How Do the Electric Vehicle FBT Exemptions Work for Plumbing Businesses?

Published on December 9, 2025

As a plumbing business owner in the ACT, you have probably seen ads for Electric Vehicles and novated lease deals that promise tax savings and say the car is “exempt from FBT”. The real question is whether the Fringe Benefits Tax exemption for EVs will actually apply to your situation, or whether you will still end up having to pay Fringe Benefits Tax on private use.

A Realistic EV Scenario for a Plumbing Business

Let’s start with a situation you might recognise. You are slammed with emergency hot water jobs one week and then it is dead quiet the next. In the middle of that, a dealer or salary packaging provider calls you with “great news” about a Battery Electric Vehicle that is a low emissions vehicle and “eligible for the FBT exemption”. They talk about pre-tax salary deductions, novated lease arrangements, and how you will not have to pay FBT.

You are probably thinking about whether this Electric Car is actually an eligible Electric Car for the electric vehicle exemption, whether there will be any Fringe Benefits Tax payable if you use the car for both work and private use, and how the Luxury Car Tax threshold and the LCT threshold for fuel efficient vehicles affect whether the car is exempt. This is where many Plumber Pete–style owners get stuck. You want the benefits of Electric Vehicles and lower running costs, but you do not want a surprise at FBT year end.

Worried your EV might still trigger FBT?

Schedule a complimentary consultation with us today to confirm your EV meets ATO FBT exemption rules and avoid surprise tax bills.

What Makes an Electric Vehicle Eligible for the FBT Exemption

The first step is to work out whether the vehicle itself qualifies for the electric vehicle FBT exemption. If it does not meet the rules as an eligible Electric Car, any private use could be a car fringe benefit with a taxable value that may mean you have to pay Fringe Benefits Tax.

The Basic Vehicle Conditions

For FBT purposes, an Electric Vehicle needs to meet several conditions to be treated as an Electric Car exemption. The vehicle has to be a zero or low emissions vehicle, such as a Battery Electric Vehicle or a hydrogen fuel cell Electric Vehicle, and it must be a car designed to carry less than one tonne and fewer than nine passengers, so it is still considered a car for FBT purposes. The vehicle must have been first purchased or otherwise first held and used on or after the relevant date set in the law for EVs eligible for the FBT exemption, and the car must never have had Luxury Car Tax payable on any retail sale or importation.

If you are looking at a second-hand Electric Car, you still need to check whether any Luxury Car Tax was payable when it was first sold. If LCT was payable at that time, it will not be eligible for the FBT exemption for EVs, even if it is now cheaper and looks like a bargain.

Why The Luxury Car Tax Threshold Matters

The Luxury Car Tax threshold for fuel efficient vehicles is a key part of whether an Electric Vehicle qualifies for the FBT exemption. The rule is that the value of the vehicle must be below the fuel efficient LCT threshold at the time of the first retail sale and any later retail sale. If the cost of the vehicle goes above that LCT threshold at any of those points, the Electric Vehicle exemption does not apply.

As a plumbing business owner, you need to check the original cost and whether it was treated as a fuel efficient vehicle, confirm whether Luxury Car Tax was payable when it was first purchased, and understand that a high-end Electric Vehicle above the LCT threshold might not qualify, even if it is clearly a low emissions vehicle. If Luxury Car Tax was payable on any earlier sale, you will not get the Fringe Benefits Tax exemption, and you may have to work out the taxable value of car fringe benefits and pay FBT on private use.

Private Use Car Fringe Benefits and Your Team

Once the vehicle itself ticks the boxes, the next question is how it will be used by you, your employees, and sometimes your family members. Even when a car is eligible for the electric vehicle FBT exemption, private use still matters for reporting and for your employees’ taxable income position.

What Counts as Private Use for a Plumbing Business

For a plumber, private use of a car can include driving from the employee’s home to the first site in the morning, personal trips on weekends or after hours, or any use that is not directly linked to plumbing work. Under normal rules, this private use would create car fringe benefits with a taxable value that could mean you need to pay FBT. When the car is an eligible Electric Vehicle and meets all the conditions, those car fringe benefits can be FBT exempt. This usually means the employer does not have FBT payable on that Electric Car, but the value of the exempt benefit may still be treated as a reportable fringe benefits amount for the employee, which can affect things like the Medicare levy and other income-tested government items.

So, while you may not need to pay Fringe Benefits Tax, you still need to know how much private use there is and keep basic records.

Apprentices Leading Hands and Shared Vehicles

If you provide an Electric Vehicle to a leading hand or apprentice for work and private use, you still need to consider whether the vehicle is a zero or low emissions Electric Vehicle that is eligible for the FBT exemption, whether the cost is under the LCT threshold for fuel efficient vehicles with no LCT payable, and whether the employee is a current employee and the vehicle ever carries more than one tonne or more than eight passengers. If those points are satisfied, the private use benefits for that employee can be exempt from FBT. But if any condition fails, the Electric Vehicle becomes a normal car benefit, and you may have to calculate the taxable value and pay FBT.

How Novated Leases and Salary Packaging Fit In

Many plumbers hear about the ev FBT exemption in the context of a novated lease or salary packaging arrangement. This is where an employee’s pretax salary deductions are used to pay the lease and running costs of the Electric Vehicle.

Novated Lease Arrangements and Tax Savings

Under a novated lease arrangement, the employee enters into a lease for the vehicle, and the employer agrees to take on the lease obligations while the employee works for them, with payments often salary sacrificed using pretax salary deductions. With an Electric Vehicle that is eligible for the FBT exemption, the private use car fringe benefits through a novated lease can be fbt exempt. This means the employer may not have to pay FBT on that Electric Vehicle, the employee can still see tax savings because part of their taxable income is replaced by pre tax salary deductions, and the benefit provided may still be reportable, even though it is exempt from FBT.

If the vehicle is not eligible for the Electric Car exemption, the employer may need to pay FBT or structure the payments so that the employee effectively covers the FBT cost using both pretax and after-tax contributions.

Running Costs Charging Costs and FBT

Plumbing business owners also want to know how running costs are treated. It is not just about the car. It is also about insurance, repairs, registration and electricity used to charge the vehicle.

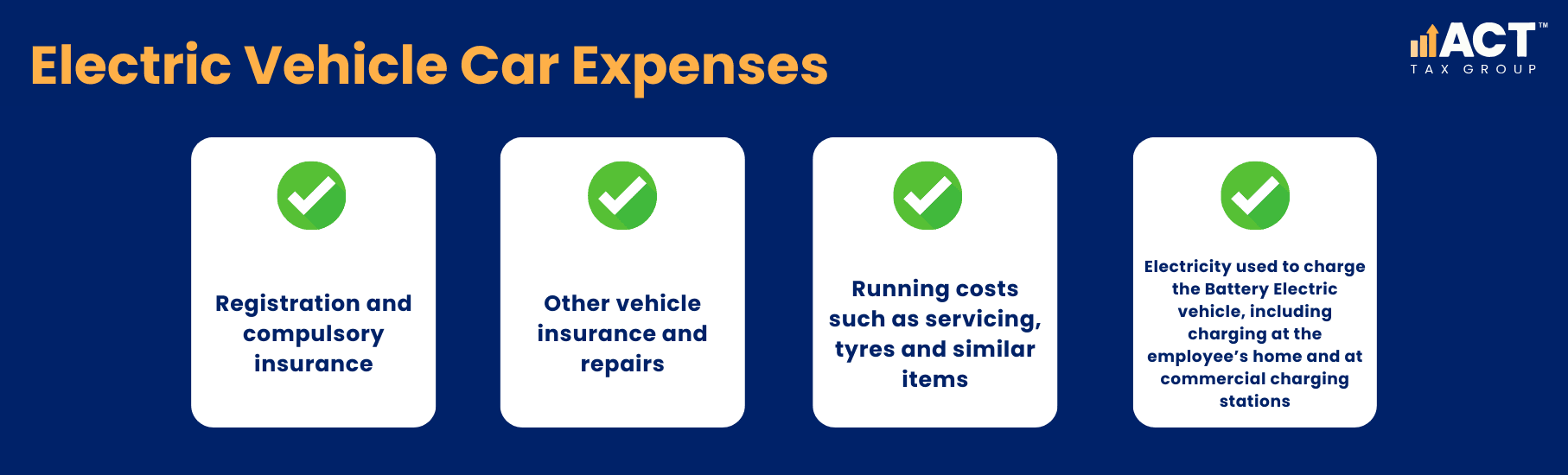

EV Car Expenses and What Is Covered

When an Electric Vehicle qualifies for the FBT exemption, the general position is that associated car expenses that relate to that vehicle are treated in line with the exemption. These EV car expenses can include registration and compulsory insurance, other vehicle insurance and repairs, running costs such as servicing, tyres and similar items, and electricity used to charge the Battery Electric vehicle, including charging at the employee’s home and at commercial charging stations. For home charging, there are ATO methods that allow employers to treat charging costs as exempt and still have a clear basis for valuing the electricity, often using a cents-per-kilometre rate for the FBT year. To use these methods properly, you generally need odometer records and a simple way to track total kilometres.

Plug In Hybrid Electric and Hybrid Electric Vehicles

Plug in hybrid Electric vehicles and other hybrid Electric vehicles sit in a slightly different category. Some plug in hybrid Electric vehicles were treated as low emissions vehicles and were eligible for the FBT exemption for EVs in earlier years, but this treatment is changing and from certain dates plug in hybrid Electric vehicles may no longer be treated as low emissions vehicles for FBT purposes. If you are considering a plug in hybrid Electric vehicle for your plumbing fleet, you need to check whether the date you purchase and make the vehicle available to employees is before or after the key date when plug in hybrid Electric vehicles are longer exempt, whether any transition rules apply to existing leases or vehicles, and how this affects your FBT payable position and any future lease or residual value decisions.

Because these changes are date-driven and depend on individual circumstances, it is important to confirm the current rules before signing a lease or purchase agreement.

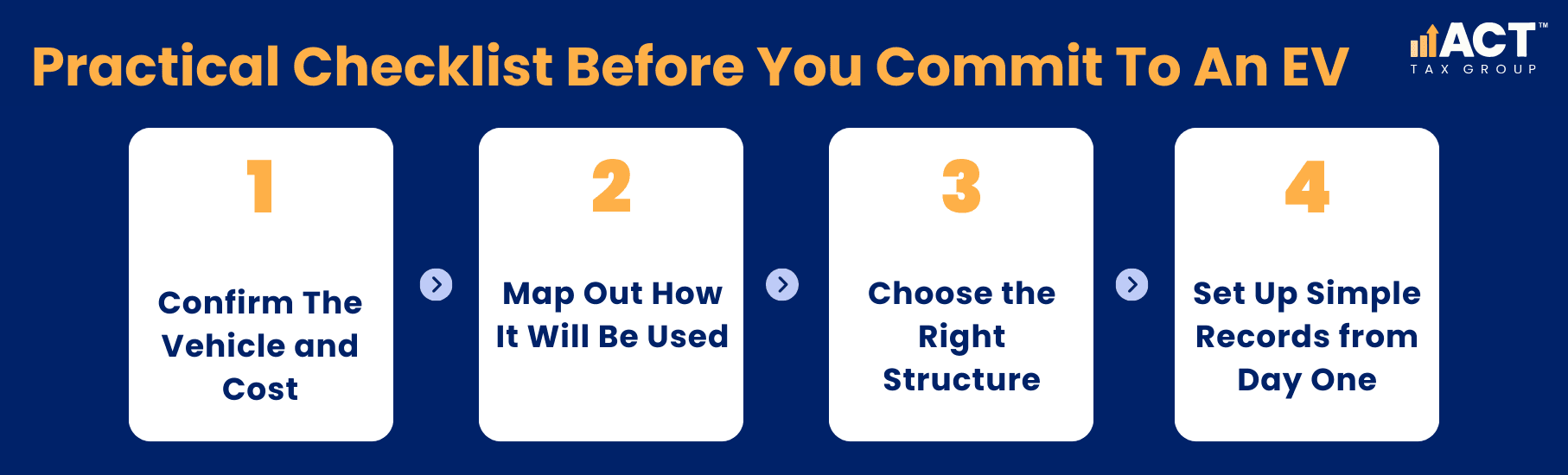

Practical Checklist Before You Commit To An EV

If you are weighing up Electric Vehicles for your plumbing business and want to make sure you qualify for any Electric Vehicle exemption without FBT surprises, here is a simple, practical checklist.

Step 1: Confirm The Vehicle and Cost

Check that the vehicle is a zero or low emissions Battery Electric Vehicle or hydrogen fuel cell Electric Vehicle.

Make sure it is a car designed to carry less than one tonne and fewer than nine passengers.

Confirm that the cost when first purchased was below the Luxury Car Tax threshold for fuel efficient vehicles and that Luxury Car Tax was not payable on any retail sale.

Step 2: Map Out How It Will Be Used

Decide who will drive the vehicle: you, a current employee, or more than one team member.

Be clear about how much private use is expected, including travel between the employee’s home and jobs, and trips by family members.

Understand that this private use is what would normally create car fringe benefits and taxable value for FBT purposes, and that the exemption only applies if the vehicle is eligible.

Step 3: Choose the Right Structure

If you use a novated lease or salary packaging arrangement, make sure the lease terms, residual value, and payment structure are clear.

Confirm how pre tax salary deductions will work and how any salary sacrificed amounts will affect the employee’s taxable income.

Plan what happens if the Electric Vehicle rules change in a later FBT year.

Step 4: Set Up Simple Records from Day One

Record the date the vehicle is first purchased and first used and keep copies of tax invoices showing no LCT was payable.

Keep odometer readings at least at the start and end of each FBT year and when employees change.

Track running costs and charging costs so you can clearly show which amounts are linked to an Electric Vehicle that is FBT exempt.

Conclusion

For plumbing businesses, the Electric Vehicle FBT exemption can be a genuine opportunity to update vehicles, manage running costs, and offer benefits to employees without having to pay FBT, provided the vehicle, cost, and usage meet all of the requirements. The key is making sure the car is an eligible Electric Car under the rules, stays under the fuel-efficient Luxury Car Tax threshold, and is used by a current employee under a structure that fits within the FBT exemption for EVs.

Because the rules involve detailed tests, dates, and thresholds, and because things like plug in hybrid Electric vehicles and hybrid Electric vehicles are changing around 1 April 2025 and later, it is important to get personalised help before you rely on any exemption. This article is general in nature, for illustration only and does not constitute financial or personal advice. For ATO-compliant support that looks at your vehicles, leases, and plumbing business in detail, book a consult with ACT Tax Group and get clear guidance before you commit.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)