Electric Vehicle FBT Exemption: Eligibility Criteria and How to Claim

Published on November 3, 2025

Electric vehicle FBT exemption eligibility criteria and strategies for claiming remain essential for employers and current employees looking to reduce the cost of company cars and lower emissions. With vehicles such as battery electric and hydrogen fuel cell cars now eligible—provided they meet zero or low emissions requirements and are under the Luxury Car Tax threshold—businesses can achieve significant tax benefits while supporting the broader shift to fuel efficient vehicles.

Accessing this exemption for electric vehicles affects personal circumstances and overall running costs, making it especially relevant for designated employees who use company cars for private use. Understanding the Fringe Benefits Tax (FBT) rules and accurately determining eligibility criteria is crucial, especially as the federal government tightens compliance around plug in hybrid electric eligibility after 1 April 2025.

What Are the Electric Vehicle FBT Exemption Eligibility Criteria?

Electric vehicle FBT exemption applies to eligible electric cars, including battery electric vehicles (BEVs) and hydrogen fuel cell vehicles. Vehicles must not have ever exceeded the Luxury Car Tax (LCT) threshold at retail sale and need to be first held and used from 1 July 2022 onwards for private use by a current employee or their family members. Hybrid vehicles such as plug in hybrid electric models remain eligible with a financially binding commitment prior to 1 April 2025. The car must carry less than one tonne and seat less than nine people to qualify for exemption.

Employers must ensure no LCT was paid on the vehicle and that all paperwork supports exemption status. Hybrid electric vehicles and fully electric vehicles must be checked against the FBT exemption threshold and cannot involve motorcycles, scooters, or extended lease arrangements beyond new commitment limits.

Need help reporting exempt EV benefits correctly?

Schedule a complimentary consultation with us today to ensure accurate ATO disclosure and record-keeping.

Eligibility criteria include:

Zero or low emissions vehicle status

First held and used after 1 July 2022

Never subject to Luxury Car Tax (LCT)

For private use by current employees or family members

Plug in hybrid electric eligible only under certain agreements

Meets requirements for weight and passenger capacity

How the Exemption Supports Businesses and Employees

Fringe Benefits Tax, or FBT, historically increased the total cost of providing company cars, but exemption for electric cars allows both employers and employees to offset taxable value exposures. Great news for fleets—salary packaging arrangements such as novated lease payments now offer lower on road costs and residual value certainty by using electric vehicle exemption under the latest federal government rules.

Electric vehicles are now more accessible, with running costs such as charging costs exempt for fringe benefit tax purposes. A novated lease setup for an eligible electric vehicle means the employee’s home charging rate, GST inclusive EV car expenses, and lease payments contribute toward substantial savings across the financial year.

Benefits include:

Lower running costs for eligible electric cars

Reduced Fringe Benefits Tax bills for employers

Improved salary package flexibility for employees

Fuel efficient transition, supported by federal government incentives

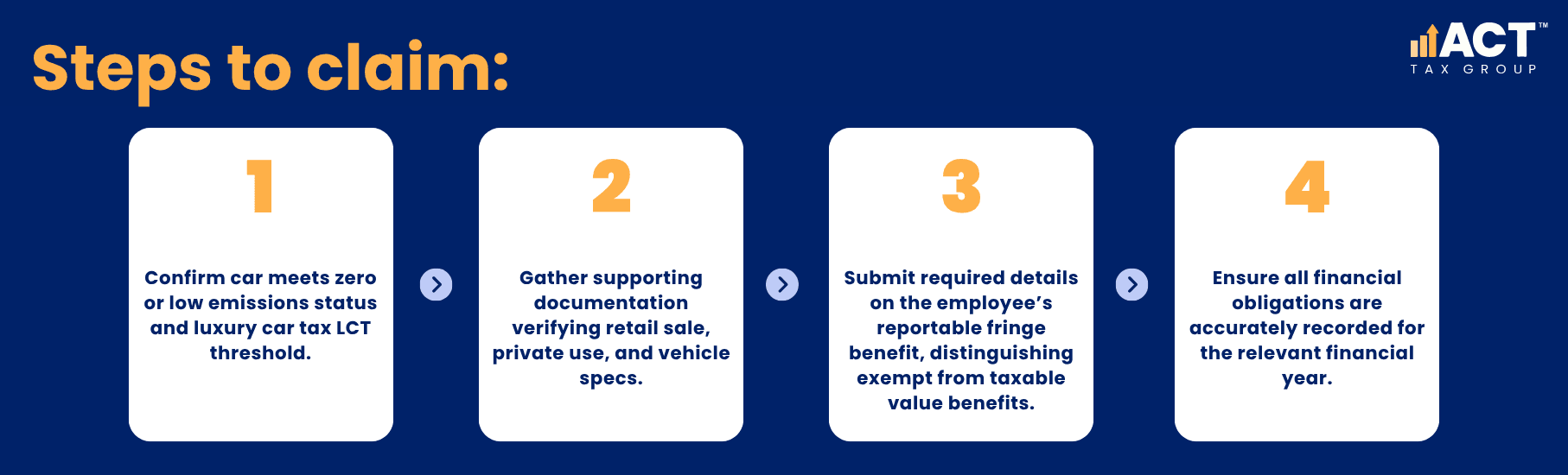

How Do You Claim the Electric Vehicle FBT Exemption?

Claiming FBT exemption for electric vehicles begins by confirming all eligibility criteria for the particular employee and their vehicle. Start by verifying the car against ATO definitions for eligible electric cars, then collect all necessary records, including retail sale documents, novated lease agreement if applicable, and evidence of private use and residual value.

Employers should report the exempt benefit as a reportable fringe benefit on the employee’s year-end summary. Charging costs, lease payments, and other EV home charging expenses for designated employees—and their family members—are covered for FBT purposes if correctly documented. Retain all relevant documents for at least five years in line with ATO rules.

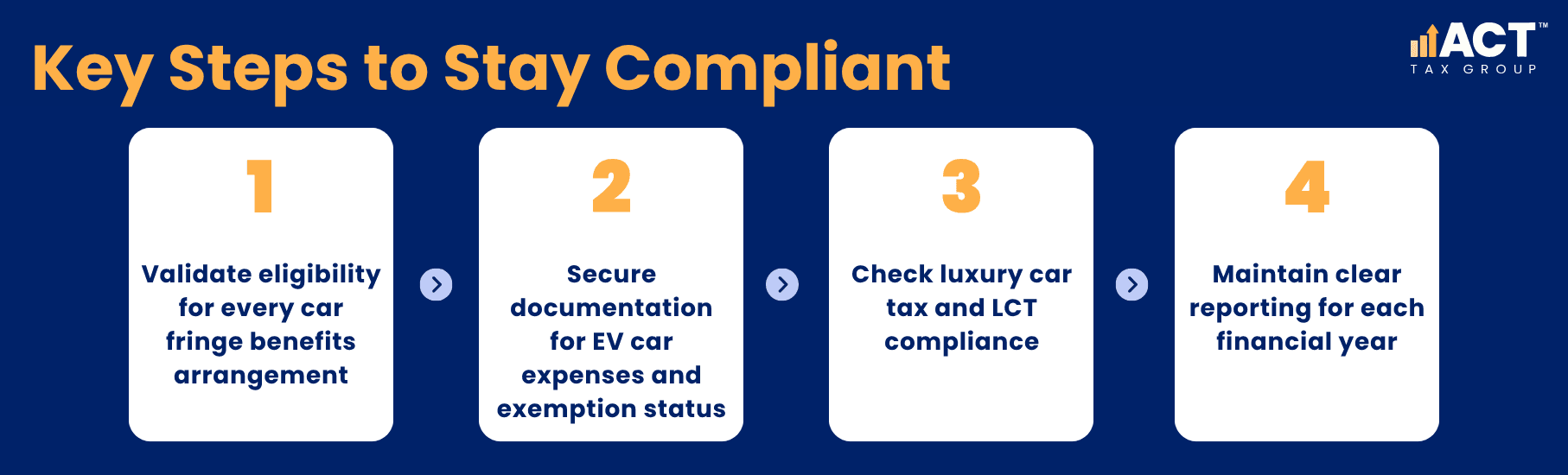

The 2025 Legislative Changes for Plug in Hybrid Electric Vehicles

From 1 April 2025, plug in hybrid electric vehicles will no longer be exempt from FBT except under financially binding commitments signed before that date. Hybrid vehicles that previously qualified under older agreements can maintain exemption—as long as no optional extension or new commitment is made. Employers and employees must review all current leases and salary package arrangements to avoid losing the exemption.

Transitioning to fully electric vehicles is recommended for upcoming company car purchases and novated lease renewals. Monitoring lease payment cycles and on road costs for hybrid electric vehicles is now essential, with residual value and total cost closely tied to ongoing eligibility.

Transition checklist:

Audit existing plug-in hybrid electric vehicle commitments for compliance

Review new company car acquisitions for exemption eligibility

Adjust salary packaging agreements before renewal dates

Plan transition from hybrid electric vehicles to battery electric vehicles

Examples for Businesses and Employees

Many Australian companies have realised significant savings by transitioning to eligible electric vehicles within the FBT exemption program. Salary packaging through novated lease arrangements for battery electric vehicles, hydrogen fuel cell cars, and other fuel-efficient vehicles have demonstrated substantial cost reductions, with lower GST inclusive lease payment exposures and charging costs now exempt from Fringe Benefits Tax.

Real-world case studies show annual employee savings, improved company car affordability, and stronger compliance on car fringe benefits for both employer and designated employee roles. The benefit applies not just to running costs but also supports sustainable fleet management in line with federal government objectives.

Examples include:

Sydney business savings of over $50,000 in their first year from eligible electric car exemptions

Employees reporting up to 30% lower running costs and improved salary package outcomes

Stronger compliance through accurate record-keeping and review of personal circumstances and reportable fringe benefit declarations

Vehicle Model | Employee Savings (Annual) | Employer FBT Reduction | Eligibility Criteria |

|---|---|---|---|

Tesla Model 3 | $4,400 | $7,650 | Battery electric, exempt from FBT |

Hyundai Kona Electric | $5,100 | $8,500 | Fully electric, meets weight/passenger rule |

MG ZS EV | $3,950 | $6,800 | Electric vehicle exemption |

Mitsubishi Outlander PHEV (pre-2025) | $4,100 | $7,500 | Hybrid vehicle, financially binding commitment |

Supporting Statistics and Expert Insights

The electric vehicle FBT exemption has driven rapid uptake in eligible electric vehicles for business use, with year-on-year growth in electric car purchases. The federal government reports a notable rise in businesses offering novated lease options and salary packaging tailored to fully electric vehicles and hybrid vehicles—especially those exempt from Fringe Benefits Tax. Accurate determination of taxable value and reportable fringe benefit amounts remains essential for compliance and maximising benefits. Expert accountants continue to emphasise the importance of reviewing eligibility criteria and financial obligations every year.

Frequently Asked Questions

What if my electric car exceeded the Luxury Car Tax threshold?

You cannot claim the exemption if LCT applied during retail sale.

How does salary packaging affect eligibility for the FBT exemption?

Salary packaging and novated lease arrangements are eligible, provided all criteria are met and running costs like charging are included.

Can company cars used partly for business and private use be exempt?

Only if the vehicle’s private use aligns with Fringe Benefits Tax rules and is for a particular employee or their associates.

Conclusion

The electric vehicle FBT exemption unlocks substantial tax savings for businesses and employees who meet strict eligibility criteria. Companies must review vehicles against the Luxury Car Tax threshold, assess private use and residual value exposures, and maintain documentation to accurately determine financial obligations and compliance. ACT Tax Group recommends auditing your company cars and salary package arrangements regularly, examining novated lease options for eligible EVs, and obtaining further information from trusted accounting professionals.

Early adoption and careful compliance will ensure you are exempt from FBT on eligible electric cars and hybrid vehicles, creating real opportunities for sustainable fleet management and improved running costs for employees and their families.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)