Understanding the Corporate Tax Rate for Small Plumbing Businesses in Australia

Published on October 20, 2025

Understanding the corporate tax rate for small plumbing businesses in Australia can make a real difference to how much you pay at year end and what you keep in the bank. If you run a plumbing business in the ACT, you already know that cash flow can feel like a rollercoaster, invoices take forever to get paid, and every BAS lodgement brings stress. The good news is that the rules around company tax rates are simpler than you think once you know what to look for.

What Corporate Tax Rate Do ACT Plumbers Actually Pay?

The most common question from plumbing business owners is, “What company tax rate do we pay?” Here’s the straightforward answer for the current income year.

Australian companies, including small plumbing businesses, pay either 25% or 30% company tax on their profit for the 2024–25 financial year. The rate you pay depends on your company’s aggregated turnover and where your income comes from. If your aggregated turnover is under $50 million and no more than 80% of your total assessable income is passive income (like rent, interest income, or dividends), you qualify as a base rate entity and pay the lower 25% rate. Companies that don’t meet these circumstances pay the full company tax rate of 30%.

For most small plumbing businesses in the ACT who earn their income from actual plumbing work—callouts, maintenance contracts, renovations—the 25% base rate applies. Passive income is not usually a factor unless you hold significant rental properties or investment assets through the company.

Are you paying the right company tax rate?

Schedule a complimentary consultation with us today to confirm your eligibility for the 25% base rate.

Example: Determining Your Rate

Assume ACT Pipe Solutions Pty Ltd operates a plumbing business with revenues of $420,000 from trading income and $3,000 in interest from a business savings account. The total assessable income is $423,000. Only 0.7% of income comes from passive sources (interest income), well under the 80% threshold. The company qualifies as a base rate entity and pays 25% tax on its profit.

If the same business had rental income of $350,000 and only $70,000 from plumbing work, then 83% of income would be passive. In these circumstances, the company would pay the full 30% rate.

How Do You Know Which Rate Applies to Your Business?

Many plumbing business owners assume the tax rate based on turnover alone, but eligibility for the base rate also depends on the type of income your company earns. Here’s what the ATO looks at:

Aggregated Turnover

This is your total ordinary income from business operations in Australia, plus the turnover of any connected or affiliated entities. It does not include GST you collect or capital gains. For small business entities with aggregated turnover under the threshold, many concessions and the lower tax rate can apply.

Passive Income Test

To qualify for the base rate, no more than 80% of your assessable income can come from passive sources. Passive income includes rent, interest, dividends, royalties, and net capital gains (excluding gains on assets used in the business). Trading income from plumbing work is active income and supports your eligibility for the 25% rate.

If your company structure includes multiple entities or you operate through a trust that distributes to a company, speak to your accountant about how aggregated turnover and income inclusion rules apply. These rules can be complex, and misleading assumptions can cost you when lodging company tax returns.

What Counts as Taxable Income for Plumbing Companies?

Taxable income is the amount left after you subtract allowable deductions from your total assessable income. For plumbing businesses, total assessable income typically includes:

Trading income from plumbing jobs, emergency callouts, maintenance contracts, and quoted work

Interest income from business bank accounts

Rental income if the company owns and leases property or equipment

Capital gains from selling company assets (like vehicles or equipment), although the taxable portion may be reduced by capital gains concessions if you qualify as a small business entity

Your profit is what’s left after deducting the cost of materials, wages, vehicle expenses, tools, insurance, rent, interest on business loans, and other operating expenses. The company pays tax on this profit at either the base rate or full rate, depending on eligibility.

ACT Plumbers—What You Can Claim and What Triggers Compliance Stress

Most plumbing business owners feel the pressure around BAS time, payroll for apprentices, and keeping on top of receipts and invoices. Cash flow is uneven, paperwork piles up, and it’s hard to know what you can and can’t claim. Here’s how to stay compliant and reduce stress:

Vehicles

If the company owns the work ute or van, you can claim running costs like fuel, servicing, insurance, registration, and interest on any vehicle loan. Deductions are limited to the business-use portion, so keep a logbook to show how much the vehicle is used for work versus private use. For new vehicles, depreciation applies, with a cost limit for certain tax concessions.

Tools and Equipment

Individual tools and equipment costing less than the relevant threshold can be claimed immediately under small business instant asset write-off rules (if your aggregated turnover qualifies). Items above this cost are depreciated over their useful life. Keep receipts and records for every purchase.

Repairs and Maintenance

The cost of repairing and maintaining business assets (vehicles, tools, equipment) is deductible. Major upgrades or improvements to the asset are treated as capital expenses and depreciated.

You must have records to support every claim. Without receipts, logbooks, and invoices, the ATO can disallow deductions and apply penalties.

Payroll, BAS, and Compliance Deadlines

Managing payroll, BAS, and compliance deadlines is one of the biggest ongoing challenges for plumbing business owners across the ACT. By knowing what’s due, when to pay, and how to keep your systems organised, you can stay compliant, protect your cash flow, and avoid unnecessary fines.

Apprentice Payroll

Follow the relevant industry award for wages, allowances, overtime, and superannuation. Single Touch Payroll (STP) reporting is required for all employees, including apprentices. Don’t leave payroll to the last minute or assume you can catch up later—the ATO monitors STP data in real time.

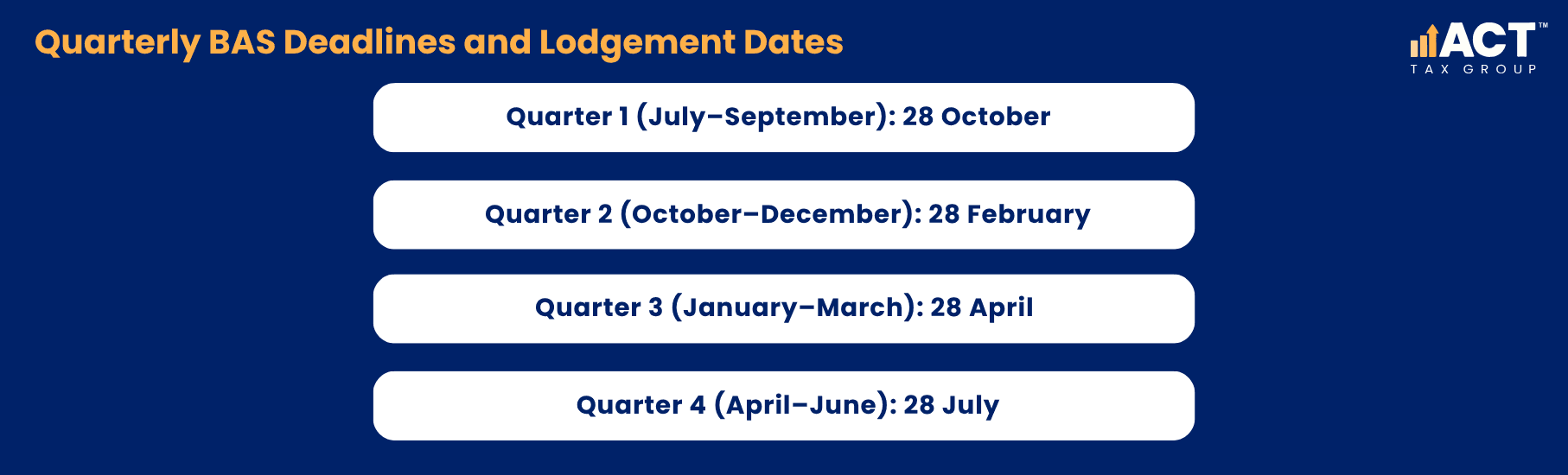

BAS Lodgement

Most small plumbing businesses lodge BAS quarterly. The due date for each quarter is generally 28 days after the quarter ends:

If you use a registered BAS agent, you may get an extension. Missing the due date triggers penalties and interest, starting at over $300 per period and increasing with repeated lateness.

GST Registration

If your GST turnover is $75,000 or more, or you expect it to reach that level, you must register for GST within 21 days and start lodging BAS. GST turnover is your total business income (excluding GST itself and certain financial supplies).

Taxable Payments Annual Report (TPAR)

If you pay contractors for building and construction services, you must lodge a TPAR by 28 August each year. This report lists payments made to contractors, including their ABN and the amount paid. Failing to lodge on time can result in penalties.

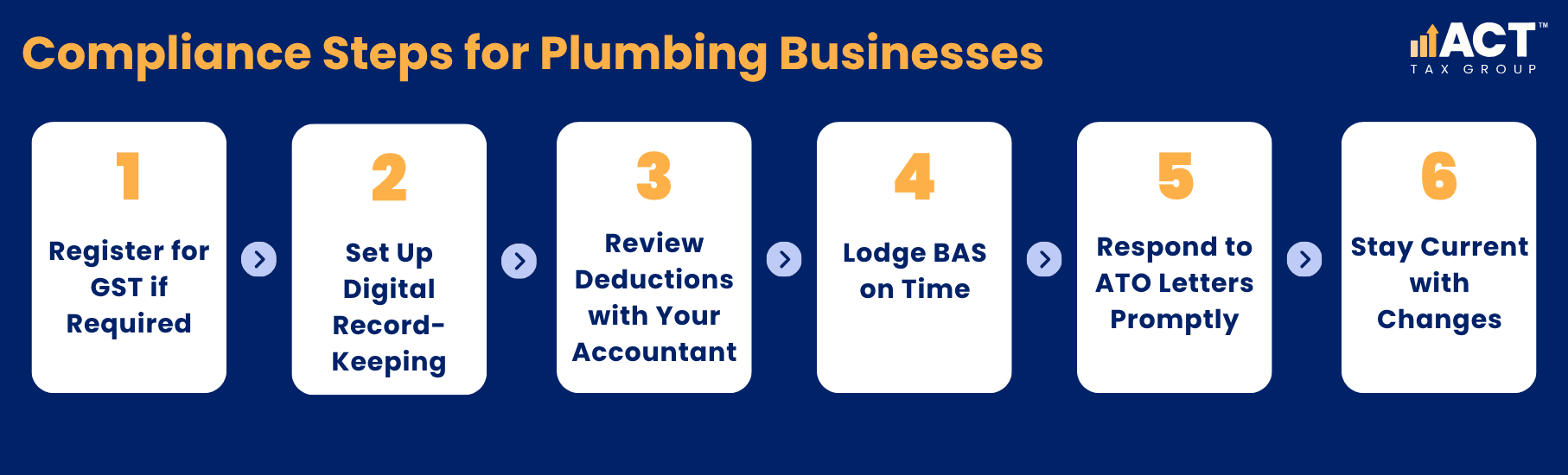

Action Steps Every ACT Plumbing Business Should Take

Here’s what you can do right now to stay compliant, reduce tax stress, and keep more profit in your business:

If your GST turnover is $75,000 or more, register for GST and start lodging BAS. Don’t wait until the ATO contacts you.

Use apps and software to capture receipts, track vehicle use, and manage invoices. Digital records are easier to organise and harder to lose.

Make sure you’re claiming everything you’re entitled to—vehicles, tools, materials, wages, insurance, rent, interest on loans—and that you have the records to support each claim.

Know your quarterly due dates, set reminders, and use a BAS agent if you need extra time or help. Don’t let late lodgement become a habit.

If you receive a notice, contact your accountant or the ATO straight away. Early action can prevent penalties and stress.

Company tax rates, thresholds, and rules can change between financial years. Review your eligibility and obligations each year, especially around June and when lodging company tax returns.

Final Thoughts

If you want clear, practical help with company tax, BAS, or getting your finances under control, speak with ACT Tax Group. We work with plumbing businesses across the ACT and know the real-world challenges you face—lumpy cash flow, payroll stress, compliance worries, and keeping the ATO happy.

This article is general information only and does not constitute financial or personal advice. For tailored support, book a consultation with ACT Tax Group.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)