Understanding the Real Cost of HECS Debts for Electricians Running Small Businesses

Published on September 16, 2025

Understanding the real cost of HECS debts for electricians running small businesses starts the moment your repayment income pushes you above the threshold. You’ve just wrapped up a big residential solar installation, but between chasing unpaid variations and managing lumpy cash flow, you’re hit with another deduction on your next pay – a compulsory repayment towards your HELP loan. Suddenly, your business bank account looks tighter than you expected.

Why ATO HECS Debt Repayments Matter for Your Cash Flow

When your small electrical contracting business is juggling wages, tools, and vehicle costs, HECS repayments become a non-negotiable slice of your income. The Australian Taxation Office calculates your compulsory repayment based on your repayment income each financial year. That means every dollar you earn above the minimum threshold counts – from trade wages to side-gigs you picked up to help cover slow weeks.

At tax time, your ATO online services profile shows your total repayment income. From there, the system withholds amounts for income tax, super, and HECS repayments in one go. If your loan balance is still above zero on 1 June 2025, it attracts an indexation rate tied to the Consumer Price Index. So even if you don’t add to your loan, its outstanding balance grows unless you make voluntary repayments before the indexation date.

Is your HECS repayment squeezing your cash flow?

Schedule a complimentary consultation with us today to keep more funds available for your business.

What Counts as Repayment Income?

Your repayment income isn’t just your wage from the daily runs. It includes net business profit, any interest or investment returns, and additional allowances. The more income you generate in your electrical business, the higher your compulsory repayment rate under the higher education loan program. In the 2024 25 financial year, repayments start when repayment income exceeds the threshold and rise progressively based on the Average Weekly Ordinary Time Earnings (AWOTE).

The Burden of Compulsory Repayments

Unlike a business loan you negotiate with a bank, your HELP loan repayments are set by law. The tax system automatically calculates what you owe and collects it through withheld amounts in your pay or as a lump sum when you lodge your tax return. That means late payments from a builder or retention clauses on commercial jobs still count toward your gross income, pushing up your repayment income even if cash hasn’t landed in your account.

What’s Changing in the 2025-26 Income Year?

From 1 July 2025, thresholds may be adjusted, so check ATO updates for the exact figures when they are published. The minimum threshold might jump, meaning many electricians running smaller operations might no longer need to repay until they hit a higher income band.

Under the new law, you’ll only pay on the slice of income above the new threshold, rather than on your entire repayment income. That change alone will reduce repayments for many sole traders and company directors in electrical services. Keep an eye on ATO online services updates in August 2025, when final figures and legislation details are published.

Choosing the Right Business Structure to Manage HELP Debt

Your business structure affects how repayment income is calculated and when you repay. As a sole trader, all business profit flows through to your personal tax return and directly adds to your repayment income. By contrast, a company structure lets you elect a director’s salary and dividends, which gives you more control over the loan account balance you report.

Sole Trader Simplicity and Drawbacks

Running as a sole trader offers the simplest setup: income minus expenses becomes your repayment income. Your HELP debt shows up in your ATO profile under study and training loans, and repayments are withheld based on total assessable income. The downside is you can’t separate business growth from personal income – every project payment counts toward your compulsory repayment calculation.

Company and Trust Strategies

If you operate through a company or trust, you can manage the timing and level of funds that hit your personal tax return. That means you could retain profits in the business to fund new equipment without immediately increasing your repayment income. However, directors must make a fair and reasonable salary, and loans distributed via trust to family beneficiaries still count as repayment income when distributed, so plan carefully with your accountant.

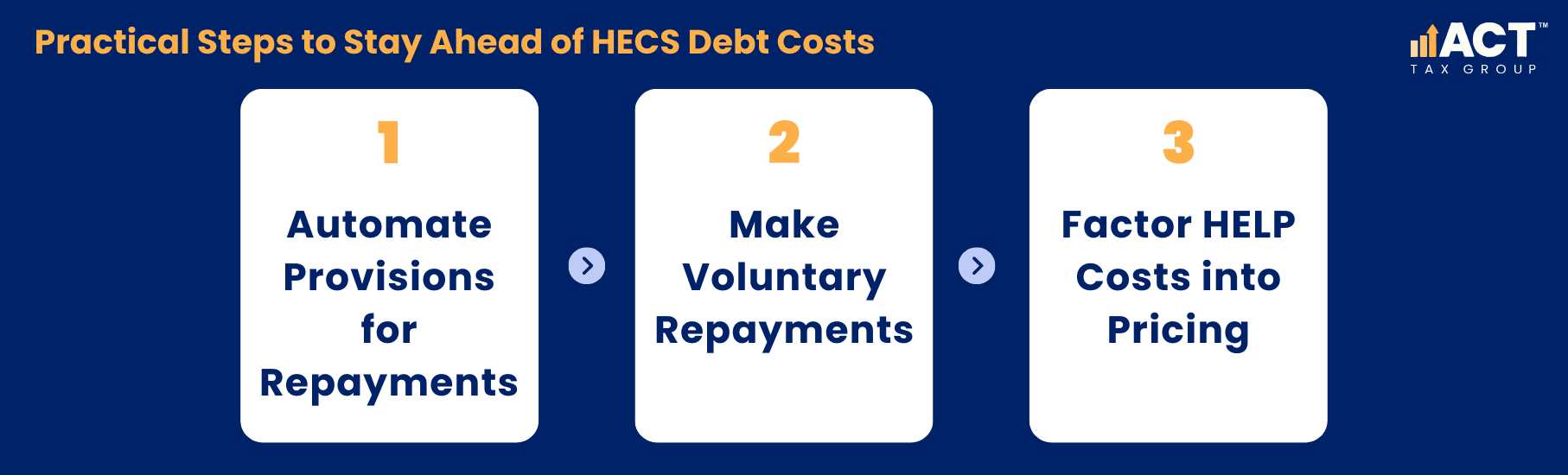

Practical Steps to Stay Ahead of HECS Debt Costs

Knowing how repayment income works is one thing; making it part of your business system is another. Here’s how to keep your HELP loan in check and preserve cash for tools, staff, and growth.

1. Automate Provisions for Repayments

Set up a separate bank account for tax and compulsory repayment provisions. Each time you receive an invoice payment, transfer a fixed percentage to this account based on your estimate for income tax plus HELP loan repayments. When tax time rolls around, you won’t have to scramble for funds.

2. Make Voluntary Repayments

Log in to ATO online services and choose to make voluntary repayments any time your cash flow allows. By reducing your loan balance before the 1 June each year indexation date, you lower the amount on which the Consumer Price Index applies, saving you from growing debt over time.

3. Factor HELP Costs into Pricing

When quoting new jobs, include an allowance for net repayment costs. If you expect to pay 2–5 percent of your income in HELP repayments, build that into your charge-out rate. That way, you’re not eating into margins every time the tax system withholds extra.

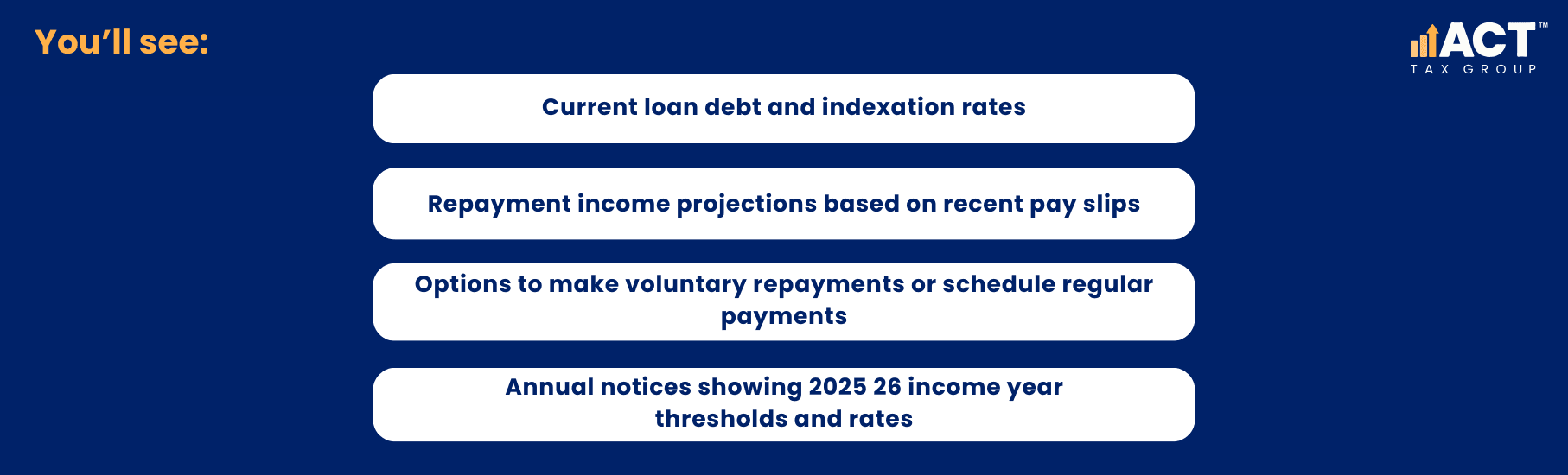

Using ATO Online Services and Tools

The Australian Taxation Office offers online services to track and manage your HELP debt, view your loan balance, and calculate upcoming compulsory repayments. Login to your myGov account, select study and training support loans.

If you’re eligible for special government support or repayment concessions, check the ATO website or speak with your accountant.

Conclusion

Understanding the real cost of your HECS debt as an electrical contractor means treating HELP repayments like any other business expense. With the 2025-26 changes on the horizon, setting aside provision amounts and adjusting your pricing now will help your small business stay compliant and thriving. For ATO-compliant support with your HELP loan and business tax planning, book a consult with ACT Tax Group.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)