Claiming the FBT Electric Vehicle Exemption: A Guide for Arborist Business Owners

Published on February 27, 2026

Claiming the FBT electric vehicle exemption is a practical way for arborist business owners to reduce fringe benefits tax while upgrading their vehicles. If you provide company cars to a current employee and allow private use, the electric car FBT exemption may allow the benefit to be exempt from FBT, provided the car meets strict eligibility rules.

For tree services businesses managing rising fuel costs, seasonal income changes, and increasing running costs, this exemption can create real tax savings. Understanding how the electric vehicle exemption works under FBT law helps you avoid errors and confidently plan your next vehicle purchase.

What Is the Electric Vehicle FBT Exemption and How Does It Work?

The electric vehicle FBT exemption is a fringe benefits tax exemption introduced by the federal government to encourage early adoption of zero or low emissions vehicles. It allows certain electric cars, including battery electric and hydrogen fuel cell electric vehicles, to be FBT exempt when provided by an employer to a current employee. Plug-in hybrid electric vehicles generally aren’t eligible from 1 April 2025, except in limited transitional cases.

To be eligible for the FBT exemption, the car must be first held and used on or after 1 July 2022, and LCT must never have been payable on the importation or retail sale of the car (including any subsequent retail sale) and be designed to carry fewer than nine passengers with a payload of less than one tonne. If these conditions are satisfied, the car benefit may be exempt from FBT. However, the exempt benefit is still generally reportable, so you may still need to calculate a notional taxable value for reporting.

Worried you’ll choose an EV that doesn’t actually qualify for the FBT exemption?

Schedule a complimentary consultation with us today to confirm EV eligibility, LCT limits and FBT treatment before you commit.

Why Is the Electric Car FBT Exemption Relevant for Arborist Businesses?

Arborists rely heavily on vehicles to transport equipment, access job sites, and visit clients. When those vehicles are also available for personal use, fringe benefits tax FBT normally applies, which increases overall cost.

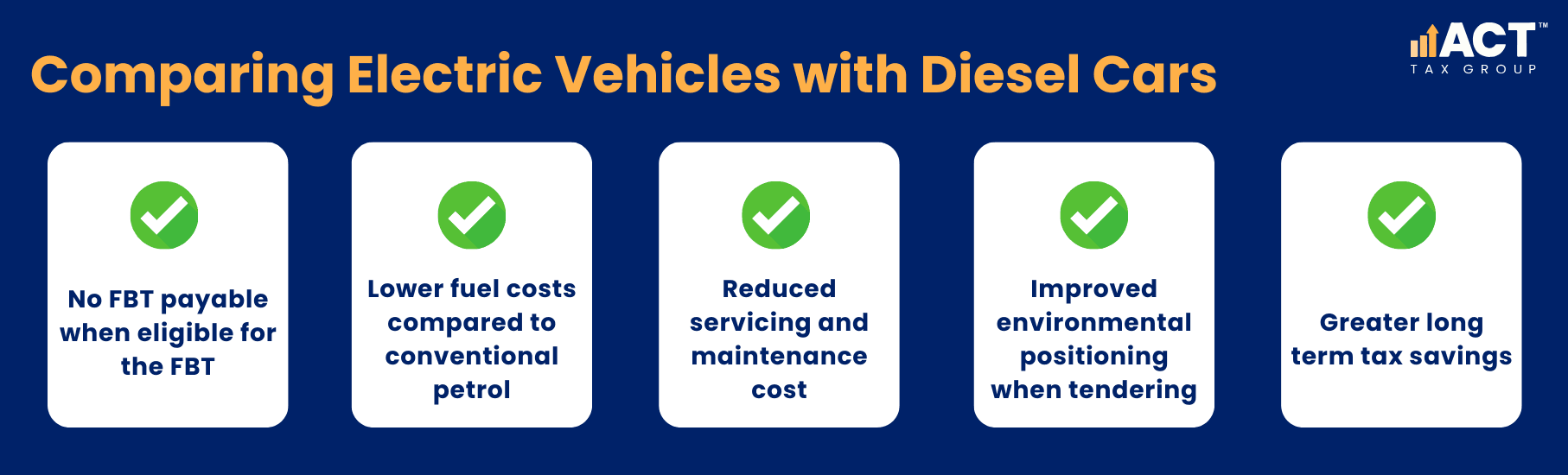

The EV FBT exemption makes electric vehicles an attractive option compared to conventional petrol or diesel cars. By removing FBT payable on eligible electric car benefits, you can lower tax exposure and improve cash flow during quieter months of the financial year.

How Does Fringe Benefits Tax Normally Apply to Company Cars?

Under standard FBT purposes, when an employer provides a car to a current employee and it is available for private use, the benefit is treated as a car fringe benefits arrangement. The employer must calculate the taxable value using either the statutory formula or operating cost method and then pay FBT at the applicable rate.

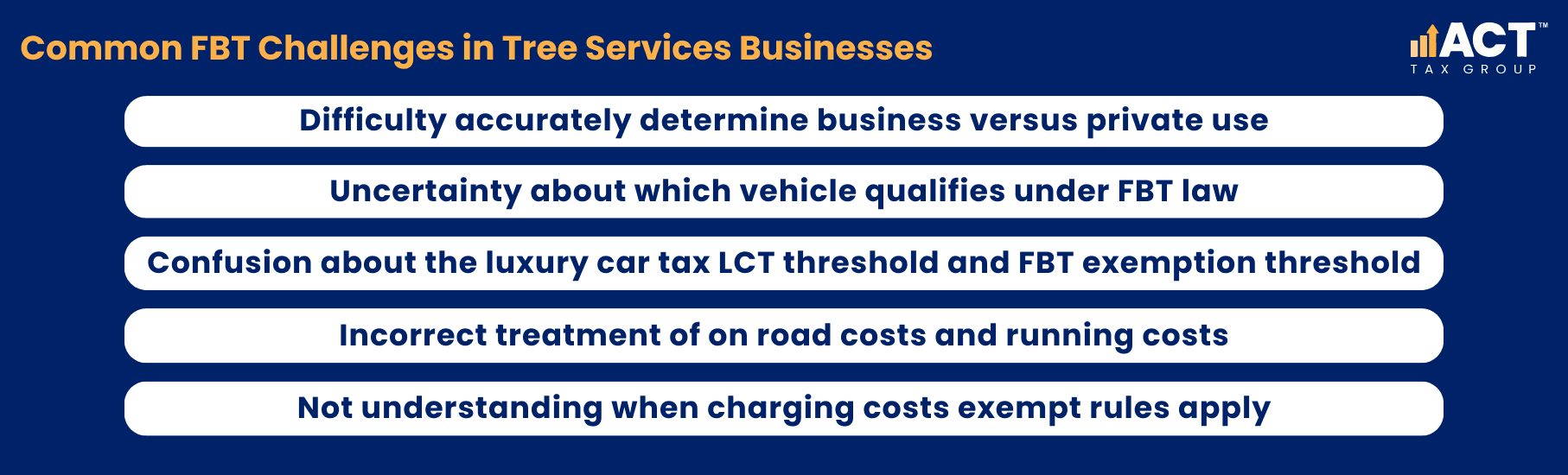

For many arborist business owners, this creates confusion around personal use, logbooks, and reporting obligations. If not managed correctly, you may pay FBT unnecessarily or understate the taxable value and face compliance issues.

These challenges can increase stress and make it harder to stay compliant throughout the FBT year (1 April to 31 March).

Which Electric Vehicles Are Eligible for the FBT Exemption?

Not all EVs are automatically eligible. To qualify as EVs eligible for the exemption, the vehicle must be an eligible electric car such as a battery electric vehicle or qualifying hybrid electric vehicles that meet legislative timing rules.

The car must be below the relevant LCT threshold at the time it is sold in a retail sale (and any subsequent retail sale), so that LCT has never been payable on the car. If the car exceeds the LCT threshold, it will not be eligible for the FBT exemption for electric vehicles and normal fringe benefits tax rules apply.

For arborists considering electric utilities, it is essential to confirm the payload capacity is less than one tonne and that the vehicle is classified as a car for FBT purposes.

How Do Charging Costs and Running Costs Work Under the Exemption?

Where the electric vehicle exemption applies, associated car fringe benefits such as charging costs may also be treated as charging costs exempt in certain circumstances. This can include electricity used at an employee’s home, using acceptable calculation methods such as the ATO EV home charging rate (a cents-per-kilometre method) where it applies.

Compared to conventional petrol or diesel cars, electric cars generally have lower fuel costs and maintenance running costs. When you combine these savings with the fringe benefits tax exemption, the total tax benefits can be significant over the life of the vehicle.

How Does a Novated Lease Fit into the Electric Car Exemption?

A novated lease can be used to structure the provision of electric vehicles to employees. Under a novated lease arrangement, the employer makes lease payments from the employee’s regular salary, and the car remains available for private use.

Where the car is an eligible electric car and meets all exemption conditions, the benefit may still be exempt from FBT. This can make salary packaging electric vehicles an attractive option for both employer and employee, particularly when compared to arrangements involving conventional petrol vehicles that would otherwise trigger FBT payable.

It is important to review the residual value, lease terms, and any optional extension at the end of the lease to ensure the arrangement remains compliant with FBT law.

What Happens If the Vehicle No Longer Meets the Exemption Rules?

If a vehicle is no longer exempt due to legislative changes or if it fails to meet eligibility criteria, standard fringe benefits tax FBT rules may apply from that point forward. For example, plug in hybrid electric vehicles may have different treatment depending on when a financially binding commitment was considered binding.

If the car exceeds the luxury car tax threshold at acquisition or was not first used within the required timeframe, it may not be eligible for the FBT exemption. In that case, you would need to calculate the taxable value and pay FBT in the relevant financial year.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

Plan Your Electric Vehicle Strategy with Confidence

The electric vehicle exemption can deliver meaningful tax savings, but only when eligibility rules are correctly applied. You must confirm the car is eligible, below the luxury car tax threshold, and meets all FBT purposes requirements before assuming it is FBT exempt.

We understand that arborist business owners already manage quoting pressures, seasonal cash flow, and equipment expenses. Our team helps you accurately determine eligibility, structure leases correctly, and ensure your fringe benefits tax exemption position is compliant and stress free.

If you are considering electric vehicles for your business, speak with us before entering into a financially binding commitment. We will review your structure, assess potential FBT payable, and help you make a confident decision that supports long term growth.

Making the FBT Electric Vehicle Exemption Work for Your Arborist Business

Electric vehicles are not simply an environmentally friendly choice. When eligible for the FBT exemption, they can reduce fringe benefits tax, lower fuel costs, and improve overall business efficiency.

By understanding the electric car FBT exemption, applying the correct FBT law, and planning before purchase or lease, you can turn compliance into a strategic advantage. With the right advice, the electric vehicle FBT exemption becomes a practical tool for reducing tax, strengthening cash flow, and supporting sustainable growth in your arborist business.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)