How the Corporate Tax Rate Impacts Small Arborist Businesses in Australia

Published on February 3, 2026

How the corporate tax rate impacts small arborist businesses in Australia shows up every time you look at your profit and wonder how much tax will be left to pay after a big season. When your work swings between busy storm periods and quiet winter months, knowing how company tax works can make a real difference to your cash flow, gear upgrades and your own pay packet.

When Tax Bills Sneak Up on Arborist Businesses

Picture this: you have a strong year of trading income from tree removals, stump grinding and emergency jobs, your books show healthy gross income, and then your accountant tells you the company pays a big tax bill. You’re left thinking, “Where did that money go?” This is where understanding taxable income, assessable income and the company tax rate becomes practical, not just technical.

For a small arborist company, your income tax bill is worked out each financial year on your total assessable income. That includes business income from Australian operations, interest income on your business account and any rental income sitting inside the same company. From this, you subtract allowed company tax deductions, such as gear, fuel, insurance and professional fees, to arrive at taxable income. Company tax is then calculated on that number using the tax rates for that income year.

Unsure if your arborist company qualifies for the lower 25% tax rate?

Schedule a complimentary consultation with us today to check your base rate entity status and avoid paying more tax than needed.

Base Rate Entity: Getting the Lower Company Tax Rate

For small arborist businesses, the big line in the sand is whether you qualify for the lower company tax rate or fall under the full company tax rate used for larger businesses or high passive income companies. This is set through the base rate entity test.

In simple terms, to be a base rate entity for the 2025–26 income year and future years, a company must usually meet both of these key points:

Its aggregated turnover is less than the aggregated turnover threshold (currently $50 million, which most small arborist companies are well under).

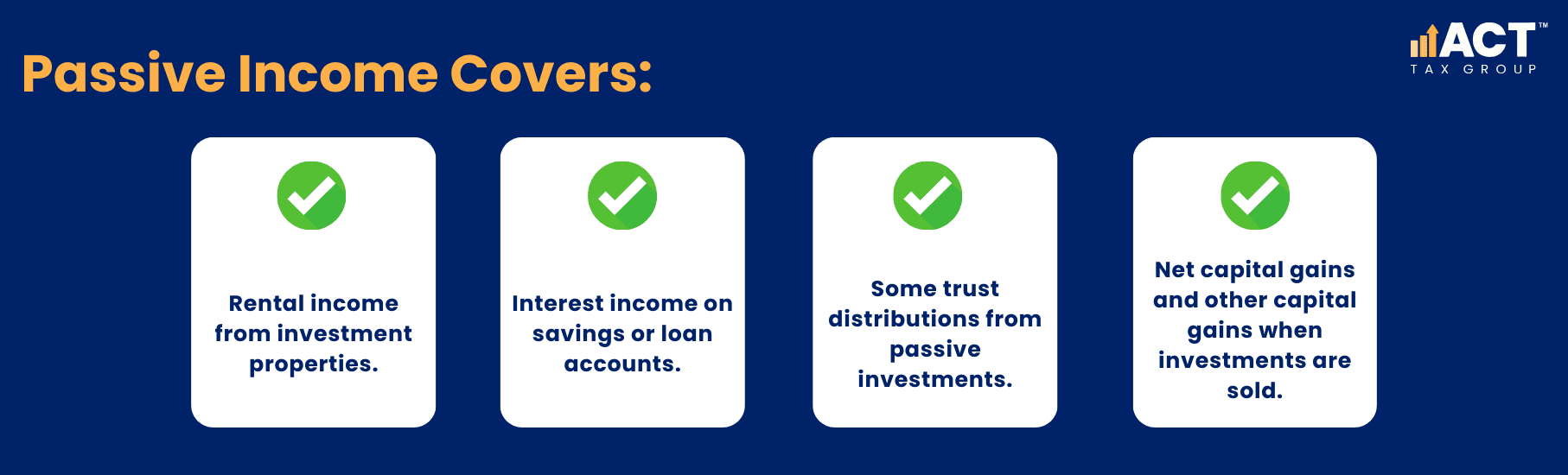

No more than 80% of its assessable income is base rate entity passive income such as interest income, rental income, some trust distributions, franking credits on some corporate distributions and net capital gains.

If your company passes this base rate entity test, you get the lower tax rate on your taxable income for that entire year. If you fail, you are stuck on the higher, standard company tax rate. The rules are determined annually based on your actual company’s aggregated turnover and mix of income in that specific income year, not what happened years ago.

Trading Income vs Passive Income for Arborist Crews

Most arborist owners are focused on business income from everyday jobs: cutting trees, clearing blocks and handling storm damage. This trading income is counted as active business income and helps you qualify for the lower rate, because it is not base rate entity passive income.

This is why many property investment companies do not qualify for the lower rate – their rental income counts as passive income and often pushes them over the passive income test limit. For a small arborist company, the risk appears when you hold investment properties or large passive assets inside the same company as your tree business, or when you have multiple entities and high passive income across the group.

The passive income test compares total base rate entity passive income against total assessable income. If more than 80% of your total assessable income is passive, you fail the test and lose access to the lower rate. That’s a big shift in how much tax you pay, especially after a strong year.

Aggregated Turnover, Multiple Entities and Your Group

Aggregated turnover is another term that trips up many business owners. It isn’t just about the sales from your main arborist company. It looks at the annual turnover of the company plus connected entities and sometimes affiliates.

If you run your tree business through one company, own a separate company for investment properties, and maybe receive trust distributions through another structure, the numbers may all feed into your aggregated turnover. Multiple entities can push you closer to the aggregated turnover threshold even if a single company looks small on its own.

For a typical arborist business with annual turnover between a few hundred thousand and a couple of million, you’re usually well under the threshold. But if your group grows, or you start adding extra companies, it is worth checking whether your aggregated turnover has changed your tax position. The base rate entity rules apply to Australian companies each year, and your eligibility requirements are checked again every income year, not just when you first set up.

How Different Tax Rates Change Your Cash Flow

Once you know whether you qualify for the lower rate or the full rate, the next question is practical: how much tax, and what does that mean for your plans? Different tax rates can change how much you have left to reinvest, save, or take out of the business.

If your base rate entity status means you get the lower tax rate, more after-tax profit stays in the company. That can fund new gear, safety training or a buffer for slow periods. If you are on the full rate, a larger slice of your profit goes to tax, and your planning needs to account for that.

Remember, company tax is only one layer. When you eventually pay dividends, those come with franking credits that reflect the tax already paid by the company. Franking credits work to stop you being taxed twice on the same company income. The franking rates you can use are linked to your previous year’s tax status and which corporate tax rate applied in that previous income year. This means your choice of structure and your company’s earlier results can affect how future dividends are taxed in your hands.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

Using Deductions and Write-Offs without Overcomplicating Things

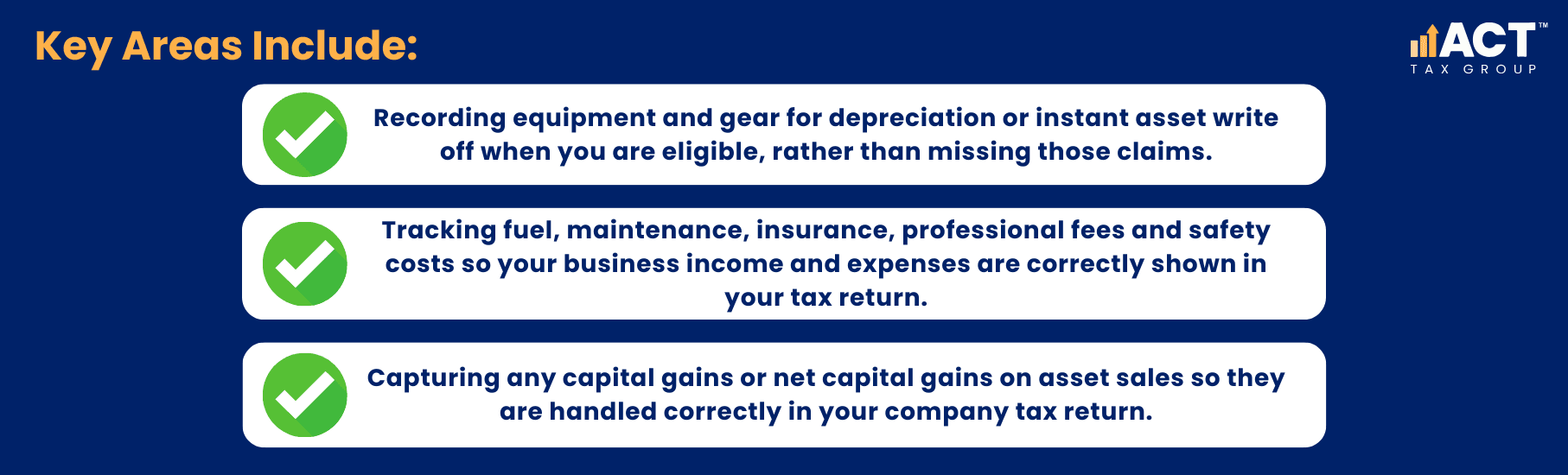

There’s a big difference between trying to avoid tax and simply using standard company tax deductions and concessions properly. For arborist companies, straightforward record-keeping can make a big difference to taxable income while staying inside the rules.

For the 2025–26 income year, instant asset write off rules and thresholds can shift, often based on your aggregated annual turnover and whether you use simplified depreciation. You still need to check whether your company is an eligible business before relying on these concessions. This is where getting help from someone who understands both the rules and your day-to-day work becomes important.

International Rules, Foreign Shareholders and Most Arborists

You might see terms like income inclusion rule, undertaxed profits rule or worldwide income and wonder if they apply to you. These rules are mostly aimed at larger, international groups and foreign shareholders, rather than small arborist companies operating locally.

For most small Australian companies in tree services, company tax is primarily based on Australian operations and Australian business income. If you do have foreign shareholders, or income from outside Australia, your tax position can be more complex, and you will need advice on withholding tax rates, trust distributions and how worldwide income is reported. But for many small crews, the focus stays on daily jobs, cash flow and paying the correct amount of tax on local work.

Why Working with a Registered Tax Agent Helps

Trying to juggle chainsaws, staff and complex tax rules is too much for one person. A registered tax agent who understands arborist businesses can step in and make this manageable without drowning you in theory.

They can help you:

Check whether your company qualifies as a base rate entity each year, using your company’s aggregated turnover and passive income.

Review your previous year’s tax status so you know which franking rates and corporate tax rate apply for the current year.

Work out how much tax you’ll likely pay by using your instalment income and gross income during the year, rather than leaving it all to the end.

Lodge your company tax returns correctly so you stay compliant, protect your base rate entity position and avoid surprises.

Most importantly, they can translate the rules into clear actions: how much to set aside each quarter, when to consider buying equipment, how to time your professional fees and other expenses, and how to keep your records tidy. You stay focused on safe jobs and good service, while they focus on keeping your tax position clean and ATO-ready.

Bringing It Back to your Arborist Business

At the end of the day, the way the corporate tax rate impacts small arborist businesses in Australia comes down to three simple questions: what income you earn, how that income is split between trading and passive, and whether you pass the base rate entity tests each year. Once you see those pieces clearly, you can plan instead of reacting.

You don’t have to become a tax expert. You just need enough understanding to ask the right questions: Are we on the lower rate or full rate? How does our aggregated turnover look? Do we have high passive income or mostly trading income? Are we setting aside enough through the year to pay tax without stress?

If you want help turning those questions into a clear plan for your arborist company, talk to a professional who understands tree services, seasonal work and the reality of running a crew.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)