Capital Gains Tax Explained for Electrical Business Owners: The Basics

Published on April 7, 2026

Capital Gains Tax Explained for Electrical Business Owners: The Basics is about how capital gains tax is calculated when you sell a major asset in your business and what that means for your money. As an Australian tax resident running an electrical business, you want to know when you will actually pay tax on a profit and how it flows through to your taxable income and other tax obligations.

Why Capital Gains Tax Matters When You Sell Up

You might be flat out on the tools and only think about tax when your BAS or GST reporting is due, but capital gains can suddenly matter when you sell a property, change structure, or plan your exit. If you sell your workshop, transfer an investment property used by the business, or sell shares in your company, you could end up with a capital gain or loss in the same financial year that pushes up your assessable income and the tax you pay.

Understanding how Capital Gains Tax (CGT) fits into your overall financial situation means you can make more informed decisions about when to sell, how to structure contracts, and what records your accountant will need. It also helps you avoid surprises when you see the net capital gain calculated in your tax return, instead of feeling like gains tax is a separate tax that came out of nowhere.

Worried a property sale will blow out your CGT bill?

Schedule a complimentary consultation with us today to map the CGT impact on your sale and cash flow.

What Capital Gains Tax Actually Is

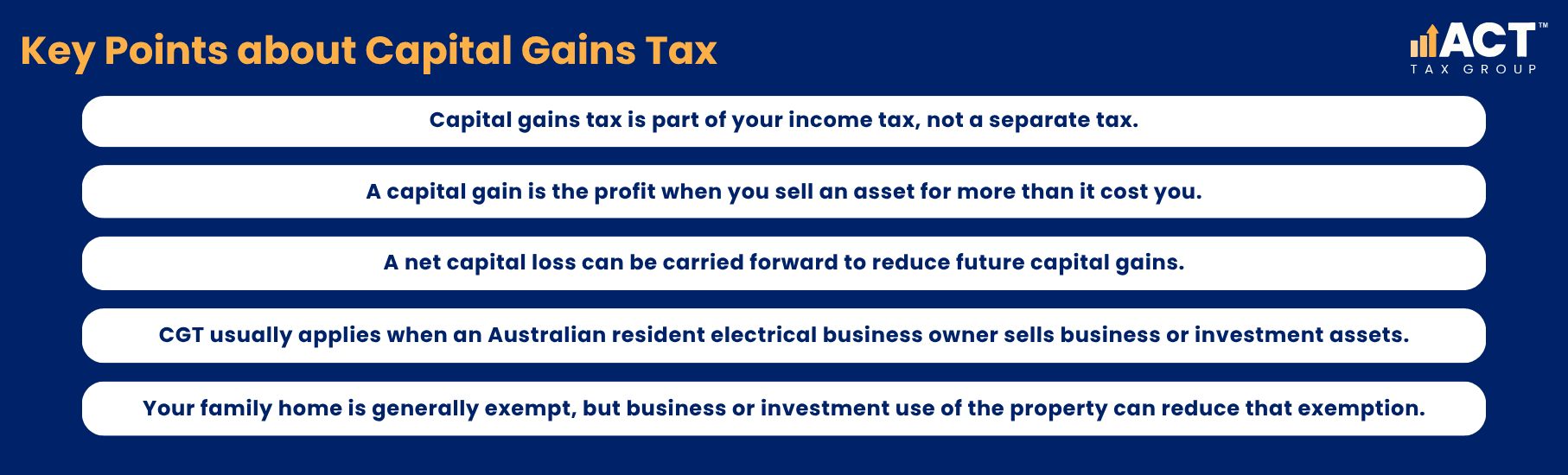

Capital gains tax is not a separate tax that sits on its own; it is part of your income tax. When you sell an asset for more than it cost you, the profit is called a capital gain, and that gain is added to your taxable income for that income year. When you make a net capital loss instead, you do not get a cash refund, but you can carry forward that loss to reduce capital gains in future years.

For an Australian resident individual, CGT usually applies when you sell CGT assets such as property, goodwill, shares or units. Some personal-use assets may be exempt, and depreciating business assets are often dealt with under separate depreciation rules instead. Your family home, when it is your primary residence for tax purposes, is generally exempt from capital gains tax. Once you start using part of your home or land for the business or treat it as an investment property, that exemption can change and some of the profit may fall into the CGT net.

Which Assets in Your Electrical Business Can Trigger Capital Gains

Most electrical business owners will have a mix of tools, vehicles, equipment, and sometimes land or buildings tied up in the business. Not every asset will involve capital gains when you sell, but some types of property are much more likely to raise CGT questions than others.

The most common trigger is property. Selling a workshop, office, or yard used by your electrical business will often result in a capital gain or loss, depending on the sale price and the original purchase cost. Investment property that has been rented out, even if related to your business, is also subject to CGT rules. Another area is ownership interests: If you sell business assets such as goodwill, or you sell shares in a company or units in a trust, a CGT event may happen. If the asset sold is a share or trust interest, extra eligibility conditions can apply before any small business CGT concessions are available.

Many day-to-day items like tools, equipment and work vehicles are usually dealt with under the depreciation rules rather than standard CGT rules. If a depreciating asset was used solely for business or another taxable purpose, CGT generally does not apply, but any private or other non-taxable use can affect the tax outcome. Even so, private use of a vehicle or similar asset can affect how any gain or loss is treated for tax purposes, so it is still important to have clear records in your accounting system.

How Capital Gains Tax Is Calculated Step by Step

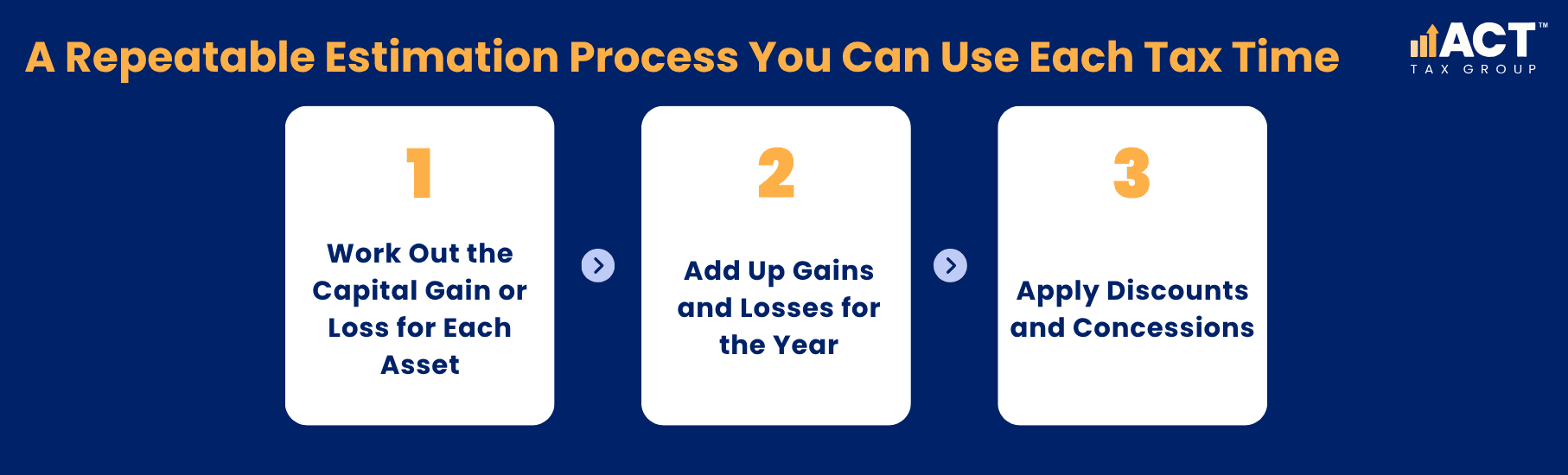

When you ask, “how is capital gains tax calculated?” it helps to strip it back to a simple, repeatable process. The aim is to arrive at your total capital gains and capital losses for the year and then work out your net capital gain that feeds into your income tax.

Step 1: Work Out the Capital Gain or Loss for Each Asset

The first step is to work out the capital gain or loss for each asset you sell. To do this, you compare what you receive when you sell with what it cost you to buy and hold the asset. The amount you receive is often the sale price or market value; the amount it cost you is called the cost base.

The cost base can include the purchase price and certain other costs such as stamp duty, legal fees, brokerage, and some non-deductible holding or selling costs, depending on the asset and circumstances.

If the sale amount is higher than the cost base, you have a capital gain on that asset. If the sale amount is lower than the cost base, you have a capital loss.

Step 2: Add Up Gains and Losses for the Year

Once you have done this for each asset sold in the same financial year, you add all the gains together to get your total capital gains and all the losses together to get your total capital losses. If the total losses are higher than the total gains, you finish with a net capital loss that you carry forward to future years.

You cannot use a net capital loss to reduce normal business income, but you can use it to reduce capital gains in later income years.

Step 3: Apply Discounts and Concessions

If your total capital gains are higher than your capital losses, you then apply the CGT rules to arrive at your net capital gain. In simple terms, you first offset current and carried-forward capital losses against capital gains. After that, the order of any CGT discount and small business concessions depends on which concessions apply. For example, the small business 15-year exemption can eliminate the gain first, while other concessions are applied in a specific ATO order.

The remaining amount is your net capital gain, and this remaining amount is included in your assessable income for that income year. You pay CGT as part of your normal income tax, not as a stand-alone bill, so it feeds into the same tax return and affects the same final tax assessment.

Because the actual discounts and small business concessions vary depending on your structure, your turnover, the type of asset, and how long you have held it, this information requires professional verification.

Investment Property, Business Premises, and Your Family Home

Property often raises the biggest capital gains questions for electrical business owners because it involves large sums and long timeframes.If you sell your home and it qualifies as your main residence, the gain is often fully exempt. But if part of the home has been used to produce income, such as running a business from an area set aside as a place of business or renting part of it out, you may only get a partial exemption.

A workshop or commercial property that is only used by your electrical business is different again. Any profit you make when you sell this kind of property is usually treated as a capital gain and flows into your taxable income in that income year. This can be a big number, especially if the land value has grown and you have owned the property for many years. In these cases, small business CGT concessions and CGT discount rules can make a big difference if the asset is held by an eligible individual or trust and the conditions are met. Companies do not get the 50% CGT discount.

Because the rules around primary residence, investment property, mixed use, and active business assets are detailed and vary depending on your circumstances, you should not rely on a generic capital gains tax calculator alone. This information requires professional verification.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

Capital Losses, Carry Forward Rules, and Future Years

Not every sale delivers a profit, and capital losses can actually be useful in the long run if they are recorded properly. When you sell shares, property, or another eligible asset for less than the cost base, you create a capital loss. You cannot use a net capital loss to cut your tax on wages or business trading income in the year it happens, but you can carry forward that loss to offset capital gains in future years.

For example, if you have a poor past performance on an investment and realise a loss, and in a later year you sell your workshop or your business for a profit, that earlier loss can reduce the capital gain you pay CGT on. This can only happen if the loss has been reported and carried forward in your tax returns. For many electrical business owners planning to sell in a few years, reviewing old records for unused losses and implementing tax‑savvy strategies to boost profits is a simple way to make sure they are not leaving money on the table. Again, the best approach will vary depending on your full financial situation, so this information requires professional verification.

Why Clean Records and Support Make Capital Gains Simpler

Capital gains feel much harder when your records are incomplete, and the same is true when you are trying to maximise GST credits and stay ATO-compliant. Clean, accurate records mean you can calculate capital gains tax properly and make sure legitimate costs are included in the cost base rather than forgotten. For a busy electrical business, that usually means keeping copies of purchase contracts, settlement statements, and invoices for major assets, and ensuring that stamp duty, legal fees, and brokerage costs are recorded in your accounting software.

It also means keeping clear notes on how assets are used. If you use a property partly as a family home and partly as a business premises, or if a vehicle is used for both business and personal reasons, that mix needs to be recorded so the tax treatment can be worked out correctly later. Online tools, such as a capital gains tax calculator or guidance on the ATO website, can give you a rough idea, but they will not capture every detail of your accounts, income, expenses, and structure, or help you avoid common tax deduction mistakes.

Getting the Right Tax Advice Before You Sell

When you are planning a big move like selling shares in your company, selling a property, or stepping away from the business altogether, timing and planning matter. The Australian Taxation Office sets the rules, but it does not give advice that is tailored to your electrical business, your bank accounts, your home loan, and your long-term plans.

Speaking with a tax professional or financial advisor who understands trades businesses in the ACT helps you see the full picture before you sign a contract. They can help you check if you are treated as an Australian resident for tax purposes, confirm how your assessable income might change in the year you sell, and walk you through how capital gains will show up in your tax return. This is about making informed decisions, not just about ticking boxes, so you know roughly how much you might pay tax on and when that will happen.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)