Unlocking the Electric Vehicle FBT Exemption: What It Means for Electrical Businesses

Published on February 10, 2026

Unlocking The Electric Vehicle FBT Exemption: What It Means for Electrical Businesses is great news if you want decent cars for your team without a big Fringe Benefits Tax bill hanging over every vehicle decision.

You might be looking at Electric Vehicles for your next ute or van and wondering if the numbers really stack up once tax, price and running costs are all counted. As an employer, you do not want to pay FBT on a benefit you do not fully understand, and you definitely do not want surprises at the end of the FBT year. In this updated version, we will walk through how the Electric Vehicle FBT Exemption works, where the Luxury Car Tax threshold fits in, and what all this means in real terms for your crews, your cash flow and your own car.

Why Electric Vehicle FBT Exemption Matters for Electricians

If you provide a car that your current employee can also use to drive home, take the kids to sport or head away on weekends, that is usually a car fringe benefit and can trigger Fringe Benefits Tax. For electrical businesses with several vehicles on the road, this can quickly add up, especially when cash flow is already tight.

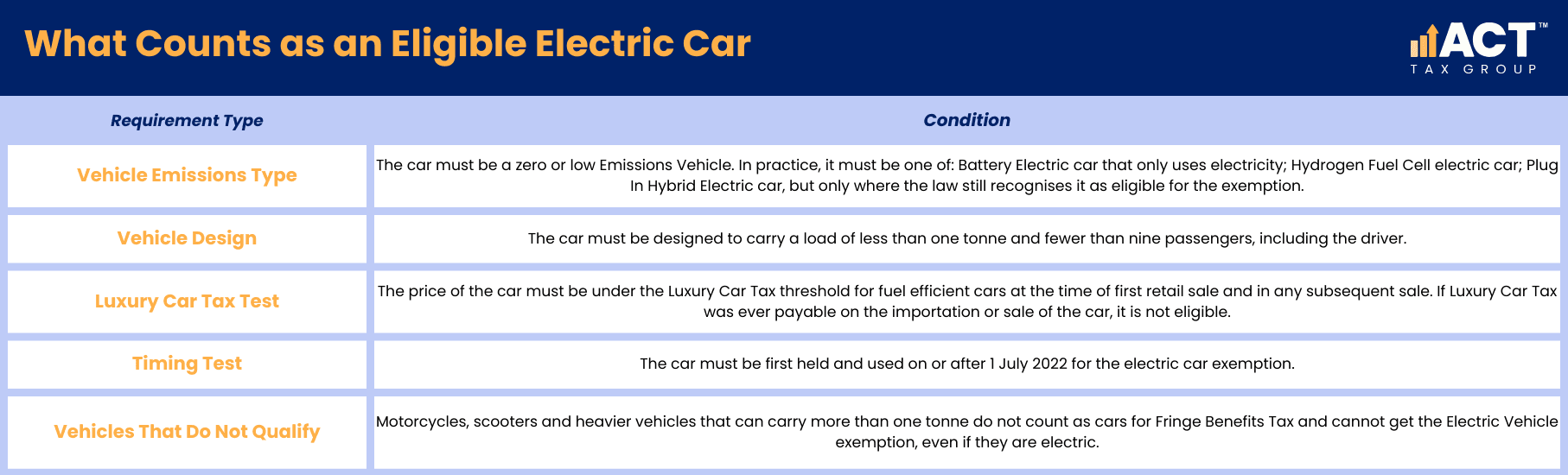

The Electric Vehicle FBT Exemption lets certain eligible electric cars be exempt from FBT, even when there is private use. In simple terms, if the car ticks the zero or low emissions boxes, was first held and used on or after 1 July 2022, is provided to a current employee or their associates, and stays under the fuel-efficient vehicles Luxury Car Tax threshold, you may not have to pay FBT on that benefit. You still work out a taxable value for the car fringe benefits, but that value is used only for reportable fringe benefits, not to calculate FBT payable.

Worried your next EV ute might still trigger FBT?

Schedule a complimentary consultation with us today to check EV eligibility and avoid surprise ATO bills.

The Key Rules Electrical Businesses Need to Understand

When you are looking at Electric Cars for your team, you need to know exactly when the exemption applies so you do not accidentally buy a vehicle that is not eligible. These rules are set at a federal government level and apply across Australia.

Why The Luxury Car Tax Threshold Matters

For both the 2024–25 and 2025–26 financial years, the Luxury Car Tax threshold for fuel efficient vehicles is $91,387. The Luxury Car Tax threshold is a cap on the value of fuel-efficient cars before Luxury Car Tax is triggered. To be FBT exempt, eligible Electric Vehicles must stay under the fuel efficient LCT threshold at the first retail sale. If Luxury Car Tax was ever payable on that car, it will not qualify for the Fringe Benefits Tax exemption.

This is where many electrical businesses get caught. A vehicle might feel like a work car, but if the price is above the fuel efficient LCT threshold, it is not eligible for the FBT exemption, and any private use can still mean you have to pay FBT. Always double check the LCT threshold for the relevant financial year before you commit.

From 1 July 2025, the definition of a fuel efficient vehicle for Luxury Car Tax purposes also changed. The maximum fuel consumption rate was reduced from 7 litres per 100 kilometres to 3.5 litres per 100 kilometres. Battery Electric Vehicles are not affected by this change, but some Plug In Hybrid Electric Vehicles with fuel consumption between 3.5 and 7 litres per 100 kilometres may be impacted.

Plug In Hybrid Electric Vehicles and the 1 April 2025 Change

If you are considering Plug in Hybrid Electric vehicles, the date 1 April 2025 is important. Plug In Hybrid vehicles are treated differently after this date, and some arrangements will no longer be exempt from FBT.

In most cases, this means new Plug-In Hybrid Electric cars provided to employees after 1 April 2025 will not be eligible for the Electric Vehicle FBT Exemption. Some older Plug-In Hybrid arrangements can stay exempt if the use of the vehicle was exempt before 1 April 2025 and the employer has a financially binding commitment to continue providing private use of the vehicle on and after 1 April 2025. Optional extensions of the agreement are not considered binding. If you already have a Plug in Hybrid vehicle or are thinking of one, you need to look closely at your lease, the term and the residual value, and get professional guidance on whether it is still FBT exempt or will be subject to FBT going forward.

How The EV FBT Exemption Helps Your Cash Flow

For most electrical contractors, the real question is simple: does this exemption save us money and reduce stress, or is it just another layer of rules? When used properly, the EV FBT Exemption can improve cash flow and make it easier to justify Electric Vehicles in your fleet.

Less FBT Payable on Eligible Electric Cars

Under normal rules, if you provide a car fringe benefit, you need to work out the taxable value and may have FBT payable at the end of the FBT year. With an eligible Electric Vehicle, that car benefit can be exempt from FBT, which means no FBT payable on that benefit even though your employee has private use.

This can have a big impact if you are running several cars, because you are not setting aside a large total amount each year for Fringe Benefits Tax. Instead of worrying about how much tax you will pay on each vehicle, you can focus on price, running costs, load capacity, and how the car helps your teams get to jobs on time.

Novated Lease, Salary Packaging And Reportable Benefits

Many directors and key staff access Electric Vehicles through a novated lease. Under a novated lease, the employee agrees that part of their pay will be used to cover lease payments and running costs, and the employer takes on the lease and provides the car. With an EV FBT Exemption, the benefits from an eligible electric vehicle on a novated lease can be exempt from FBT, which makes salary packaging more attractive and often improves the after-tax outcome compared to a standard car.

However, you still need to work out the notional taxable value of the car benefit. If the total taxable value of reportable fringe benefits provided to the employee during the FBT year exceeds $2,000, you must report the grossed-up amount on the employee’s income statement. That amount does not create extra income tax for the employee, but it can affect things like Medicare levy surcharge, family benefits and other income-based tests. So, while the employer may not pay FBT, you still need to think about personal circumstances when you design these car packages.

Associated car expenses such as registration, insurance, repairs, maintenance and charging costs that are exempt under the Electric Vehicle FBT Exemption are not included when working out the employee’s reportable fringe benefits amount. Only the car benefit itself is included in the calculation.

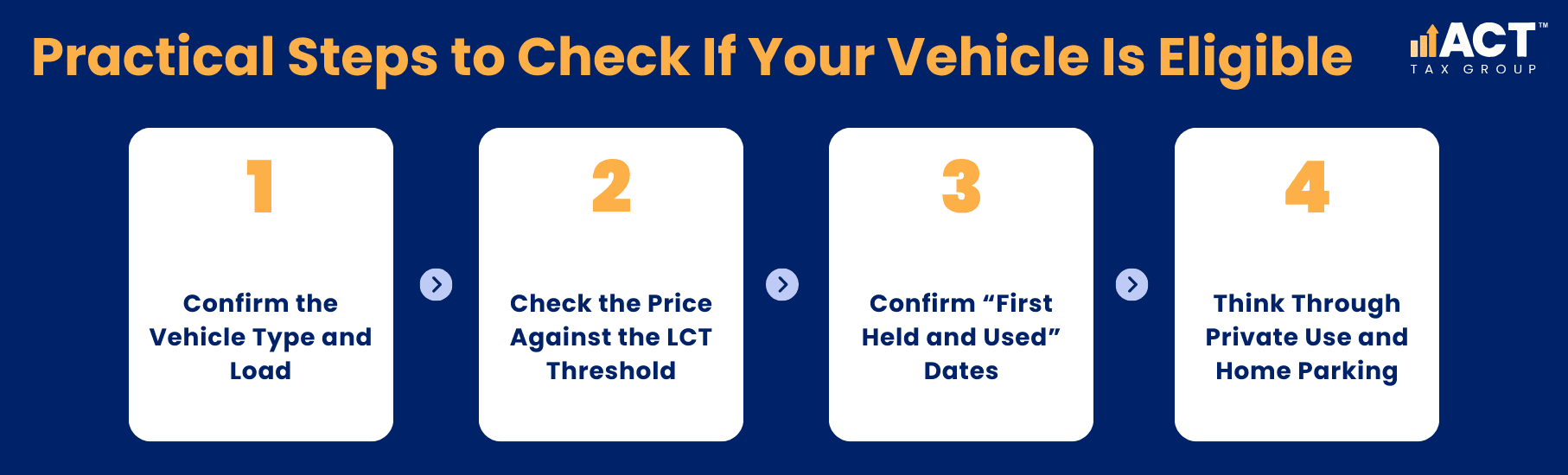

Practical Steps to Check If Your Vehicle Is Eligible

If you want to use the Electric Vehicle exemption without getting lost in the detail, it helps to run through a simple checklist before you purchase or sign any lease.

Step 1: Confirm The Vehicle Type and Load

Start by confirming that the vehicle is actually a car for Fringe Benefits Tax. It must be designed to carry less than one tonne and fewer than nine passengers. If you are looking at a van or ute that can carry more than that load, different rules apply, and the Electric Vehicle FBT Exemption may not be available.

Once you know it is a car, check that it is a Battery Electric, Hydrogen Fuel Cell or eligible Plug In Hybrid Electric vehicle. Regular hybrid vehicles that mainly use petrol and only use electricity to assist are not treated as zero or low Emissions Vehicles for this exemption.

Step 2: Check The Price Against the LCT Threshold

Next, look at the total price of the car at first retail sale, including delivery and accessories, and compare it to the LCT threshold for fuel efficient vehicles for that financial year. If the price is above the LCT threshold and Luxury Car Tax would have been payable at first sale, it will not be eligible for the Electric Vehicle exemption, even if you are buying it second hand.

Dealers should be able to confirm whether the car was ever subject to Luxury Car Tax. If there is any doubt, ask for documentation or walk away, because this one detail can make the difference between being exempt from FBT or having to pay FBT every year on that benefit.

Step 3: Confirm “First Held and Used” Dates

The rules also look at when the car was first held and first used. To qualify, the first time it was both held and used needs to be on or after 1 July 2022. If you are buying second hand, you need to check the history, not just when you get the keys.

For example, if the first owner bought the car and started using it before the qualifying date, then the car will not be eligible for the exemption for later owners. If they bought it before the date but did not use it until after, and both events line up correctly, it can be eligible. It is a small detail, but it decides whether the car is fbt exempt or not.

Step 4: Think Through Private Use and Home Parking

Remember that Electric Vehicle FBT Exemption is about private use of the car. If the car goes home with the employee each night, sits at the employee’s home on weekends, or is used by family members, all of that counts as private use and is normally a fringe benefit. The exemption simply means that for eligible electric cars, this benefit is exempt from FBT.

You should still keep clear records of who has which car, how it is used and what the running costs look like. This helps you support the taxable value calculations for reportable fringe benefits and keeps your accountant happy at Fringe Benefits Tax time.

What Counts as Exempt Running Costs and Charging Costs

The Electric Vehicle exemption does not only cover the car itself. Certain associated car expenses can also be exempt from FBT when they relate to an eligible EV.

Registration, insurance, repairs, maintenance and many running costs linked to an exempt Electric Vehicle can also be exempt from FBT. Charging costs exempt from FBT can include the cost of electricity to charge eligible EVs, provided they are clearly linked to that car. However, providing an employee with a home charging station is a separate fringe benefit and is not exempt under the Electric Vehicle FBT Exemption. This is useful when you are tracking EV car expenses across multiple vehicles and want to know which costs are fully exempt and which are not.

It is still important to keep clear records of total kilometres travelled and your spending on each vehicle, so you can support your calculations if the ATO asks questions later. The ATO provides a shortcut method of 4.20 cents per kilometre to estimate home charging costs for Battery Electric Vehicles. Even when items are exempt, clear records help you support your position if the ATO asks questions later.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

Bringing It All Together for Your Business

Electric Vehicles and the Electric Vehicle FBT Exemption can be powerful tools for electrical businesses, but only if you match them carefully to your real-world needs. When you get it right, you can provide good cars for your team, keep Fringe Benefits Tax under control, manage running costs and keep your books clean.

The federal government is required to complete a review of the Electric Vehicle FBT Exemption by mid-2027 to assess electric car take-up. This means the exemption is not guaranteed to continue in its current form beyond that point, and businesses entering into longer lease arrangements should factor this into their planning.

At ACT Tax Group, we help you work through the details: which cars are likely to be eligible for the FBT exemption, how the Luxury Car Tax (LCT) threshold affects your options, and what novated lease or other arrangements make sense for your situation. We always bring it back to your numbers, your people, and the way your crews actually use their vehicles day to day.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)