective salary sacrifice arrangement, it has to be set up before the income is earned, clearly documented, apply to future salary only, and follow Australian Taxation Office rules. Once you understand those basics, you can decide which salary packaging benefits actually make sense for your crew.

How Salary Packaging Works for Arborists in Real Life

For arborists in the ACT, salary packaging affect mostly shows up in three areas: extra super contributions, vehicles, and a small set of other benefits that might be eligible expenses. The trick is to focus on simple, approved benefits that are easy to explain to your team and don’t create extra ATO stress, and to stay on top of common tax deduction mistakes so your claims stay accurate and compliant.

When you use salary packaging correctly, the salary sacrifice arrangement reduces the employee’s taxable income, which means less income tax and possibly more money overall, even though their employee salary on paper looks lower.

Salary Sacrifice into Super: Often the Easiest Starting Point

If you want to use salary packaging without diving into complex Fringe Benefits Tax rules straight away, extra super is usually the simplest place to start. Instead of taking all of their salary as cash, your crew member can choose to salary sacrifice some of their pre-tax income into their super fund.

Here’s how this type of salary packaging works in practice:

The employee agrees to give up part of their pre-tax salary.

The employer pays that agreed amount into the employee’s super fund as a salary-sacrifice contribution. The employer must still pay compulsory Superannuation Guarantee on the employee’s pre-sacrifice ordinary time earnings, because salary sacrifice cannot reduce SG obligations.

Because this amount comes out of pre-tax income, the employee’s taxable income is lower, so they may pay less income tax.

This kind of salary sacrifice arrangement can improve financial wellbeing over the long term, especially for a senior climber or crew leader who wants to build retirement savings and is comfortable with slightly lower after-tax income today; older business owners might also look at strategies like the Downsizer Scheme to boost super when planning for retirement.

Employees also need to watch the concessional contributions cap, because salary-sacrifice contributions count towards it. The general concessional cap is $30,000 from 1 July 2024.

Vehicles, Fringe Benefits Tax and Employee Contributions

Many arborist businesses already provide utes or vehicles to crew. Once there is any personal use, that often becomes a common fringe benefit. When a vehicle is part of salary packaging arrangements, you need to think about whether you may have to pay FBT.

In simple terms, a car or ute made available for private use is usually a fringe benefit. The employer pays the associated costs such as fuel, rego, insurance and loan repayments or novated lease, and may also have to pay FBT. Sometimes, the employer asks for employee contributions from after tax income to reduce the taxable value of the fringe benefit and therefore reduce or remove the need to pay FBT.

The main points to keep in mind are:

A car made available for private use is usually a fringe benefit. For some eligible commercial vehicles such as certain utes and vans, limited private use may be exempt from FBT, so the facts matter.

If you offer a novated lease or allow the employee to package eligible vehicle costs, you need to understand the FBT treatment.

The way tax is calculated on car fringe benefits can be complex, so simple, clear policies and accurate records really matter.

For a small arborist business, you want any vehicle salary packaging to be straightforward, fair across the crew, and not create surprise FBT bills.

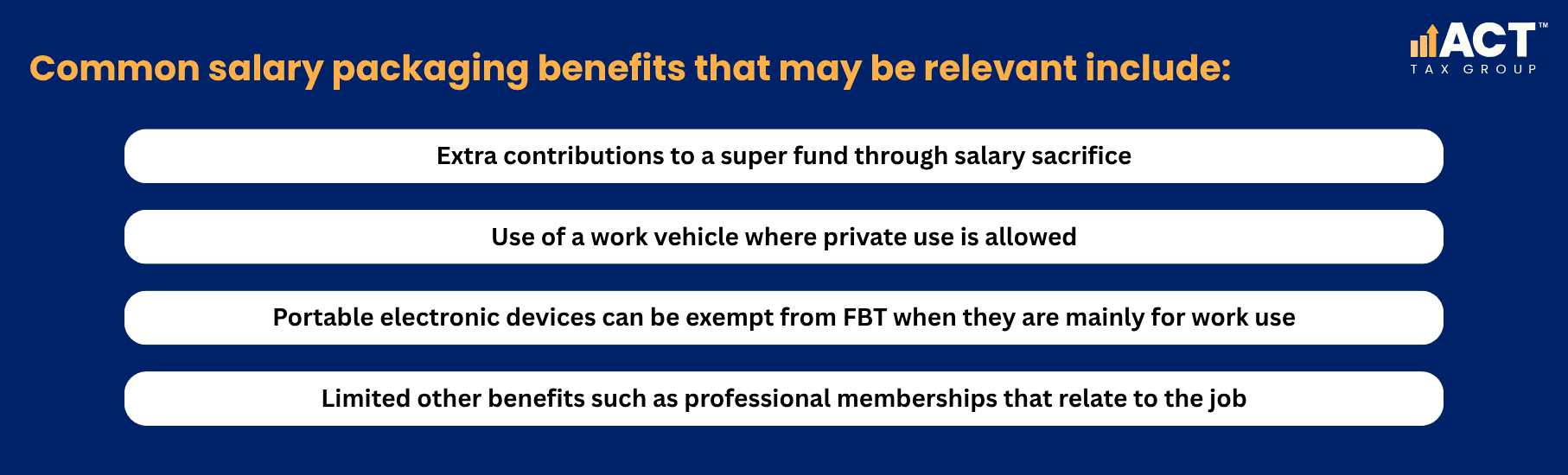

Other Specific Benefits: What Might Be Possible

Beyond super and vehicles, some employers use salary packaging for other benefits that count as approved expenses or approved benefits, depending on the rules. For arborists, this might include:

Work‑related professional memberships

Portable electronic devices such as mobile phones or tablets used mainly for work

In some industries, limited meal entertainment, though this has particular tax implications

If an employer offers these other benefits as part of salary packaging, they do so by swapping part of the employee’s pre-tax salary for these specific benefits. In some cases, these are exempt benefits for FBT purposes; in other cases, the employer may have to pay FBT or factor in additional costs and administrative fees charged by any external salary packaging providers.

The key is to stick to simple, clearly related work benefits rather than trying to package every living expense. Mortgage payments, school fees and general living expenses are not typical salary-packaging options for a standard private-sector arborist business and usually require specialist advice. Those benefits are more commonly discussed in not-for-profit or concessional employer settings.

How Salary Packaging Affects Take Home Pay and Government Benefits

Most crew members want to know one thing: “Will I have more money in my pocket, or less?” Salary packaging works by trading full salary in cash for benefits paid with pre-tax dollars. This can lead to less income tax and tax savings overall, but only when the chosen benefits are worth more than the cash they give up and any additional costs.

Here’s what usually happens:

Pre-tax salary goes down because part of it is swapped for certain benefits.

This reduces your taxable income, so you may pay less tax and less Medicare Levy Surcharge if you were above certain thresholds.

Take home pay (the cash arriving in your bank account) may be lower, but when you add the value of the packaged benefits, your total position can be similar value or better.

Salary packaging can also affect government benefits and income tests, because income statement reporting, reportable fringe benefits, and reportable employer super contributions can change the amounts used for some assessments. That’s why each crew member should think carefully about their broader financial situation, including any family payments they receive, before signing up for salary packaging, and why owners should also watch how salary structures combine with turnover when deciding whether to stay under the GST registration threshold.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

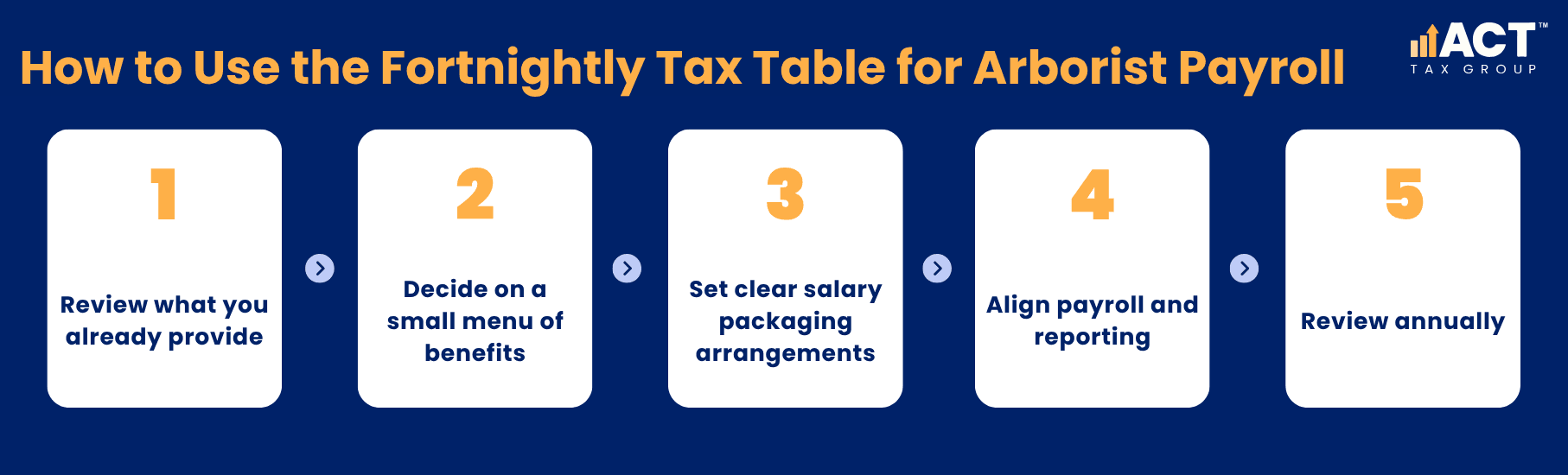

Operational Steps for an Arborist Business Considering Salary Packaging

As an arborist owner, you don’t need to become a tax expert to offer basic salary packaging, but you do need a solid operational process. The aim is to protect the business, keep employee satisfaction high, and avoid any confusion at BAS and GST reporting or year‑end.

A simple, arborist‑friendly sequence might look like this:

Review what you already provide

List any non-cash benefits you already give staff: vehicles, phones, professional memberships, or other benefits. Work out where fringe benefit rules might already apply and whether you might need to pay FBT.Decide on a small menu of benefits

Start with salary sacrifice into a super fund as your main option and consider whether you also want to offer a basic vehicle benefit or mobile phones as salary packaging benefits. Keep the list short so admin and tax implications stay manageable.Set clear salary packaging arrangements

For each type of benefit, have a simple, written salary sacrifice arrangement explaining how much pre-tax income will be packaged, what specific benefits the employee receives, and how this will change their take home pay and after-tax income.Align payroll and reporting

Make sure your payroll setup can handle pre-tax and after-tax adjustments, track employee contributions, and report correctly through Single Touch Payroll (STP) so employees receive accurate income statement information.Review annually

Each year, check whether any rules from the Australian Taxation Office have changed, whether associated costs (like FBT or administrative fees) still make sense, and whether the salary packaging works for both the business and the crew.

This keeps the focus on smooth operations, accurate reporting, and keeping your people informed, rather than chasing short‑term tax tricks, and it also supports cleaner BAS data so you’re less likely to run into BAS and GST reporting issues or ASIC‑related late fees and penalties for missed obligations.

When Salary Packaging Might Not Be Worth It

Salary packaging isn’t always the right move. In some cases, the extra admin, additional costs, or need to pay FBT can cancel out the tax savings. As an arborist owner, you should be cautious when:

The benefit is mostly personal living expenses such as general living expenses or mortgage payments, and the structure is complex.

The value of the fringe benefit is modest, but the cost to pay FBT and manage the paperwork is high.

An employee’s income is already low enough that there isn’t much income tax to save by reducing their taxable income.

In these situations, it may be simpler for the employee to receive their full salary, pay tax in the usual way, and manage their own after tax money, instead of using salary packaging, particularly where income levels and family circumstances interact with Family Tax Benefit Part A entitlements.

Bringing It All Together for Your Arborist Crew

For a small or growing tree services business, the best use of salary packaging is usually a small number of clear, practical options that genuinely improve financial wellbeing for your team. Extra super contributions through salary sacrifice, carefully structured vehicle use, and a few work‑related benefits like mobile phones or professional memberships can all be considered without turning your office into a full‑time payroll department.

If you’d like help working through which specific benefits are suitable for your business, how salary packaging arrangement reduces taxable income in your case, and when the employer pays FBT or other costs, ACT Tax Group can walk you through it in a way that fits your crew size, work mix and cash flow.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)