Corporate Tax Rates Explained: What Electrician Companies Need to Know for 2026 and Beyond

Published on January 20, 2026

Corporate Tax Rates Explained: What Electrician Companies Need to Know For 2026 and Beyond is not just a technical topic – it is a core part of how much tax your company pays on the profit you work so hard to earn. When the wrong company tax rate is used in planning, you can feel slammed with jobs but still short on cash once the Australian Taxation Office processes your company tax returns and issues the final bill.

When A Busy Electrical Company Gets a Tax Shock

Picture this. You run an electrical company with steady business income from residential jobs, light commercial work and a mix of government grants and maintenance contracts. All year you assumed your company was on the lower company tax rate, only to find at tax time that the full company tax rate actually applies because of how your company’s taxable income and company’s aggregated turnover are treated for that income year.

Worried your electrical company is on the wrong tax rate?

Schedule a complimentary consultation with us today to confirm your correct ATO corporate tax rate and avoid bill shock.

The Two Company Tax Rates Electricians Face

If your electrical business is run through a Pty Ltd company, you are dealing with corporate tax, often called corporate income tax or simply company tax. In practical terms there are two main tax rates that apply to Australian companies: a lower company tax rate for eligible companies, and a full company tax rate for everyone else.

For electrician companies that qualify as a base rate entity, the company pays the lower company tax rate on the company’s taxable income from trading income and other assessable income. For companies that do not meet the base rate entity test, the full company tax rate applies to the company’s taxable income for that income year. The key point is that tax laws do not lock you into one rate forever – the tax rate can change with your business, your annual turnover and your mix of corporate income year by year.

How Company Tax Connects to Your Day-To-Day Numbers

From your point of view as an electrical contractor, the company tax rate is the percentage applied to your company’s taxable income after allowable deductions like tools, vehicles, professional fees, and other company tax deductions. The company’s assessable income usually includes gross income from business income, interest income, some government grants, and sometimes rental income counts if held in the same company.

The difference between gross income and taxable income is driven by allowable deductions such as instant asset write off (when rules apply), capital allowances on bigger equipment, and other business expenses you can immediately deduct or claim over time. Getting this wrong does not just affect the tax return at year‑end – it flows through to your tax position during the year, your instalment income for PAYG, and how confident you feel when quoting jobs.

What is a Base Rate Entity for an Electrical Company?

The base rate entity rules decide whether your company qualifies for the lower company tax rate or the full company tax rate. Even though they sound technical, they boil down to two big questions: what is your company’s aggregated turnover, and how much of your company’s assessable income is high passive income rather than trading income.

Aggregated Turnover and Business Size

The base rate entity test looks at aggregated turnover rather than just sales in your Xero file. Aggregated turnover is your annual turnover plus the annual turnover of any business entities that are your affiliates or are connected with you, including both Australian and overseas operations where relevant. For many electrician companies this still stays well below the aggregated turnover threshold used for the lower company tax rate, but it is important to check if you run multiple companies, a service company plus a trading company, or have related entities.

Annual turnover is measured separately for each income year. For base rate entity status, only your current‑year aggregated turnover and passive income are used – aggregated turnover from prior years is not taken into account for this test. Previous‑year figures can still matter for other purposes, such as some small business concessions and franking rules, which is why your accountant will look at both current and prior years when planning.

Passive Income Test and High Passive Income

The second part is the passive income test. While your main business income is trading income from electrical work, many property investment companies and some electrical businesses also hold investment properties, shares, or term deposits inside the same company. In those cases, interest income, rental income, and some other returns are treated as passive income.

If a company has high passive income compared to its total assessable income – for example, where rental income from investment properties or interest income is a large part of the company’s assessable income – the company may fail the base rate entity passive income test and end up on the full company tax rate. This is why many business owners separate business income from investment properties or other passive income, so that passive income does not dominate total assessable income in their trading company.

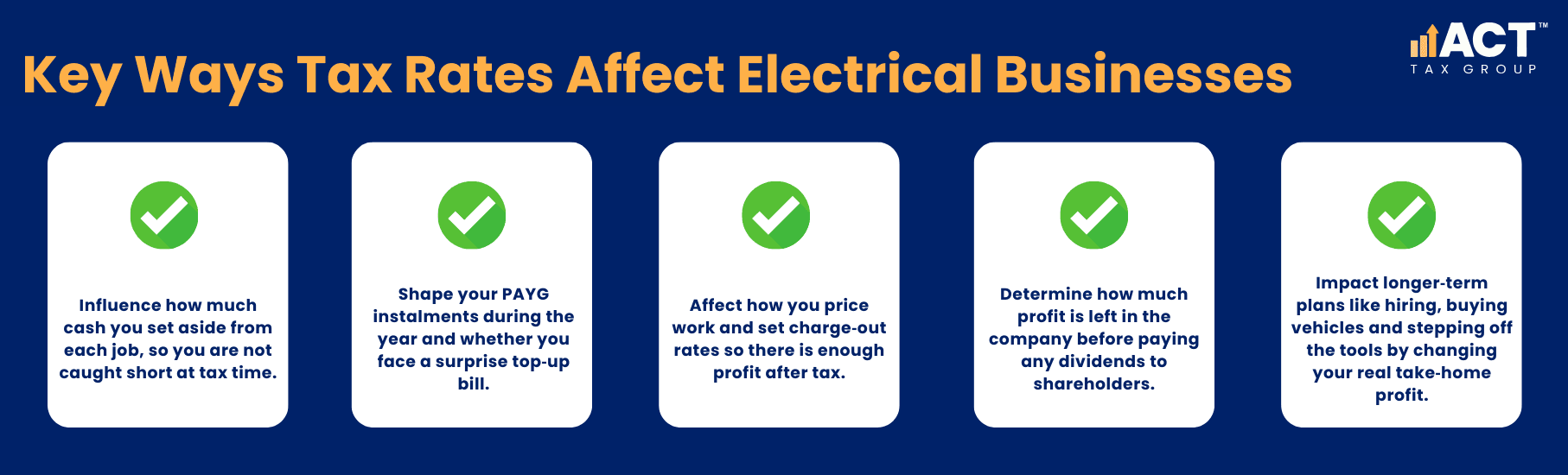

Why Corporate Tax Rates Matter to Electrical Contractors

You might be thinking that your registered tax agent can sort the tax return and company tax at the end of the year, so why worry now? In reality, corporate income tax ties directly into how much tax you set aside from each job, how you plan for tools and vehicles, and how you make decisions about growth.

Cash Flow, PAYG And “How Much Tax” You Really Pay

During the year, many Australian companies pay tax through instalments based on instalment income and previous year assessments. If your PAYG instalments are based on the lower company tax rate but your income mix changes and the company no longer qualifies as a base rate entity, you can end up with a top‑up bill when your company tax return is lodged. That is often where the “how much tax” surprise happens.

On the flip side, if you overestimate and assume the full company tax rate when your company actually qualifies for the lower rate, you might be tying up cash that could go into hiring another sparkie or upgrading vans. Clear tax planning around the correct company tax rate helps reduce both risks.

Pricing, Margins and Stepping Off the Tools

Your company’s tax obligations should sit inside your job costing, not outside of it. When you set your charge‑out rates without factoring in the real corporate tax rate and allowable deductions, the after‑tax profit can end up thinner than planned. Over time, this slows your goals of building a team and getting off the tools.

Many business owners focus on gross income and forget that corporate distributions like dividends to shareholders come after company tax. For resident companies, franking credits work by passing on the tax the company has already paid so shareholders are not taxed twice under normal income tax rules. For foreign shareholders, withholding tax rates and double taxation agreement rules can also come into play, especially where there is a permanent establishment overseas or non resident companies involved, but most local electrician companies are simply trying to keep their Australian sourced income and corporate distributions clean and well documented.

Key Concepts Electrician Companies Should Understand

You do not need to track every line of international tax rules, income inclusion rule or undertaxed profits rule, but it helps to understand a few core ideas that show up in company tax conversations with your accountant.

Corporate Income, Worldwide Income and Australian Sourced Income

Resident Australian companies are generally taxed on their worldwide income, while non‑resident companies are taxed only on their Australian‑sourced income, but for many local electrician companies the practical focus is simply reporting Australian sourced income from local jobs and projects correctly. If you start taking on overseas work or dealing with foreign shareholders, international tax rules, income inclusion rule ideas and undertaxed profits rule frameworks can start to matter.

For now, if your work is mainly in Australia, your aim is to make sure all business income, passive income and corporate income is captured correctly in your company tax return, that the right tax rate is applied, and that any franking credits are handled properly when profits are paid out.

Net Capital Gains, Capital Gains and Capital Allowances

From time to time your company might sell a vehicle, large piece of equipment, or even an asset that gives rise to capital gains. The company may have net capital gains that are included in the company’s assessable income after offsetting capital losses, which then feed into the company’s taxable income.

Separate from that, capital allowances and instant asset write off rules affect how quickly you can claim the cost of new equipment. Some assets you can immediately deduct up to certain limits, while others are written off over a number of years. All of this affects how much tax you pay in a particular income year and your overall tax position.

Practical Steps for Electrician Companies in 2026 And Beyond

Here are practical, non‑technical steps that fit how busy electrician companies actually work, without stepping into personal advice.

1. Confirm Your Company Tax Rate and Status Each Year

Do not assume your company is on the lower company tax rate just because it was last year. Ask your registered tax agent to confirm, in writing, whether your company qualifies as a base rate entity for the current income year. That means checking the base rate entity test, the company’s aggregated turnover and the passive income test against the current tax laws.

This yearly check also clarifies whether any small business concessions apply and whether your company tax planning should assume the lower or full company tax rate when you map out the next 12 months.

Power up your business with Accounting Built for Electricians

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow at every stage of growth.

2. Keep Trading Income and Passive Income Separate Where You Can

If you hold investment properties, large share portfolios or other assets that throw off passive income, consider whether they sit in the same company as your electrical business. High passive income inside the trading company can push the ratio of passive income to total assessable income up, affecting your base rate entity passive status.

While you should not restructure anything without advice, raising this with your accountant helps them check whether the way rental income, interest income and other passive income is reported could change the corporate tax rate that applies to your electrical company.

3. Build the Tax Rate into Your Cash Flow and Quotes

When you build your cash flow forecast and job costing, plug in the correct company tax rate rather than just guessing. This means using the lower company tax rate only if your company qualify as a base rate entity, and the full company tax rate if it does not.

Make sure your forecast includes expected business income, instalment income, professional fees for bookkeeping and tax, and any company tax deductions such as vehicles, tools, and software. This helps you see how much tax the company pays across the year, not just at the end.

4. Use The Right Support for Company Tax Returns

Company tax is not just an extension of your personal tax return. A registered tax agent who understands electrician businesses can help make sure your company tax returns pick up all allowable deductions, apply the correct tax rate, and clearly show how much tax you have already paid through instalments.

They can also help explain, in simple terms, how franking credits work for you as a shareholder, and how resident companies like yours interact with income tax rules when corporate distributions such as dividends are paid.

5. Track Company Tax Throughout the Year, Not Just at Tax Time

Instead of waiting until the end of the financial year to think about company tax, build it into your monthly or quarterly bookkeeping routines. Review your PAYG instalments regularly with your registered tax agent to make sure they are on track with what you actually expect to earn, and flag any changes in business income, passive income or asset sales that could shift the company tax rate you are on.

This ongoing approach means fewer surprises when your company tax return is due, clearer forecasts for planning equipment and staff, and a better sense throughout the year of how much profit is genuinely available for growth or shareholder distributions.

How ACT Tax Group Supports Electrician Companies with Company Tax

If you are like many electrician business owners, you do not want a lecture on international tax rules – you just want to know which corporate tax rate applies to your company, how it affects your cash flow, and what you need to do to stay on top of your tax obligations.

ACT Tax Group works with electrician companies to:

Clarify whether the company is likely to be on the lower company tax rate or full company tax rate for each income year, based on the base rate entity test, business income and passive income mix.

Fold that tax rate into regular forecasts so you can see how much tax the company pays and how that affects decisions on vehicles, tools and staff.

Keep records, coding and company tax returns aligned with current tax laws, so your tax position is supported and you are clear on how much tax you owe – before the bill arrives.

This article is general in nature, for illustration only and does not constitute financial or personal advice. It does not replace advice from a registered tax agent who can look at your specific structure, foreign shareholders (if any), non-resident companies in your group, or permanent establishment issues. For ATO‑compliant support that fits your electrical business, book a consult with ACT Tax Group.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)