Are Your Government Industry Payments Assessable? What Every Arborist Should Know

Share this article

Published on September 15, 2025

Cash flows great in summer but you’re struggling through winter, and now the council’s offered you a storm-damage cleanup contract. The payment looks good, but will the ATO want their slice? Understanding assessable government industry payments is essential for your profit and loss statement and avoiding surprises at tax time in the ACT region.

What Makes a Government Payment Assessable Income?

If you run a tree services business, most payments from government contracts or grants count as assessable income. This includes monthly payments for ongoing pruning or emergency response work, as well as one-off advance payments. Including these amounts correctly ensures your business records and tax return reflect the income you’ve earned. Note that some grants may be exempt or NANE (Non-Assessable Non-Exempt), so always confirm their tax treatment before excluding them.

Will your council contract payments increase your tax bill this quarter?

Schedule a complimentary consultation with us today to plan for PAYG and avoid surprise ATO debts.

Business Income vs. Other Business Income

Business income is the money you earn from providing tree services. Other types of payments, such as reimbursements for biosecurity work or small grants for equipment, may also need to be reported. While these can come from different sources, the ATO generally treats them as assessable income unless the payment is specifically exempt. Fuel tax credits, however, reduce fuel costs and should be recorded separately rather than counted as income.

Grants, Subsidies and Disaster Payments

Some government grants may be exempt from tax, particularly disaster recovery payments or other legislated support. Payments that compensate for losses, rather than paying for services, may not count as assessable income. However, these exemptions change regularly, so it’s important to confirm the current status with the relevant legislation or the ATO before leaving a grant off your profit and loss statement.

How to Recognise Income in Your Profit and Loss Statement

The timing and nature of government payments affect how you report them. Recording them correctly helps you manage cash flow and plan for tax instalments.

Advance Payments and Monthly Payments

Advance payments for future tree services are generally assessable in the year you receive them. Monthly payments from council maintenance contracts are also income when received. Businesses using accrual accounting may report income when earned instead of when received, so check your accounting method. Keeping clear records ensures income is reported in the correct period and helps with tax planning.

Personal Services Income vs. Ordinary Income

Most payments for arborist work are ordinary business income because they relate to providing tree services, equipment, and labour. If a contract mainly pays for your personal effort rather than services provided, it may fall under personal services income rules. For most arborists, this does not apply, but seek advice if a contract appears to focus on your individual work rather than the overall service.

Capital Gains and Capital Assets

Selling a business asset, such as a vehicle or chipper, may trigger a capital gains event if the sale exceeds its market value. Ordinary service payments and asset sales should be recorded separately, with vehicle or machinery sales tracked outside your profit and loss for services. Small business exemptions, like the 15-year active asset or retirement concessions, may apply—seek professional guidance to confirm eligibility.

GST, Fuel Tax Credits and Tax Deductions

Almost all government payments are subject to GST if you’re registered. You must include GST-inclusive amounts in your BAS and claim fuel tax credits where eligible.

GST on Government Contracts

Council contracts for pruning, stump grinding, or storm cleanup involve supplying a service, so you’ll charge GST. Report the total GST-included payment in your BAS under the “assessable government industry payments” label. This ensures the ATO sees the correct amount of GST collected and owed.

Fuel Tax Credits

When you use your vehicle or machinery for tree services, you can claim fuel tax credits for fuel consumed off-road. These credits reduce your overall fuel cost and should be recorded as a negative expense in your profit and loss statement. Include fuel tax credits under other business income, not as a deduction, because they offset your fuel expenses directly.

Decline in Value and Depreciating Asset Deductions

You can claim depreciation on assets such as chainsaws, stump grinders, and chip trucks. For small businesses, assets below the instant asset write-off threshold of $30,000 can be written off immediately. Larger assets go into the small business pool and are depreciated at 15% in the first year and 30% in following years. These rules help manage deductions efficiently and keep your records clear.

Reporting Exempt Income and Special Cases

Some payments you receive may not count as assessable income. Recognising exempt income correctly keeps you compliant and avoids overstating your gross income.

Exempt Grants and Non-Assessable Income

Certain bushfire or drought recovery grants are legislated as exempt income. They don’t form part of your assessable income, but you must note them separately in your records. If you receive one of these grants, ensure you hold documentation proving its non-assessable status, so your tax return reflects it correctly.

Wine Equalisation Tax (Irrelevant but Noted)

While the wine equalisation tax applies to wine producers and retailers, it has no bearing on arborists. However, acknowledging it clarifies that not all government-related taxes affect your business.

Keeping Records for Tax Purposes

Good record-keeping is the backbone of accurate tax reporting. It ensures you know exactly what to include in your assessable income and what qualifies as exempt.

Income Tax Return and Business Activities

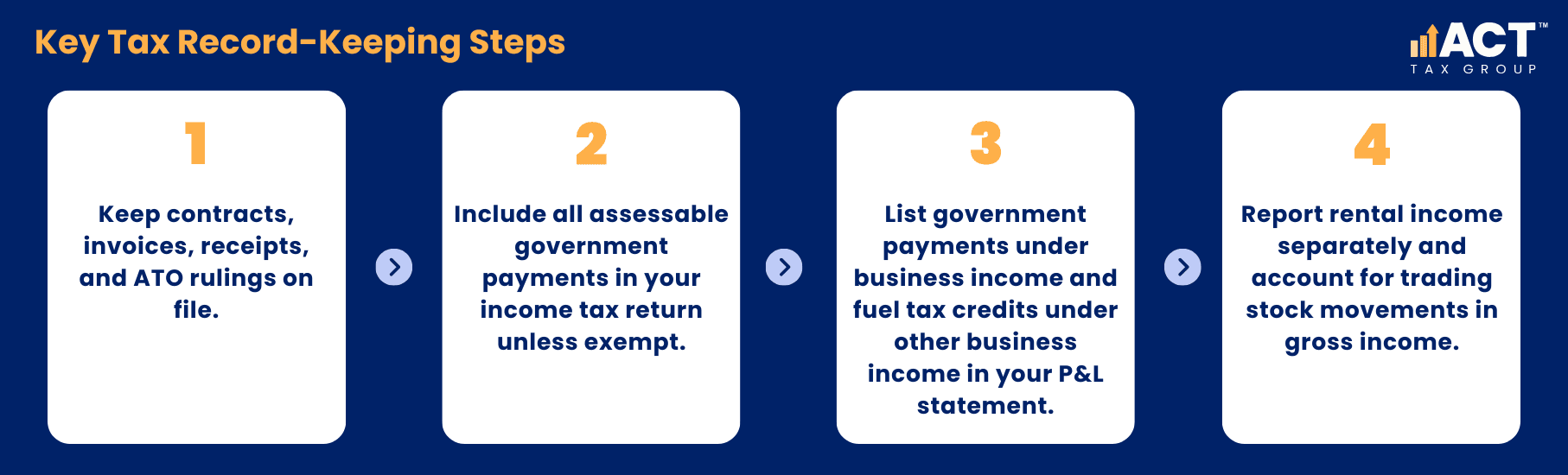

At the end of each financial year, you’ll complete your income tax return. Include all government payments in your assessable income section unless they qualify as exempt income. Keep copies of contracts, invoices, payment receipts, and any ATO rulings or grant guidelines that explain the tax treatment.

Profit and Loss Statement

Your profit and loss statement should list all assessable government industry payments under business income. List fuel tax credits under other business income and show your deductions for depreciating assets. This document forms the basis of your tax return and ensures you don’t miss any income or deductions.

Rental Income and Trading Stock

If your arborist business also earns rental income from equipment hire or sells seedlings as trading stock, report these separately. Rental income goes under other business income, while trading stock movements affect your gross income and cost of goods sold.

Planning for the Tax Impact of Government Payments

Large government payments can trigger significant tax bills. Planning ahead helps smooth cash flow and avoids surprises when paying income tax.

Quarterly PAYG Instalments

When a government contract boosts your turnover, adjust your PAYG instalments to match your higher income. Failing to do so can leave you with a large balance at tax time. Use your profit and loss statement projections to estimate your total tax liability and divide it into quarterly payments.

Balancing Cash Flow Through Seasonal Lulls

Government payments often come during busy seasons, leaving you with a tax bill right before slower months. Set aside a percentage of each payment for tax purposes—typically around 30–45% depending on your marginal rate. Holding that money in a separate account prevents cash shortages when the ATO comes knocking.

Avoiding Common Mistakes

Knowing where arborist businesses often trip up helps you steer clear of penalties and interest.

Assuming All Grants Are Non-Assessable

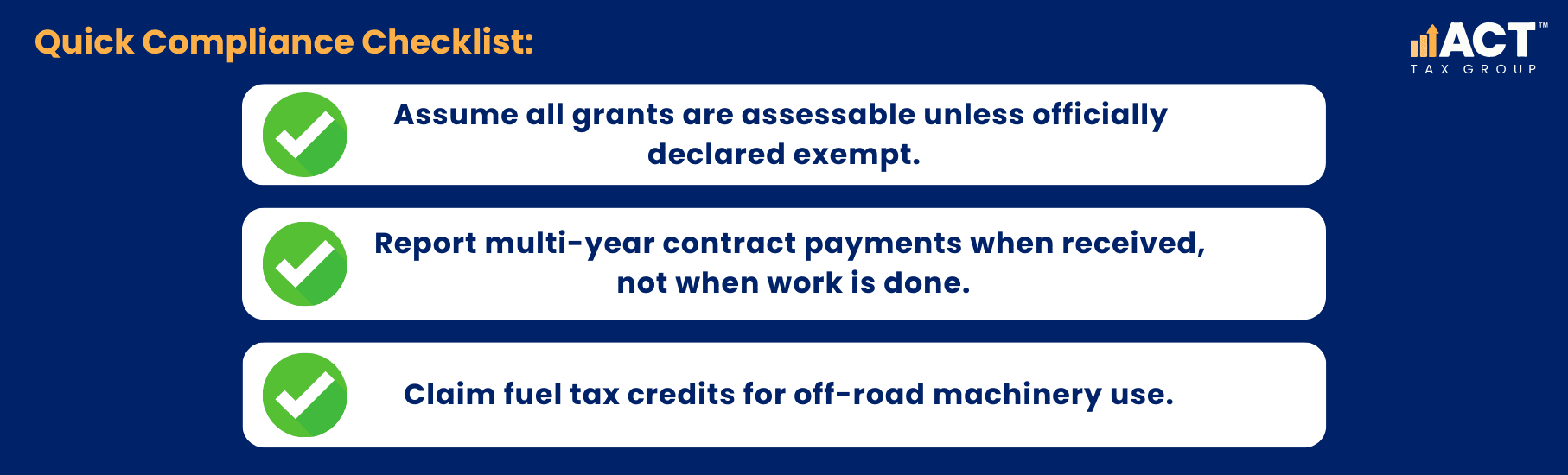

Not every government grant is exempt from tax. If a grant pays you for services, it counts as assessable income. Only officially declared exempt grants qualify as non-assessable income. When in doubt, treat the payment as assessable and adjust later if you receive clarification.

Forgetting RPM on Multi-Year Contracts

For multi-year council contracts with progress payments, make sure you report the payment when received rather than when the work is done. This keeps your BAS accurate and your cash flow projections realistic.

Overlooking Fuel Tax Credits

Too many arborist businesses forget to claim fuel tax credits on off-road machinery use. Tracking fuel separately in your records ensures you capture these credits and reduce your overall fuel expense.

Next Steps and Getting Professional Help

If you’re unsure about the tax treatment of a particular payment or grant, getting expert advice can save you headaches.

Small business entities often benefit from a quick consultation to confirm whether a payment is assessable income or exempt. An accountant can also help you prepare your trading stock schedules, rental income records, and depreciating asset pools for your tax return.

Lukasz Klekowski

Principal of ACT Tax Group, specialising in tax compliance and financial strategy for Australian small businesses.

Share this article

Disclaimer: All information provided in this publication is of a general nature only and is not personal financial or investment advice. It does not take into account your particular objectives and circumstances. No person should act on the basis of this information without first obtaining and following the advice of a suitably qualified professional. To the fullest extent permitted by law, no person involved in producing, distributing or providing the information in this publication (including ACT TAX GROUP PTY LTD, each of its directors, councilors, employees and contractors and the editors or authors of the information) will be liable in any way for any loss or damage suffered by any person through the use of or access to this information. The Copyright is owned exclusively by ACT TAX GROUP PTY LTD (ABN 31634338088)