Should Your Arborist Business Operate Under a Discretionary Trading Trust? Key Tax and Payroll Implications

Published on February 17, 2026

Picture this: you are flat out finishing hazardous tree removals in June, your bank account is up and down, and your bookkeeper is chasing you about trust minutes, payroll, and unpaid super. You are wondering whether your current business structure is doing its job or whether a discretionary trading trust would better protect assets and simplify how you pay tax.

What a Discretionary Trading Trust Really Means for Arborists

For an arborist, a discretionary trading trust is simply a legal agreement where a trustee runs the business, holds trust assets, and decides how to distribute income to eligible beneficiaries. In legal terms, a trust is a relationship (not a separate legal entity); the trustee is the legal party that holds the assets and enters into contracts. However, trusts are treated as taxpayer entities for tax administration, and the trust deed sets the rules, including who the individual beneficiaries are and how income and capital can be shared. A family discretionary trust is a common version, where family members and sometimes a company are named as potential beneficiaries.

In many cases, business owners choose a trustee company as the legal owner of the trust property, with company directors in charge of decisions. This type of trust structure is often called a discretionary trading trust when it is used to run a business that generates income from day‑to‑day trade, such as tree removal, stump grinding, pruning, and related services. The trustee decides how to allocate income from the trust each financial year, instead of being locked into fixed entitlements. For many trusts, the decision needs to be made by 30 June (or earlier if the trust deed requires it) and recorded, or the trustee may be taxed on the trust’s income.

Struggling to keep payroll, PAYG and super correct under your trust?

Schedule a complimentary consultation with us today to clean up STP, PAYG withholding and super obligations.

Key Features of a Discretionary Trading Trust for Your Tree Services Business

When you look at the key features of a discretionary trading trust, you are really asking how it handles business assets, profit distribution, and tax advantages compared to other options. This includes how the trust’s bank account is used, who can receive trust income distributions, and how asset protection might work if something goes wrong on a job.

“First, business assets, such as chippers, trucks, and equipment, are typically held in the name of the trustee acting as trustee for the trust, not in your personal name. This can help protect personal assets like the family home if the business faces business risks or creditor claims, because the assets held in the trust are generally treated as trust property, not private property. Second, the trust income is pooled, and then the trustee can distribute trust income and capital gains to eligible beneficiaries, usually family members or related entities, in line with the discretionary trust deed. Third, the trust generally needs its own TFN, and it can have an ABN if it is carrying on an enterprise. The trustee registers for the trust’s TFN and ABN in its capacity as trustee.

How Tax and Income Distribution Work Under a Trading Trust

If you move your arborist business into a discretionary trading trust, the way you pay tax changes from being all in your own name to being split between beneficiaries. The trust lodges a tax return using its own tax file number, and the trustee reports how much trust income and any capital gains are allocated to each person or entity. Those beneficiaries are generally taxed on the amount they are entitled to as at 30 June, even if they receive the cash later.

Because a discretionary trust lets the trustee decide who receives income distributions, it can create potential benefits for tax planning in some family businesses. For example, the trustee might distribute income to adult family members who have lower income for that year, which may lead to some tax savings compared to having all profit taxed in one person’s hands. At the same time, the trustee can choose not to distribute income to someone in a higher tax bracket, if that suits their personal circumstances. This flexibility is often discussed as a tax advantage, but it must be managed carefully and in line with the trust deed and current rules. Rules can apply if one person is made entitled to trust income but another person benefits (Section 100A).

Asset Protection, Personal Risk, and Your Equipment

In a high‑risk trade like tree services, asset protection is usually one of the main reasons business owners look at a discretionary trading trust. Your crew is working at height, near power lines, or on storm‑damaged trees, which means business risks are always present even with good safety systems in place. You want to protect personal assets and family assets if something goes wrong and leads to a claim.

A common setup is to have a corporate trustee, often called a trustee company, as the legal owner of trust assets and business property. In that case, the company is the legal owner of the business assets used to generate income, while you and any other company directors hold control over decisions. The idea is that if the business faces financial loss or a lawsuit, only profits and assets held in the trust are exposed, not your personal home or other personal assets, as long as everything has been set up and operated correctly. This can support financial security and your financial future, especially if you want to protect assets for future generations.

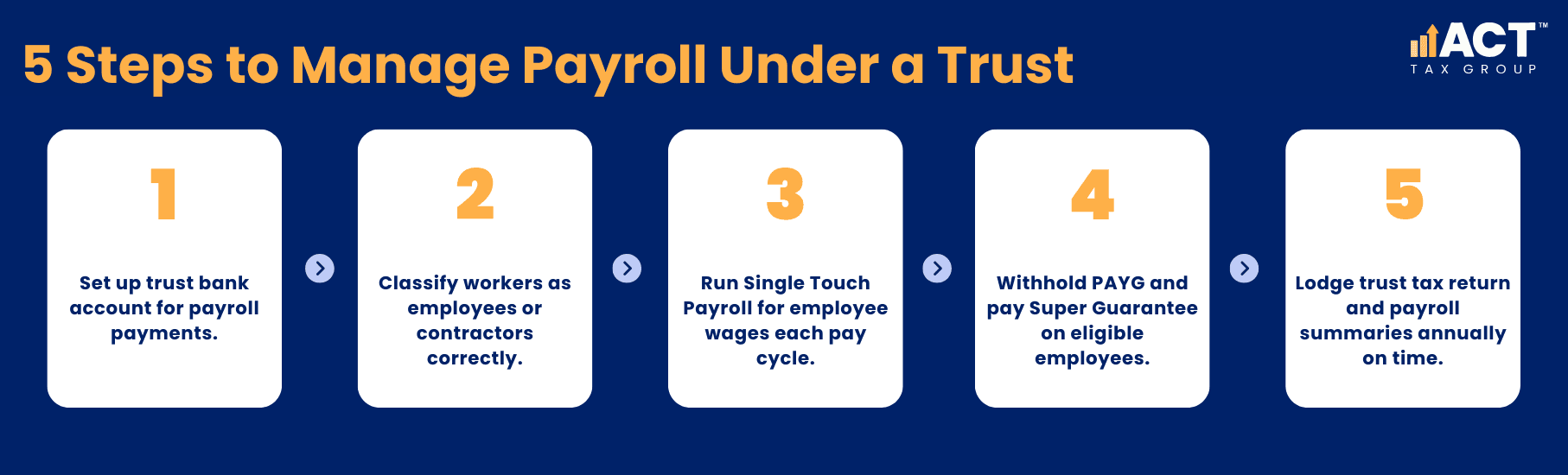

Payroll, Workers, and Day‑To‑Day Compliance Under a Trust

Switching to a discretionary trading trust does not remove your duty to pay your people correctly. Since 1 January 2024, most employees can also take court action under the Fair Work Act for unpaid super, so late super can create extra risk. The trustee (as trustee for the trust) is the employer and still needs to pay wages, withhold tax, report through Single Touch Payroll, and pay super. The super guarantee rate is 12% for eligible wages paid on and after 1 July 2025, and from 1 July 2026 super generally needs to be paid at the same time as wages (Payday Super). The name on the legal agreement may change, but the practical work stays the same.

If your trust hires climbers, ground crew, and admin staff, it will need its own bank account for payroll and a clean system to track who is on wages and who is a contractor. Employees are set up through payroll, with PAYG withholding and super, while contractors are paid on invoice if they are genuinely in business for themselves. You still need to make sure you classify workers correctly and pay super where required.

For super, you may need to pay a contractor if the contract is mainly for their labour, and an ABN does not change that. The trust must lodge the right forms each financial year, including its trust tax return, and it must meet its employer reporting duties. If you report through Single Touch Payroll, you usually do an end‑of‑year finalisation and employees receive an income statement rather than a payment summary.

Cash Flow, BAS, and Keeping the Trust Books Clean

Seasonal work makes cash flow management tough for many arborist businesses, and a discretionary trading trust does not magically fix that. It does, however, make it more important to keep the trust’s bank account and records tidy so income and expenses are easy to track across the financial year. This is because your profit distribution and trust income distributions depend on accurate numbers.

All business income from jobs should go into the trust’s bank account, and all business costs fuel, repairs, wages, insurance should be paid from that same account. That way, at year end you can see clearly what the business structure has actually earned. When it is time to implement the distribution, the trustee can pay funds to beneficiaries in line with the decision. If a private company is a beneficiary and the amount is left unpaid, extra tax rules can apply (including Division 7A). Keeping this separation makes it easier to complete BAS, track tax obligations, and make sure you only pay tax on the income that belongs to each person or entity. It also makes it easier to show a lender or potential buyer how strong your business interests are if you are looking at business growth or new equipment finance.

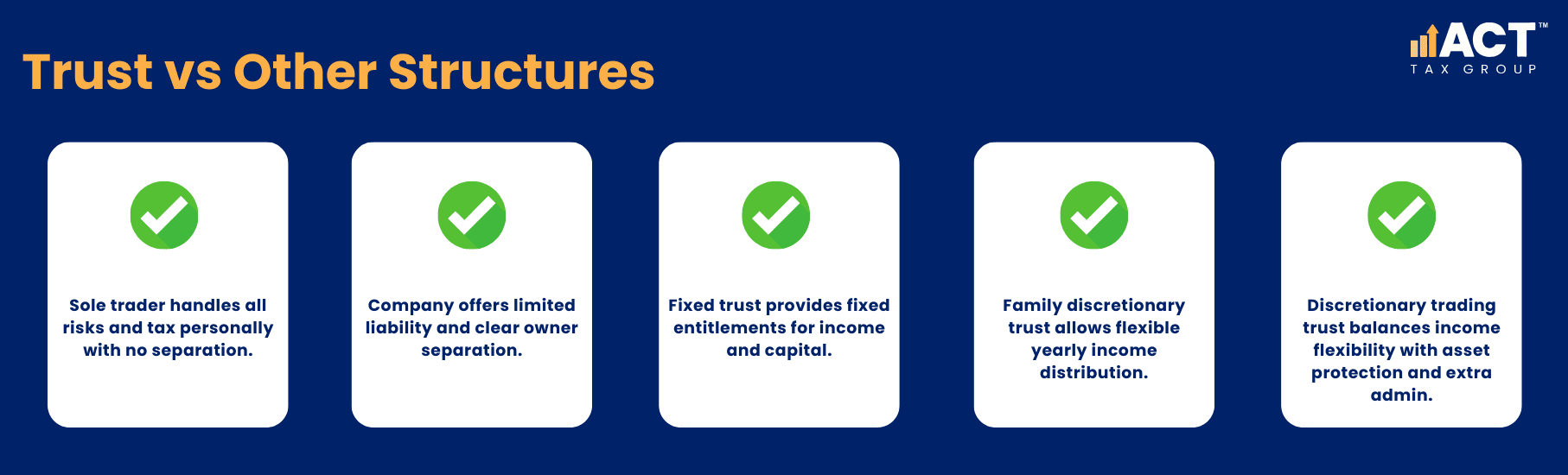

How Discretionary Trusts Compare to Other Options

You might hear other business owners talk about running everything directly as a sole trader, using a company with limited liability, or setting up a fixed trust where beneficiaries have fixed entitlements. Each option handles business risks, income tax, and asset protection differently, and the right choice depends on your personal circumstances.

A company is often preferred for limited liability and clear separation between owners and the legal entity. A fixed trust may be used where investors or family members need fixed interest and clear rights to income and capital. A family trust or family discretionary trust is often used for family businesses where the trustee can distribute trust income each year based on who needs it. A discretionary trading trust structure sits somewhere in the middle, combining flexibility to distribute income with some protection for assets held in the trust, but with more administration and rules to follow. This is why many advisors say to seek advice before changing structures, rather than setting up a trust just because another arborist or someone in the construction industry has one.

Testamentary Trusts, Estates, and Long‑Term Planning

You may also hear terms like testamentary trust or testamentary discretionary trust when thinking about what happens to business assets when you are no longer around. These are trusts created under a will, often used to hold family assets and business interests for children and future generations after a deceased estate is finalised. They are separate from your day‑to‑day discretionary trading trust, but they can sit alongside it as part of your longer‑term planning.

In this context, potential benefits include better control over distributing assets and income to younger family members, some protection from creditor claims or financial loss in their own lives, and the ability to manage tax on income and capital in a flexible way. These arrangements can be complex, and they usually need careful drafting so that the formal trust deed, business structure, and will all work together. Again, this is a space where you should seek professional advice instead of trying to piece together something from templates.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

Why You Should Seek Professional Advice Before Setting Up A Trust

Trusts bring more moving parts than running your business in your own name. You need to get the trust deed right, register the trust for a tax file number and Australian Business Number (ABN), set up the right bank account, and make sure the trustee company or individual trustee understands their responsibilities. On top of that, the trustee must keep records of profit distribution decisions, make sure income distribution is made correctly, and pay tax where income is not properly allocated.

Because every family trust, business structure, and set of personal circumstances is different, the safest path is to seek advice from a qualified professional who works with family businesses and trade‑based clients. They can help you weigh up the potential benefits, such as asset protection and flexible income distribution, against the extra costs and responsibilities, like more detailed bookkeeping and tighter deadlines each financial year. Getting this right at the start is far easier than trying to repair a structure that was rushed or set up without proper guidance.

How ACT Tax Group Can Help Your Arborist Business

If you run an arborist business in the ACT or nearby, you want a team that understands chainsaws, seasonal cash flow, and real‑world business risks not just theory. Whether you already have a discretionary trading trust or you are thinking of setting one up, we can help you see clearly what it means for your tax obligations, payroll, and long‑term financial future.

ACT Tax Group works with tree services business owners to set up clean systems around bookkeeping, payroll, BAS, and trust reporting, so your trust structure actually supports your business growth instead of adding confusion. We take the time to explain how your trust deed, trustee company, and bank accounts fit together, how to distribute trust income correctly, and what records you need to keep so you can pay tax with confidence each year.

If you would like a practical, no‑nonsense review of your current setup or you are considering a discretionary trading trust for the first time, we encourage you to seek professional advice and book a consult with ACT Tax Group. This article is general in nature, for illustration only and does not constitute financial or personal advice. For support tailored to your situation, please seek professional advice from ACT Tax Group or your own qualified advisor.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)