How to Calculate the Medicare Levy and Surcharge for Australian Arborists

Published on December 15, 2025

How to Calculate the Medicare Levy and Surcharge for Australian Arborists is something most crews only think about when the tax return is already lodged, and the result is worse than expected. As an arborist with lumpy earnings across the financial year, it is very easy to misjudge your taxable income and end up paying more Medicare Levy and Medicare Levy Surcharge (MLS) than you thought, even when it feels like “there is not much money left over”.

When Your Tax Bill Jumps Because Of Medicare

Imagine this: you have had a strong summer of hazardous removals, storm work and emergency call‑outs, your wages from the business have gone up, you bought a new truck for the crew, and you are juggling fuel, insurance and transportation costs after a couple of big accident call‑outs. By the time you get to tax time, you feel like every dollar has gone straight back into the business.

Then your accountant finishes the tax return and suddenly there is more income tax, plus amounts to pay for the Medicare Levy and possibly the Medicare Levy Surcharge on top. You start asking how much tax is actually being taken and whether there was any way to avoid paying the surcharge if you had set things up differently with private health insurance or salary sacrifice during the year.

Unsure if your private hospital cover actually avoids the Medicare Levy Surcharge?

Schedule a complimentary consultation with us today to check your policy against ATO MLS rules and thresholds.

Step 1: Get Your Taxable Income and MLS Income Clear

The first step to calculate Medicare Levy and decide if MLS applies is to get your taxable income right for the full financial year. For an arborist, this usually includes:

Wages from your own company or employer if you are on the books

Net profit from your own arborist business if you are a sole trader or in a partnership

Any other earnings such as interest, rental income or side jobs

Your taxable income is the base for your income tax and for the standard Medicare Levy. For Medicare Levy Surcharge (MLS), the Australian Taxation Office uses ‘income for MLS purposes’, which includes your taxable income plus reportable fringe benefits, reportable superannuation contributions, and total net investment losses. That means the figure used for MLS calculations can be higher than the income you think of when you look at your bank account.

If your bookkeeping is behind or your BAS figures do not line up with your real income and costs for things like equipment, transportation and ambulance cover, the calculations for Medicare can be off and you can slide into a higher surcharge tier without realising it.

Step 2: Check If You Qualify for a Medicare Levy Reduction or Exemption

The Medicare Levy is normally 2% of your taxable income for Australian residents, but some people pay less or are exempt. The ATO website explains that there are low‑income thresholds and special rules for certain personal circumstances, such as some seniors, people who are medically unable to get Medicare benefits, or people who are not fully covered for the full financial year.

This is where your family situation matters. The rules look at your income, and sometimes your family income threshold as well, including your spouse and dependants such as kids. If you are a single parent, you might be assessed differently to a couple with one child. If your annual income is under a certain amount for the year, or you only earned income for part of the period, you may pay a reduced Medicare Levy or be exempt.

You do not choose whether to pay the Medicare Levy; it is calculated automatically in your tax return based on the ATO rules, and your job is to make sure the income and family details are accurate, so the right amount is calculated for your situation.

Step 3 Calculate the Medicare Levy for Your Arborist Income

Once your taxable income and family details are correct, the Medicare Levy itself is fairly straightforward. If you are above the low‑income range and do not qualify for an exemption, it is simply 2% of your taxable income for that year. So if your annual income from arborist work and other sources is a certain amount, 2% of that amount will be the levy you pay.

If you are close to the low‑income thresholds, the amount can be reduced rather than being the full 2%. The ATO website has detailed explanations, and there are simple online tools where you can enter your income, family situation, and period covered to estimate how much will be calculated. Using a calculator like this during the year lets you estimate how much money to put aside so the Medicare part of your tax does not knock your cash flow around when the assessment arrives.

Remember, this does not include MLS yet – that is the extra charge linked to private hospital cover, or the lack of it.

Step 4: Understand the Medicare Levy Surcharge and Private Hospital Cover

The Medicare Levy Surcharge is an extra surcharge that applies on top of the standard Medicare Levy if your income is over certain income thresholds and you do not hold an appropriate level of private hospital cover. It is aimed at medium to higher income earners who rely only on the public hospital system.

For arborists who have grown their crew and now earn strong income in good years, this can suddenly appear on the tax return once the family income threshold is crossed. Many people think that any private health insurance will avoid MLS, but that is not the case. You generally need eligible private hospital insurance, not just extras. That means cover that includes hospital treatment and meets the ATO’s rules around excess amounts and level of cover.

If you, your spouse, and your dependants (for example your first child and any younger kids) do not hold an appropriate level of hospital cover for the full financial year, and your income for MLS purposes sits above the relevant income thresholds, you may have to pay the surcharge. If the cover only applies for part of the year, the surcharge may be calculated just for the period you were not covered.

Step 5: Work Out Your MLS Tier And Estimate the Surcharge

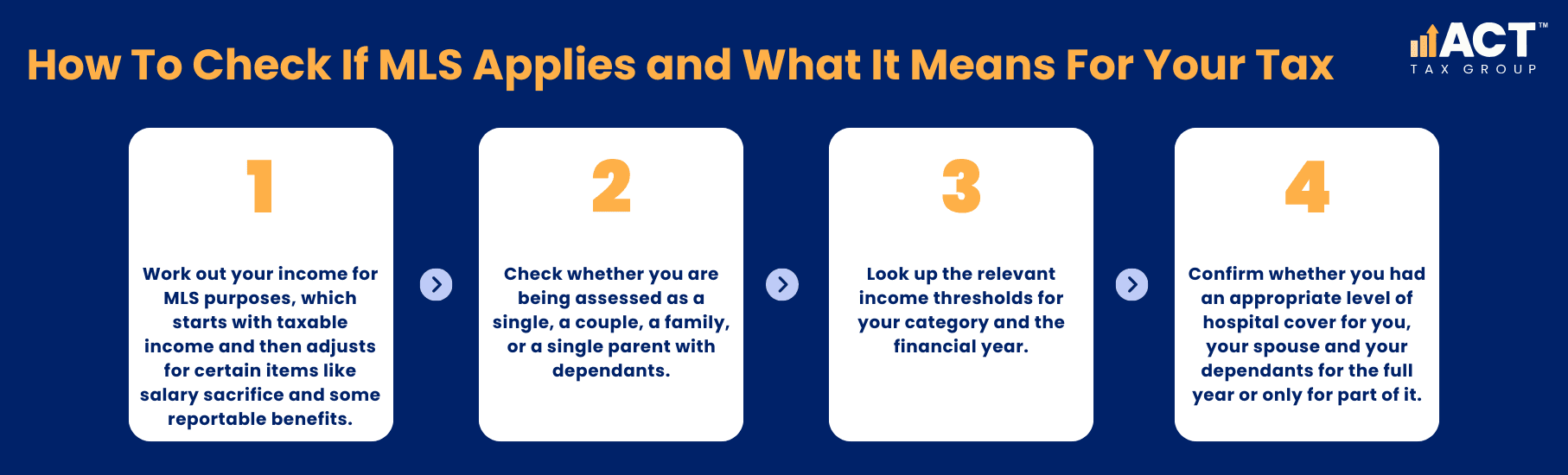

To estimate whether you will pay MLS and how much it could affect your tax, you need to:

Work out your income for MLS purposes, which starts with taxable income and then adjusts for certain items like salary sacrifice and some reportable benefits.

Check whether you are being assessed as a single, a couple, a family, or a single parent with dependants.

Look up the relevant income thresholds for your category and the financial year.

Confirm whether you had an appropriate level of hospital cover for you, your spouse and your dependants for the full year or only for part of it.

The surcharge is calculated as a percentage of your income for MLS purposes, using different percentage rates depending on which tier you fall into. The higher your income and the higher your tier, the higher the surcharge rate. That percentage is then applied to your MLS income, similar to how the 2% Medicare Levy is applied to taxable income.

This is where a Medicare Levy Surcharge calculator or an income tax calculator can help you estimate the dollar impact. You enter your annual income, your family situation, whether you had private hospital cover, and for what period. You then see an estimate of how much extra tax might be payable as MLS if you did not meet the conditions.

Step 6: How Private Health Insurance Rebate and Tax Offset Fit In

The Australian Government rebate on private health insurance can reduce what you pay for premiums if you are eligible, based on your age and income. If you claim the rebate as a reduced premium through your insurer, your tax return will later balance things out based on your actual income for the year.

If you claim the rebate as a tax offset at tax time instead of through your policy, it can reduce the overall tax you pay. However, the rebate itself does not remove the MLS, and only holding appropriate private hospital cover can help you avoid paying the surcharge

The key point for arborists is that an appropriate level of private hospital cover can help you avoid paying the surcharge in the first place, and the rebate can take some of the sting out of premiums. But you still need to check the details of your policy, such as the type of cover, benefits, hospital excess, and whether all family members are included, so that it actually matches the MLS rules.

Grow your tree care business with Accounting Built for Arborists

From start-up to expansion, our accounting team supports your tax, payroll, and cash flow — so you can focus on running your business safely and profitably.

Why Arborists Feel the Medicare Impact More

Because arborist income is often seasonal, you might earn a lot in one period and much less in others. It is common to push hard through a busy season, take on extra staff, pay more wages and overtime, invest in equipment, and then face quiet months where every dollar counts. When that happens, it can feel like you should be paying less tax because there is not much cash left in the account.

The problem is that the income tax, Medicare Levy and any MLS are based on your actual annual income for the full financial year, not how much money you have in the bank at a particular moment. So a strong run of high‑value jobs, even if mixed with quiet patches, can still push your taxable income and MLS income into higher brackets, even after claiming fuel, maintenance, insurance and other costs.

This is why many arborists get caught out by Medicare – it is not that the calculations are unfair, it is that the way cash flows in the business does not match the timing of the tax and levy calculations.

Practical Steps to Manage Medicare Levy and MLS as an Arborist

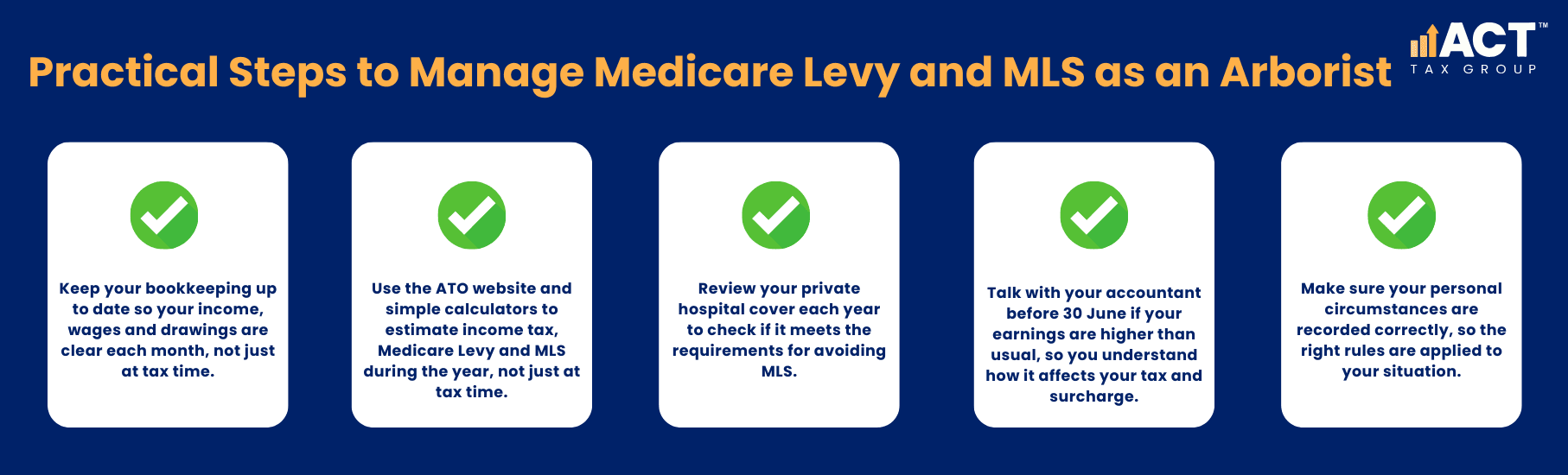

To keep control and avoid surprises around Medicare Levy and the surcharge, you can:

These steps do not promise less tax, but they do help you understand what will be calculated and give you time to plan for the payment instead of being blindsided.

How ACT Tax Group Can Help You Stay Ahead

If you are like most arborists in ACT and the South Coast, you just want to know how much tax you will pay and how much you actually get to keep after the work, the fuel, the gear and the crew. Medicare, MLS, thresholds and cover levels are not what you want to think about after a big day on site.

At ACT Tax Group, the focus is on keeping it simple and practical. That means setting up clean accounts, keeping your numbers current, and walking you through how Medicare Levy, MLS and income thresholds work in your specific situation. You stay on top of your obligations, understand what is being calculated and why, and have fewer surprises when it comes time to lodge your tax return.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)