When Can You Legally Withdraw Your Super in Australia?

Published on December 16, 2025

When can you legally withdraw your super in Australia is a question many people ask as they get closer to their preservation age and think about retirement. Your ability to access your super account depends on your age, your work and retirement status, and whether you meet specific circumstances known as conditions of release. Because your super savings are meant to fund your future, taking money out too early can affect your long‑term security and may lead to extra tax.

What Are the Main Ages for Accessing Your Super?

You can usually access your super when you reach your preservation age and retire, or when you turn 65, even if you keep working. Preservation age based rules link directly to your birth date, so different people reach this age at different times. Once you turn 65, your super paid to you is generally not restricted by conditions of release, and you can choose a combination of lump sum and income stream payments.

Between preservation age and 64, you generally need to be retired or use a transition to retirement income stream from your super fund to access only part of your balance. In this stage, you may still be employed, but withdrawals are limited so your money can remain invested and keep earning investment earnings inside your super account. Getting tailored advice before you reach these ages helps you understand the rules and plan when to access your super.

Concerned that early withdrawal might trigger extra ATO tax?

Schedule a complimentary consultation with us today to understand how tax applies to super withdrawals.

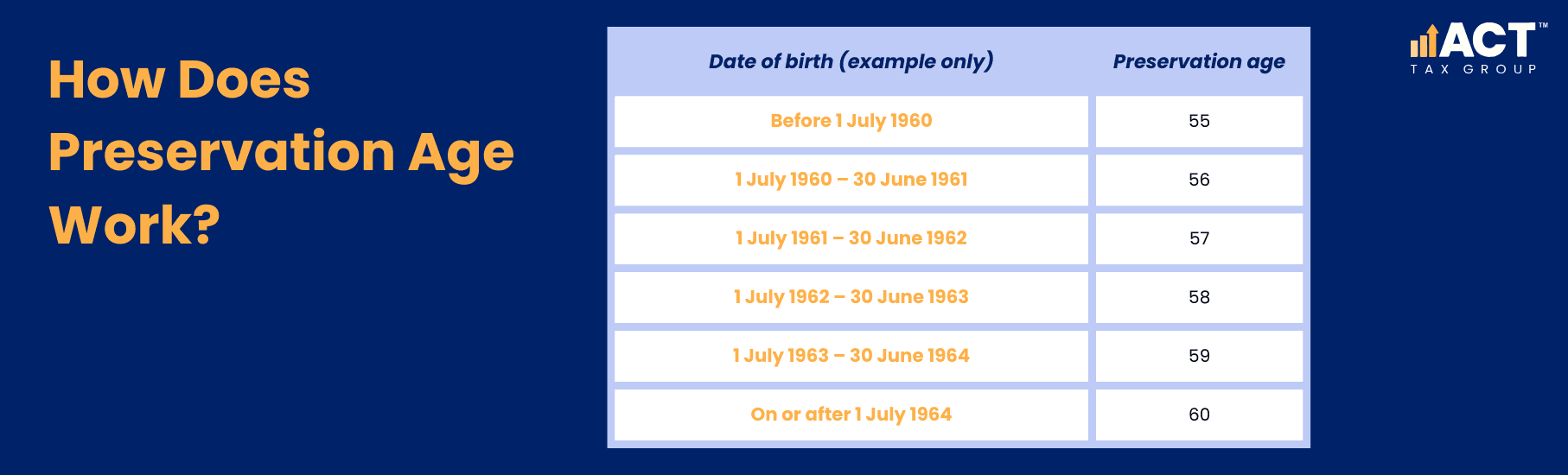

How Does Preservation Age Work?

Your preservation age is the age when you can usually withdraw your super, and it depends on your birth date. It reflects government rules designed to keep superannuation locked away until you are close to retirement. This means your super savings stay in your fund longer, with investment earnings and employer contributions building your retirement account.

Your birth preservation age sits between 55 and 60, depending on when you were born. People born on or after a set date have a preservation age of 60, while those born earlier reach theirs sooner. Checking your date of birth against a simple table on your fund’s page or the ATO site helps you confirm exactly when you can access your super.

What Does “Retirement” Mean for Super Purposes?

For super withdrawing, “retirement” is more than just deciding to stop work; it has a specific meaning under the rules. If you are 60 or over, you are usually treated as retired when you leave a job and do not plan to work more than a small number of hours per week. Once this condition is met, your fund is satisfied that you have reached a condition of release and can pay benefits.

If you retire after reaching preservation age but before 60, you may need to show that you have no intention of returning to gainful employment. The fund may ask for details such as a letter from your employer confirming your retirement date or a signed declaration from you. Being clear and honest about your plans is important, because payments made before you truly retire can be treated as early release when you do not qualify.

When Can You Use a Transition to Retirement Strategy?

You can start a transition income stream once you reach your preservation age, even while you keep working. This strategy allows you to access your super early in a controlled way by drawing a regular income stream, while your remaining balance stays invested in your fund. Many people use this approach to reduce work hours without losing too much take‑home pay.

A TTR pension has annual limits on withdrawals, so you cannot simply empty your super account. Your investment earnings in a TTR account are taxed at a maximum rate of 15% inside your fund. Once you convert to a retirement income stream after meeting a condition of release, investment earnings may become tax-free. Before switching into a transition strategy, speak with a professional to understand fees, insurance cover and how this change might affect your long‑term balance.

What Are the Standard Conditions of Release?

Standard conditions of release cover the most common ways to access your super savings. These include turning 65, retiring after reaching preservation age, and starting a transition to retirement income stream once you are old enough. Death is also a condition of release, allowing super to be paid to your eligible beneficiaries or estate.

Your fund can only release money when a condition is met and the fund rules allow that type of payment. Some accounts may have additional restrictions, especially older products or certain types of retirement account structures. Checking your product’s terms and asking your fund to explain any limits helps you understand when they can legally release money from your super.

When Can You Access Super Early on Compassionate Grounds?

In limited circumstances, you can request early access to part of your super on compassionate grounds. This pathway exists for specific circumstances such as paying for medical treatment, medical transport, palliative care, disability‑related home modifications or funeral costs for a dependant. You cannot use this option just to cover general living expenses or credit card debts.

To apply, you normally submit a request through an online page, attach supporting documents and complete the details required, such as quotes, invoices or arrears letters from your lender. If the regulator is satisfied that you meet the eligibility criteria and cannot pay these expenses any other way, they may authorise an early release amount. Your fund then pays the money to you, and normal tax on super withdrawals may apply.

How Does Severe Financial Hardship Early Access Work?

Severe financial hardship is another way some people can access their super early. To qualify, you usually need to have received government income support payments for a minimum period and still be unable to meet reasonable and immediate living expenses. This is designed for people whose money situation has become very tight and who are struggling to pay for basics, not for general spending.

There are two categories of severe financial hardship: Category A (26 weeks income support) allows $1,000–$10,000 per 12-month period with one withdrawal annually. Category B (39 weeks income support, not currently employed) allows multiple withdrawals per year with no maximum limit. The withdrawal is usually paid as a lump sum and may be taxed, so your final amount can be less than expected. Because this option reduces your retirement savings, it is important to consider advice and look at other supports before you take money out of your super.

What Other Special Circumstances Allow Early Access?

Other specific circumstances allow early access to super, including permanent incapacity, terminal illness and very small super balances. If you become permanently incapacitated and cannot return to suitable employment, you may qualify to withdraw your super earlier than the usual ages. In terminal illness cases that meet strict criteria, super can often be paid tax free, which can help with medical and family costs.

There are also rules for temporary residents leaving Australia and for small lost super accounts below a set balance. In some cases, older restricted or unrestricted non‑preserved amounts within your super can be accessed without waiting for preservation age. Each of these situations has its own eligibility criteria, so it is essential to check the rules that apply to your fund and circumstance.

How Is Super Taxed When You Withdraw It?

Tax on super withdrawals depends on your age, your super balance mix and whether you take a lump sum or an income stream. For many people who withdraw super after turning 60 from a taxed Australian fund, payments can be tax free. Before 60, some components of your super may be subject to tax when you withdraw, especially if you access your super early.

Investment earnings within your super fund are generally taxed at a lower rate while you are still in the accumulation phase. Once you move into a retirement account that pays you a regular income stream and you have met a condition of release, investment earnings on that part of your balance may no longer be subject to tax inside the fund. Getting clear advice on how tax, investment returns and withdrawals interact can make a big difference over time.

Why Is Illegal Early Access So Risky?

Illegal early access happens when money is released from your super before you qualify under the rules. This can occur if someone offers to help you withdraw your super early in exchange for a fee, or if you use an SMSF to pay yourself before a condition of release is met. These schemes often sound attractive because they promise quick money, but they can be very costly.

If payments are treated as illegal early release, you may have to pay extra tax and penalties, and your fund can lose its complying status. You could also lose insurance cover linked to your fund and severely damage your future retirement income. Staying clear of these arrangements and only accessing super through approved pathways protects both your balance and your peace of mind.

How Can Planning Help You Get the Timing Right?

Planning ahead lets you connect your retirement date, super access and other investments into one clear picture. Instead of asking “can I withdraw my super now?” in a rush, you can look at when you want to stop work, when you qualify for age pension and how much you want to draw from your super each year. This helps you balance today’s living expenses with tomorrow’s security. The Age Pension eligibility age is currently 67 years old, which is different from preservation age (55–60) and TTR access age. Understanding this helps you coordinate your super withdrawals with Age Pension entitlements.

A good plan considers your super balance, your non‑super investments, any debts, and whether you want to keep some money aside as a buffer. It also looks at how withdrawals will affect tax, age pension entitlements and any insurance you hold inside your fund. With a planned approach, you can choose the right combination of lump sum and income stream and adjust your strategy if your circumstances or employment change.

How our team can support your super withdrawal decisions

Accessing your super is one of the biggest financial decisions you will make, and it is normal to have questions about timing, tax and the impact on your future. Our team helps people across the ACT and Australia understand when they can legally access their super, how early access rules work and what each option means for their retirement income. We focus on simple explanations, so you feel confident, not overwhelmed.

If you are thinking about when to withdraw your super or whether you qualify under financial hardship or compassionate grounds, it pays to speak with a professional before you act. Our team can review your balance, your employment and your goals, and then explain your options in clear, straightforward language. Reach out to us to start a conversation about your superannuation and take the next step towards a planned, comfortable retirement.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)