What Is the CGT Discount and How Does It Work in Australia?

Published on January 19, 2026

The CGT discount in Australia lets eligible taxpayers reduce certain capital gains before they pay tax, which can make a big difference to the final bill. When you sell a CGT asset like an investment property, shares, or other assets, the capital gains tax discount can cut how much of the gain ends up in your taxable income. Understanding how the CGT discount works helps you plan smarter, pay less tax where the rules allow, and keep more of your money for your goals in Australia.

For many investors, capital gains arise when they sell property, managed funds, or a business for more than the cost base. Without good tax planning, you can miss out on tax concessions and pay more capital gains tax than you need to. Getting this right is not just about rules on paper; it affects your cash flow, retirement plans, and how you build wealth over each income year.

What Is the CGT Discount in Australia?

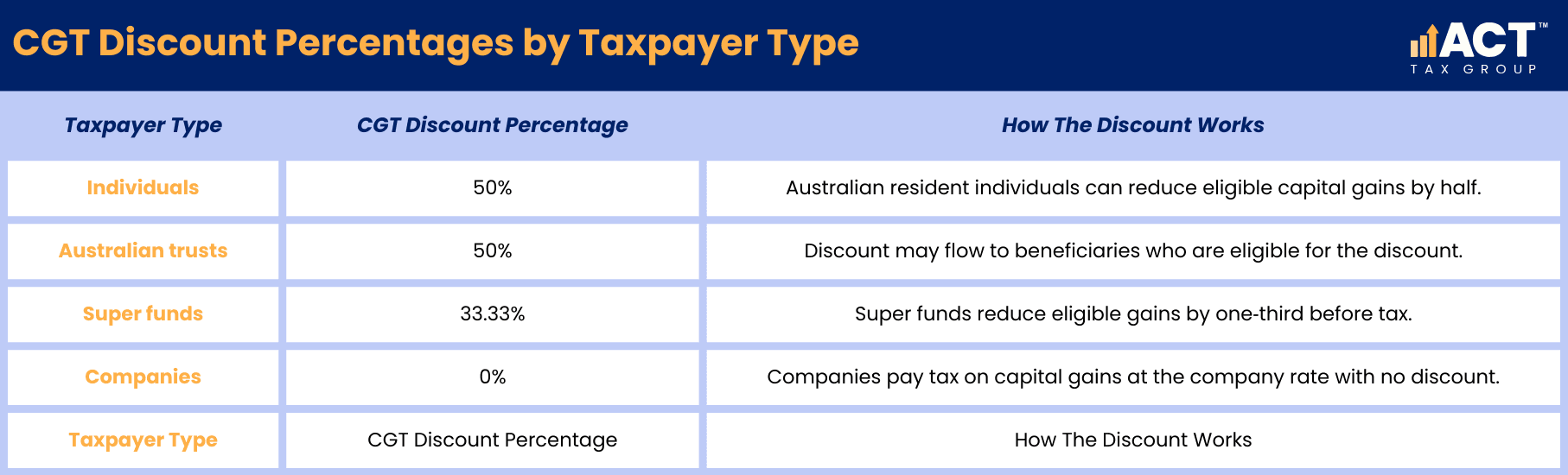

The CGT discount is a Capital Gains Tax concession that reduces eligible capital gains after you calculate your net capital gain for the year. If you are an Australian resident individual and you meet the conditions, you may receive up to a 50% CGT discount on certain gains, which means only half of the gain is added to your taxable income. Trusts can often pass the CGT discount through to beneficiaries, while super funds receive a smaller discount and companies cannot claim the full CGT discount at all.

This discount is designed to encourage longer‑term investment in assets like property, shares, and businesses rather than short‑term trading. It applies only when specific rules apply, including how long you held the asset and when the CGT event happens. By using the discount alongside other tax benefits correctly, you may pay tax at a lower rate on your capital gains than on your regular income.

Unsure how to apply losses before the CGT discount?

Schedule a complimentary consultation with us today to correctly apply capital losses and reduce your tax.

How Does the CGT Discount Work in Practice?

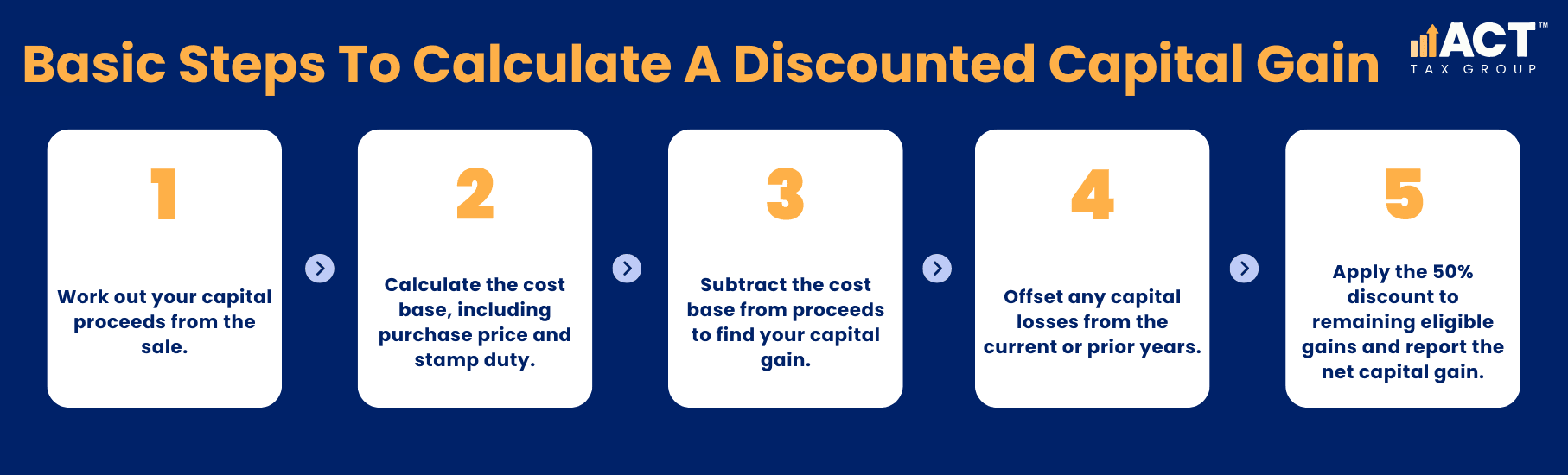

In practice, the CGT discount works as one of the final steps in your capital gains tax calculation. You first work out whether there is a gain on each CGT asset by comparing your capital proceeds to the cost base, including expenses like stamp duty and some legal costs. Once you have total capital gains for the income year, you apply any capital losses, and only then do you apply the relevant discount to the remaining eligible gain.

The result is your net capital gain, which is added to your other income and taxed at your marginal rate. This means the discount does not give you a separate lower rate; it reduces the gain that flows into your taxable income. Used well, the discount, together with other tax concessions, can reduce your overall tax burden and help you pay less tax on the sale of long‑term investments.

What Are the Eligibility Rules for the CGT Discount?

To access the Capital Gains Tax discount, you generally need to be an Australian resident for tax purposes and meet a minimum holding period. The key rule is that you must have owned the CGT asset for at least 12 months between acquisition and the CGT event. Temporary residents and foreign residents may face different rules and may not receive the full advantage of the discount, especially on certain property and business assets.

You also cannot use the discount if you choose the indexation method on older assets where different rules apply. In addition, integrity rules are in place to stop people from using artificial transactions to convert regular income into capital gains just to access the discount. These income tax integrity measures help keep the tax system fair while still allowing genuine investors to benefit from the discount.

How Does The 12‑Month Holding Period Affect Your CGT Discount?

The 12‑month holding period is central to whether the CGT discount works for a particular gain. You must have owned the asset for at least 12 months from acquisition to just before the CGT event, often measured from contract date to contract date rather than settlement. Missing this holding period by even a short time can mean you pay full Capital Gains Tax with no discount, which can be a big difference to the tax outcome.

Some situations allow you to count an earlier ownership period, such as when you receive an asset from a deceased estate or through a relationship breakdown. In these cases, the previous owner’s period of ownership may be added to yours when working out if the full CGT discount is available. Because these rules are detailed, it is often worth seeking tailored advice before you decide when to sell.

How Do Capital Losses Interact with the CGT Discount?

Capital losses can reduce your Capital Gains Tax bill, but they must be applied before you use the discount. First, you add up all your capital gains for the income year and then subtract any capital losses from the same year, and any prior year losses carried forward. Once this is done, you apply the relevant discount to any remaining gains that qualify.

This order matters because it affects how much of the gain is finally taxed. For example, if you have a large capital gain on one property and a loss on shares, using the loss first means the 50% discount is only applied to the smaller remaining amount. Thoughtful tax planning around when to sell winning and losing investments can help you manage your tax burden and use losses to your best advantage.

How Does The CGT Discount Affect Investment Property And Rental Properties?

For many investors, the CGT discount becomes relevant when they sell an investment property or rental properties. If you have owned the property for more than 12 months and you are an Australian resident, the Capital Gains Tax discount may apply to the gain after adjusting for expenses and capital losses. This can be especially important in markets where house prices have risen over time and the gain is substantial.

The cost base of a property normally includes purchase price, stamp duty, legal fees, and certain ownership expenses that are not claimed as deductions along the way. Negative gearing can affect your overall tax position each year but does not directly change whether the gain qualifies for the discount when you sell. By combining the discount with careful timing, you can often reduce how much tax you pay when you finally realise that gain.

How Do Small Business and Super Funds Use the CGT Discount?

Business owners often deal with capital gains when they sell business assets, shares in a company, or units in a trust that carries on a business. In addition to the standard discount, there are specific small business tax concessions that can further reduce capital gains, especially for active assets used in a business. In some cases, the combination of the discount and these concessions can bring the taxable gain down to a very low level or even remove it entirely.

Super funds may also apply a discount, although at a lower rate than individuals, when they hold investments like property and shares for more than 12 months. Gains in super are usually taxed at a lower rate than personal income, and in some retirement phases, certain gains may be effectively tax‑free. Putting all of this together can be complex, but the potential tax benefits are significant for long‑term retirement and business planning.

What About Integrity Rules, Affordable Housing and Policy Debates?

The CGT discount sits within a wider tax system that also tries to manage fairness and stability. Integrity rules are designed to prevent artificial transactions that aim to convert normal income into capital gains purely to access the discount. This focus on income tax integrity means that arrangements which do not reflect real investment risk and ownership may be challenged by the authorities.

There are also special rules for affordable rental housing provided through certain structures, where an additional discount or other tax benefits may apply if strict criteria are met. Policy groups such as the Grattan Institute have argued that the discount and its interaction with negative gearing and house prices should be reviewed to improve access for first home buyers and support more affordable housing. In recent submissions to a Senate inquiry established in 2025, the Institute has called for reducing the discount from 50% to 25% with a gradual phase-in. While these debates continue, the current rules still offer meaningful benefits for everyday investors who use them correctly.

How Can You Use the CGT Discount for Better Tax Planning?

Used thoughtfully, the CGT discount can be a powerful part of your tax planning and investment strategy. By choosing when to sell, which assets to sell first, and how to use capital losses, you can often pay a lower rate of tax on capital gains than on your other income. Making these choices with a clear plan in place can help you build wealth more smoothly and reduce unnecessary tax along the way.

For example, you might decide to sell a property in a year where your other income is lower, or to spread the sale of several assets over more than one income year. You might also review whether gains should be realised personally, through Australian trusts, or in super funds depending on your long‑term goals and the different rules for each. Tailored advice can help you weigh these options, rather than relying only on generic online calculators or one‑size‑fits‑all tips.

Final Thoughts on Making the Most of the CGT Discount

Understanding how the CGT discount works puts you in a stronger position when you decide to sell an asset and realise a gain. It helps you calculate your likely tax, plan around key dates, and avoid surprises when you lodge your tax return. While the basic idea is simple, the details around eligibility, different rules for different entities, and the interaction with other concessions can be complex.

If you are planning to sell property, shares, or a business and want to manage the tax impact, our team can walk you through the numbers. We focus on giving tailored advice that fits your situation, so you can make confident decisions and keep your attention on growing your business, protecting your family, and building your future. When you are ready, we can help you use the CGT discount and other tools in the tax system to reduce your tax burden and move forward with clarity.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)